The CBDT has notified the Income-tax Return (ITR) Forms for the Assessment Year 2019-20 with many changes and revisions. While the last date for filing income tax returns has been extended to August 31 for FY 2018-19, the changes and penal clauses for late filing mean one should start the process as soon as possible.

- ITR 1 takes into account announcements made during the Union Budget 2018-19.

- From Assessment Year 2019-20, an individual has to mention his gross salary and then the amount of exempt allowances, perquisites and profit in lieu of salary shall be deducted or added to arrive at the taxable figure of salary income. Further, the new ITR forms seek separate reporting of all deductions allowable under Section 16, namely:

a) Standard deduction

b) Entertainment allowance

c) Professional tax

- Taxpayers has to furnish details of exempt income like HRA and the clause under which the tax benefit is allowed and specify the nature of income from other sources and the deductions claimed in respect of family pension in accordance with Section 57 unlike last year where we have to mention figures only. Such extra disclosures have been asked by the Dept. to check that the ineligible persons are not using the ITR 1 and ITR 4 for filing of return.

- Use ITR-1 if you are an ordinarily resident individual with income from salary, pension and interest of up to Rs. 50 lakh, agricultural income of up to Rs. 5,000, and own one house. If this limit exceeds, use ITR-2.

Following classes of Persons who used to file ITR-1 until last year have to file ITR-2 for AY 19-20.

- Individuals being a director in a company.

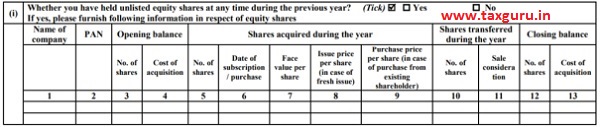

- Individuals who have investment in unlisted equity shares at any time during the FY or have capital gains / losses to declare.

- ITR 2

- This form now requires detailed information on the number of days spent in India while declaring the residential status. Until 2018-19, you had to simply choose between resident, resident but not ordinarily resident and non-resident options.

- Director in a company has to provide name of company, PAN, DIN and if the company is listed or not as shown in the table below:

- For investment in unlisted equity, taxpayers need to provide details of the company, PAN and transactions done in the financial year shown as below:-

- If assessee reports capital gain, from transfer of an immovable property, in income-tax return, it would be mandatory for him to furnish the following information about the buyer:

a) Name of buyer

b) PAN of buyer

c) Percentage share

d) Amount

e) Address of property

f) Pin code

It is mandatory for the assessee to furnish the PAN of buyer in ITR form if tax has been deduced under section 194-IA or PAN is quoted by buyer in the registration documents.

PAN is otherwise a mandatory document to buy or sell an immovable property if the stamp duty value or the sales consideration exceeds Rs. 10 lakhs.

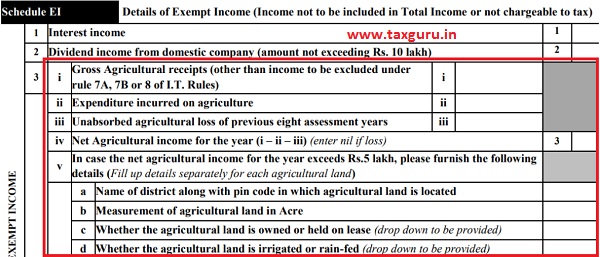

- Furnish details related to agricultural income including ownership, size, location and address and status on irrigation.

- Use ITR-2 if you are a salaried individual or a pensioner who cannot use ITR 1.

- Do not use ITR-2 if you draw income from any business or profession.

- Agricultural income

Taxpayers with agriculture income of more than Rs 5 lakhs, have to fill up ITR 2. ITR 2 asks for additional details such as the name of the district with pin code, measurement of agricultural land, whether owned/leased, etc. under exempt income schedule.

Author Bio

May I know if Savings Bank interest (Rs.10,000/-) can be claimed as additional deduction in ITR-1 for AY 2019-20 for assessees below 60 years of age. Also advise for above 60 years of age. Thanks