The ISD i.e. input service distributor provisions is being made mandatory from 1st April 2025, which will have various financial and practical challenges. ISD compliance would require a decent amount of dexterity, vigilance and expertise in its efficient and compliant implementation. To get a better understanding of ISD, this article discusses several aspects of it, which are as follows –

Page Contents

1) What is ISD? general and provisional aspects.

ISD as known, is a continued concept which existed during service tax regime as well and ISD in service tax regime was more or less an intermediary which received invoices issued under service tax regime and issued documents to distribute such credit amongst its different business units.

To obtain a more general understanding of what is ISD under GST? let’s take a scenario.

- Imagine there is a company which has a widespread business across India and each of such State presence is materialised by regional offices.

- To have a proper co-ordination between each of these regional offices, a head office has been established.

- The head office receives services like accounting, auditing, consulting, etc. not only for itself but for all the other regional offices as well.

- Now, while receiving these common services the head office pays taxes and therefore is allowed to take the credit for such taxes paid.

But what went unnoticed in this scenario is that the services availed by the head office were used by all the regional offices as well.

Which brings us to a conclusion that not only the head office, but all the other offices shall also be allowed to take ITC for such services received, based on the principle that as these services are received by such offices, they should also be allowed to avail ITC on them, in defined proportions. This would still be applicable to those entities who are unable to claim ITC as they may have significant exempt/RCM outward supplies.

To enable, regulate and manage this allowance of ITC by the head office to/by its branches. The concept of ISD was introduced in the GST law.

| Invoiced to | Actual Recipient | ISD applicable? |

| KA | All States | Yes |

| KA | KA, MH, TS | Yes |

| KA | MH | Yes |

| KA | KA | No |

An ISD in the above scenario is the head office which is receiving the services for its regional offices in various States and should distribute the credit on taxes paid amongst its regional offices. The scenarios under which ISD is applicable can be better understood with the help of the table below

Taking help of the above discussion, we can better understand the definition of ISD which is defined under 2(61) of CGST act, 2017 as Input Service Distributor means

- an office (head office in our scenario) of the supplier of goods or services or both which receives tax invoices towards the receipt of input services, including invoices in respect of services liable to tax under section 9(3) or 9(4) of CGST Act (or section 5(3) or 5(4) of the IGST Act),

- for or on behalf of distinct persons (regional offices in our scenario) referred to in section 25, and

- liable to distribute the input tax credit in respect of such invoices in the manner provided in section 20.

Several questions might arise after further discussion, that –

- Why are only the word services being mentioned here, what about the goods?

- There are many head offices that dispatch goods to their branches as well, what about the distribution of ITC for them?

- What about the outsourced manufacturer and service providers?

The ISD concept is only introduced for and encompasses the ITC related to services and not the goods.

The reason behind it being that there are no clear means to locate the ITC available to each distinct persons for services while for tangible goods its quite clear.

All the head office must do is issue cross charge invoices for goods dispatched to each branch subject to valuation rules, and they will get the credit for it accordingly.

As the tangible goods are physically identifiable as to how much is being received by each branch such problem of identification of a correct basis of apportionment or scope of accounts manipulation doesn’t occur or is reduced in relation to goods. (there is a detailed discussion on cross charge invoices and how they differ from ISD later)

To discuss the provisional aspect of ISD, one must be well versed with the following provisions related to ISD which are as follows –

1) Section-7 of CGST Act, 2017 read with schedule-1 para-1

2) Section 15 of CGST Act, 2017 read with rule-28 of CGST Ruled,2017

3) Section 25(4) of CGST Act,2017

4) Section 20 of CGST Act, 2017

5) Section 21 of CGST Act, 2017 (in combination with Sec-74A and 50)

6) Section 39 of CGST Act, 2017

7) Rule 39 of CGST Rules, 2017

8) Rule 54 of CGST Rules, 2017

9) Rule 65 of CGST Rules, 2017

Provisions which specifically relates to ISD out of the above-mentioned list can be discussed briefly as follows-

Section 21, being a penal provision broadly states that –

- Where ISD distributes the credit in contravention of the provisions contained in sec-20 resulting in excess distribution of credit to one or more recipients of credit,

- The excess credit so distributed shall be recovered from such recipients

- Along with interest, and the provisions of Section 74A ,as the case may be, shall, mutatis mutandis, apply for determination of amount to be recovered”.

- Section 21 is recovery mechanism whereas section 74A provides penal consequences!

Situations which may be considered as excess credit distributed:

- ITC distributed considering incorrect turnover as the basis of distribution

- ITC distributed considering incorrect basis (other than turnover, ex. Number of employees)

- Ineligible ITC distributed as Eligible ITC

Subsequently identified ineligible ITC:

- ITC distributed without receipt of services/receipt of invoice.

- ITC not reversed due to vendor not filing his GSTR 3B (in terms of Rule 37A)

- ITC not reversed due to non-payment to vendor (in terms of Rule 37)

Possibility of ITC reversal at recipient GSTIN location may be warranted.

Sec-39(4) which governs the “furnishing of returns” broadly states that “every taxable person registered as an Input Service Distributor shall, for every calendar month or part thereof Furnish, a return, electronically, within thirteen days after the end of such month”.

In other words, every ISD must furnish a return for a tax period by 13th of the month next to such tax period.

For example, for April’25 month, the return would need to be filed on or before 13th May’25. Considering that GSTR 6A auto-populates based on vendor GSTR 1 filing (due date being 11th), there are only 2 days, i.e. 12th & 13th to ensure ISD filing compliance.

Rule 39 which discusses the manner of distribution broadly directs the ISD about –

- Distribution of ITC – The ITC of a period shall be distributed (eligible and ineligible separately) in the same period under form GSTR- 6, and it should not exceed the ITC available for distribution. (i.e. the amount distributed shall be equal to amount available)

- Attribution of ITC – the attribution shall be done as follows:

a. If it relates to a specific recipient, it should be distributed only to him

b. If it relates to a fraction of all the recipients, then it should be distributed amongst that fraction of recipients in the proportion of their turnover for the relevant periods to the total turnover.

c. If it relates to all the recipients, then it should be distributed among all the recipients relative of their turnover to the total turnover. (relevant period means previous financial year or the last quarter if there was no turnover in previous year)

- Formula for distribution – C1 = (t1 / T) × C

Where t1 is recipient’s turnover, T is the total turnover of all concerned recipients, and C is the total credit to be distributed and C1 is the apportioned credit. This can be understood with help of the table below –

(Table showing distribution of ISD credit based on turnover)

| Scenario | Description | ITC Distribution | Example |

| ITC belongs to a single entity

|

All the input services are used only by a single recipient entity. | The entire ITC is distributed to the single recipient entity. The distribution is done based on the proportion of the eligible ITC, i.e., 100% of the ITC goes to this entity. | HO receives ITC of ₹1,00,000 and Entity A is the only recipient of the service, the entire ₹100,000 is distributed to Entity A. |

| ITC belongs to one or more of the entities | ITC belongs to more than one entity, but not all entities. | The ITC is distributed in proportion to the eligible turnover of each recipient entity. The distribution will be done based on their turnover ratio, but not all entities will get it. | HO has ₹20,000 ITC, which belongs to Entity B with ₹50,000 turnover and C with ₹1,50,000 turnover.

ITC will be distributed as B – 5,000 and C – 15,000. |

| ITC belongs to all the entities | ITC is applicable to all the entities, and distribution is based on their turnover | The ITC is distributed to all recipient entities based on the turnover of each entity. The total ITC is allocated proportionally among all the entities. | HO has ₹20,000 ITC, which belongs to all entities wherein Entity A has 2,00,000 turnover, B has ₹1,50,000 turnover and C has ₹50,000 turnover.

ITC will be distributed as A – 10,000 B – 7,500 and C – 2,500. |

4) Tax-Type Distribution – While distributing credit the thing to be kept in mind is IGST will be distributed as IGST while CGST and SGST will be distributed as CGST and SGST respectively to the distinct person situated within the same State or UT as the ISD or as IGST to the distinct person situated outside of the State or UT in which ISD is situated. (For example – if an ISD is registered in Karnataka and has an invoice with CGST + KAGST and it has to be distributed to an entity within Karnataka, it will be distributed as CGST + KAGST. But if it has to be distributed to an entity in Delhi it will be distributed as IGST)

5) Invoices and Credit note – ISD must issue separate invoices or credit notes to the recipients when they distribute the credit and in case of decrease in ITC distributed due to credit note issuance, same procedure shall be followed as above to give effect to such change in credit. For increase, ISD debit note not specifically provided for in GST law, possibly fresh ISD invoice to be raised.

Rule 54 discusses the contents of an invoice or credit note to be issued by ISD or any other distinct person who is the recipient of services (even under RCM) who invoices such transactions to ISD for distribution, which are as follows:

- An Input Service Distributor (ISD) invoice under GST must include the ISD’s name, address, and GSTIN, a unique consecutive serial number not exceeding 16 characters (with alphabets, numerals, or special characters), the date of issue, the name, address, and GSTIN of the recipient to whom the credit is distributed, the amount of credit distributed, and the signature or digital signature of the ISD or their authorized representative.

- As for the distinct person issuing invoices to ISD for supplies received under RCM to be distributed by the ISD point most of the things remains same except additionally they should include their own GSTIN and GSTIN of ISD (refer to the chart below for better understanding).

But, if the ISD is a banking company or a financial institution, including a non-banking financial company, a tax invoice shall include any document in lieu thereof but must contain the details mandated in Rule 54 discussed as above.

Lastly, Rule – 65 which broadly states that

- Every Input Service Distributor shall, based on details contained in Form GSTR-6A, and where required, after adding, correcting or deleting the details, furnish electronically the return in GSTR-6

- GSTR-6 should contain the details of tax invoices on which credit has been received and those issued under Sec-20,

- Such return is to be filed through the common portal either directly or from a Facilitation Centre notified by the Commissioner”

In other words, an ISD must file the GSTR-6 in line with Sec-39 as discussed earlier. After considering, adding, deleting or correcting the details included in the GSTR-6A, which is similar to GSTR-2A available for GSTR-3B, showing real time dynamic details of all the invoices available for distribution.

………contd.

2) Practical procedure and challenges faced with ISD implementation and filing ISD returns

Before deciding to implement the ISD, it is important to understand that

- What are the expenses that are being received by ISD on behalf of the distinct persons?

- What basis should it be decided to be classified under ISD?

- Which distinct person must the credit be distributed to?

- Whether eligible and ineligible credit can be distributed?

- What entities can be covered under ISD and what entities are to be covered under cross charge?

- How many and in which state the ISD registration should be obtained?

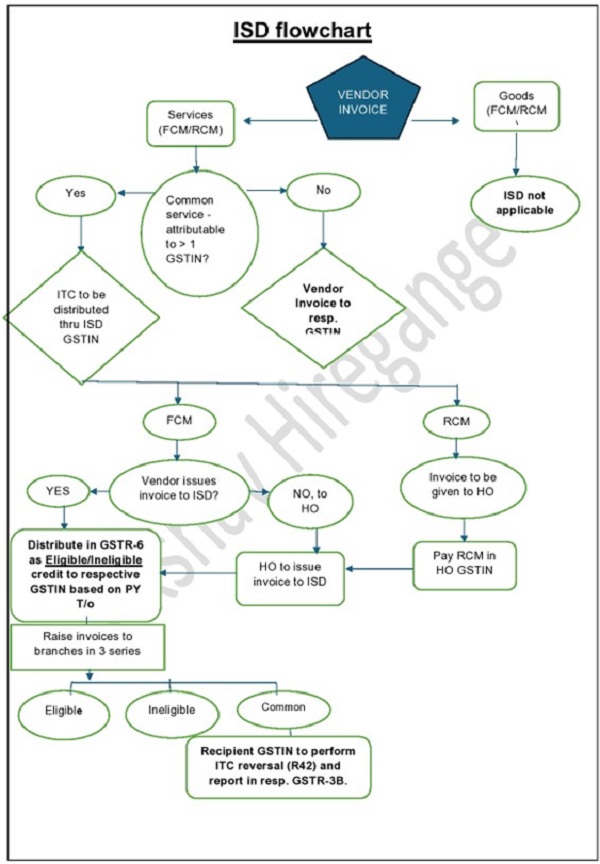

- What will be the flow of the expenses and how they should be availed, allocated and distributed? (click on the link below to refer the flow chart attached to understand the flow of transactions)

After above-mentioned questions are answered, for filing ISD returns following steps can be followed, kindly note that these are general steps and can be modified based on the individual filer’s requirements.

Step 1 – Arrange the data required for the ISD returns i.e. details of invoices accounted in books and downloaded excel of GSTR-6A.

Step 2 – Consolidate them with the earlier data available of past periods (if any) and run a reconciliation between both the consolidated 6A and invoices accounted (which are invoiced to ISD)

Step 3 – Now the invoices reconciled can be uploaded to table 3 (invoices) and table 6B (credit note) through offline utility tool.

Step 4 – And after that, the ISD invoices shall be uploaded to the table 5(invoices) and 8 (credit note) which are appropriately distributing the ISD to various distinct persons.

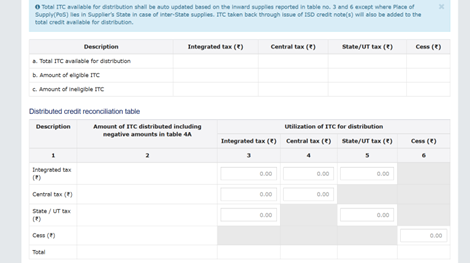

Step 5 – After all, the invoices are uploaded, table 4 shall be prepared, as follows:

1) 4(a) will be auto populated from Table 3 and 6B

2) 4(b) & 4(c) will be auto populated from Table 5 and 8

3) The sum of Table 4(a) should be equal to the sum of Table 4(b) and 4(c)

4) And then we move to table titled as “distributed credit reconciliation table” under which the column “Amount ITC distributed including negative amounts in Table 4A which also has figures populated through table 4(a), corresponding to the table we have to provide the details of the manner in which we distributed the credit as discussed while discussing the rule – 39 and then we have to click on the tab calculate ITC and save the form.

Table 4 in GST portal

Step 6 – After saving the form filer can proceed to file the GSTR-6

Following things shall be kept in mind while filing the returns –

1) While uploading invoices and credit notes in offline tool, due care should be exercised and proper acceptable format for data should be used (for ex- invoice date should be in DD-MM-YYYY format) and anything to be selected from the drop-down selection in a cell shall be selected from drop down selection and not to be written as it is.

2) The ITC available should be equal to ITC distributed otherwise portal won’t allow table 4 to be saved.

3) Reconciliation between books and GSTR-6A is performed on consolidated basis to avoid missing out any previous tax periods’ invoices populating this month.

4) The consideration of the date till which the invoices shall be considered in a tax period’s GSTR-6 is at the discretion of the filer.

5) The Table 4, once filled wrong can be filled again only after 10 minutes of clicking on the “calculate ITC tab” therefore due care should be taken while filling the utilization of ITC distribution column in “Distributed credit reconciliation table”

Once the GSTR-6 is filed the Table 4(A)(4) of GSTR-3B will get auto populated with the ITC apportioned to the respective registrations.

ISD invoices will not auto-populate in the IMS of the recipient GSTIN and would directly display in the GSTR 2B and GSTR 3B accordingly.

For ensuring smooth implementation and compliance, the preliminary personnel and system requirements are as follows:

- The Personnel should be trained and given the knowledge of all the provisions discussed above and they should ensure that all the invoices, on which ITC is to be distributed are accounted in a separate log in made for accounting ISD invoices and all the invoice copies should have ISD’s GSTIN mentioned.

- The ledger to be maintained in such cases are listed below:

CGST/SGST/IGST ISD A/c [ITC claim]

CGST/SGST/IGST ISD-TN Eligible A/c [ITC distribution]

CGST/SGST/IGST ISD-TN Ineligible A/c [ITC distribution]

CGST/SGST/IGST ISD-TN Common A/c [ITC distribution] (for taxable & exempt)

TN – Assumed States. Based on no.of States, ledgers may increase.

- The vendors should be communicated to only include ISD’s GSTIN in such invoices and ensure this while filing their GSTR-1, so that it gets correctly populated in GSTR-6A.

- The entities receiving RCM invoices and are issuing an invoice for such services to ISD shall ensure that the ISD’s GSTIN as well as their own GSTIN is mentioned in such invoice and accounting is also done in line with such GSTINs.

- The IT infrastructure for such ISDs needs to be robust with in-built GST compliance and a system to flag common expenses and/or ISD invoices and to differ it from regular invoices and to mitigate the clerical mistakes that can curb the proper flow of accounting and thereby the credit.

- A recommended list of common expenses which can be potentially distributed by ISD is attached below for reference.

- Advertisement

- Analysis /Testing Charges

- Bank and Telephone Charges

- Commission Sales Promotion Expenses

- Conference & Seminar Expenses

- Conveyance

- Courier Charges

- CSR Expenses

- Insurance and L&D Expenses

- Exhibition – International and Domestic

- Freight

- Hiring Charges

- Housekeeping

- IT Services

- Membership & Subscription

- Professional & Legal Charges

- Repair & Maintenance

- Security Charges

- IPO/Brokerage expenses

3) Comparison between cross charge and ISD

| Aspect | ISD (Input Service Distributor) | Cross Charge |

| Definition | ISD is a mechanism to distribute Input Tax Credit (ITC) related to common services to various units of an organization | Cross charge refers to the inter-unit transfer of goods or services within the same legal entity but across different GST registrations. |

| Applicability | ISD applies to input services used by distinct persons. | Cross charge applies to goods and services transferred between different GST registrations under the same legal entity. |

|

Nature of Transactions |

||

| Tax Credit Distribution | ITC is allocated from a central unit (ISD) to distinct persons. |

A separate invoice is raised for the supply between different GST registrations, and the GST paid is used by the receiving unit for ITC. |

| Valuation | ITC to be distributed as per Rule 39 based on Turnover and does not attract valuation provisions. | Valuation is linked to Rule 28 and ITC eligibility to the recipient entity.Valuation linked to Rule 28 and eligibility of ITC to the recipient entity. |

| Invoicing | ISD issues an ISD invoice for the ITC distribution. The invoice is typically issued to the eligible units. | A normal tax invoice is raised for the supply of goods or services between the different GST registrations, as per the regular GST rules.

|

| Eligibility | Only distinct persons registered within the same PAN are eligible for ISD credit.

|

Any unit within the same legal entity (separate GST registration) can raise or receive a cross charge, but it is for supplies of goods or services between such units |

| GST return to be filed | GSTR-6 is to be filed | These transactions are routed normally through GSTR-1 and 3B |

| Types of inputs | Applies only to input services. | Applies to all kind of inputs. |

| GST liability | No GST is levied on transactions between ISD and distinct persons.

|

GST is levied on the cross-charge transaction (goods or services) from one registration to another based on section 7 read with schedule 1 |

- Generally, ISD is a concept used for ‘distribution’ of ITC to one or more supplying units, whereas cross charge is the concept for ‘accumulation’ of ITC scattered at different location to a central location. The concept of cross charge enables the assessee to use the ITC effectively.

- However, since ISD is made mandatory for the offices receiving input services on behalf of distinct persons we will be required to file GSTR-6 for all such transactions and distribute the credit but for Input and capital goods’ ITC distribution the cross charge is still available.

- Under cross charge there is still a supplier and a recipient, but ISD is not a recipient but a mere distributor of credit and exist for the sole purpose of it.

- And meanwhile ISD invoices are dealt through GSTR-6, cross charge invoices doesn’t have any separate returns made mandatory for disclosure and are dealt with through GSTR-1 (by issuer of such invoices) and GSTR-2B and 3B (by recipient of such invoices) which makes cross charges an easier affair.

- Circular 199/11/2023-GST provides clarification on cross charge services between distinct persons. Circular 211/5/2024-GST on valuation on import of services.

4) Frequently asked questions on ISD

After all the above discussion, certain frequently asked questions in relation to the ISD concept are discussed in this section of article.

Q1 – Is E-invoice generation mandatory for ISD?

Ans – No, as ISD is not making any outward taxable supplies but is merely distributing the credit. The E-invoice generation is not mandatory for it.

Q2 – Will IMS have invoices related to ISD?

Ans – No, in the advisories issued by GSTN for the IMS it is clearly mentioned that invoices related to ISD credit distributed will directly flow to GSTR-2B rather than getting populated in IMS.

Q3 – Will RCM invoices be a part of ISD?

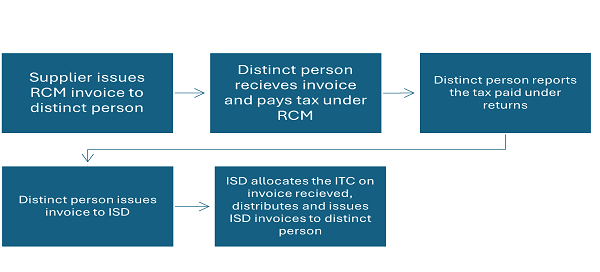

Ans – No, RCM invoices cannot directly become the part of ISD as ISD has no option to disclose and pay off the RCM invoices as regular taxpayer has when he files the 3B. instead as per Rule 54(1A) indirectly a distinct person receiving such services can issue an invoice to the ISD for services received by it on behalf of all the entities chargeable to tax under RCM and ISD can in turn distribute the credit based on such invoices.

Q4 – Is ISD applicable on a head office of a multi-State organization with registrations in different States with different PAN (on internally generated services)

Ans – No, ISD is only applicable when services are being received by an office on behalf of its distinct persons and based on sec-25(4) and as a person can have only one PAN, ISD will only cover distinct persons to the extent they are registered under the same PAN.

Q5 – What about the inputs and capital goods purchased by head office on behalf of the distinct persons?

Ans – The ISD can only distribute ITC available on input services as per Sec-20. Therefore, the option of cross charge can be explored for capital goods and inputs (goods) while giving due attention to Rule -28.

Q6 – Do ISD invoices from the GSTR-6 flows and get reflected in GSTR 2B?

Ans – Yes, once the GSTR-6 is filed the GSTR-2B gets populated with the ISD invoices (as well as Table 4(A)(4) of GSTR-3B) and for invoice wise details sheet “ISD” and/or “ISDA” can be referred.

Q7 – If there is a newly formed entity which is newly registered and doesn’t have any turnover in previous year or quarter, what shall be the turnover for relevant period for such entity under Rule 39?

Ans – As there is no base to distribute credit to such entities it is advisable to not consider such entities for distribution. Once the quarter completes, then such details may be used for distribution until previous financial year are available.

Q8 – Can a composition scheme dealer have the ITC attributable to it?

Ans – No, because as per the provisions of sec-10 of CGST Act, 2017 A composition taxpayer shall not collect any tax from the recipient on supplies made by him nor shall he be entitled to any credit of input tax and moreover if one registration has opted for Sec-10, all the registration under the same PAN has to opt for it.

With the careful reading of the above provisions we can conclude that the fact of inclusion of composition taxpayer is not legally possible.

Q10 – What if the SGST to be distributed is different from the State or UT in which ISD is registered?

Ans – Such ITC cannot be distributed through the ISD registerted in another State. Although, to distribute such ITC registration in such States or UTs can be taken especially if the marketing or operational team frequently visit these States or UTs which needs to a large amount of ITC accumulation. Multiple ISD registrations can be taken under a single PAN.

Q11 – Is ISD required to be distributed to an SEZ as well? What if it is only making zero rated supplies? Will the refund be allowed for such credit?

Ans – The SEZs will be treated as a distinct person like any other distinct persons and the credit will be distributed to them based on the turnover. To avoid ITC accumulation at SEZ entities it is suggested to have specific vendor invoicing to SEZ under LUT (with appropriate procedural compliance) and application to claim the refund shall also be allowed on such accumulated credit. (Britannia Industries Limited v. Union of India (SC))

Q12 – What if the invoice includes both services and goods?

Ans – Since the invoice will have ISD’s GSTIN on it, once GSTR-1 is filed it will get populated with the entire amount in GSTR-6A. The ISD shall be required to bifurcate the credit into two parts and consider only the input services’ ITC and discard the goods related ITC.

To avoid such wastage of credit it is advisable to communicate with the vendor to issue separate invoices for goods and services wherein goods will be invoiced to the concerned registered persons directly and services will be invoiced to ISD.

Q-13 Can we implement any other logical basis for apportionment of credit by ISD to branches?

Ans – In the earlier tax regime before April 2012 there was no provisional formula for allocation of ISD credit to the distinct person and any reasonable base was being used and agreed upon for the distribution of the credit. (TITAN INDUSTRIES V/S SERVICE TAX TRIBUNAL). After Apr 2012 onwards, turnover based ITC distribution was only allowed.

for example – the employee state insurance expense was being distributed based on the number of employees in the organization) but post such period and in GST regime also a formula for distribution has been implemented in the law (Rule 39 of CGST Rules, 2017) which is incorporates turnover in state or UT of the recipient entities.

Q-14 – What if an invoice is partly eligible and partly ineligible?

Ans – If an invoice is partly eligible and partly ineligible it is suggested to distribute such invoice as eligible between the distinct persons and after receiving such credit the recipient should bifurcate such invoice into eligible and ineligible and perform the necessary reversal therein.

Q-15 How should the ineligible credit be distributed under ISD?

Ans – It is suggested to distribute such credit as ineligible credit and the same shall be auto-populated in GSTR-3B of the recipient entity under 4(A)(4) as ISD’s distributed credit and under 4(B)(1) as a permanent reversal and if it is not being populated as such it is suggested to perform necessary reversal under 4(B)(1) manually in the recipient GSTIN against such ineligible credit.

Q-16 Whether disputed ITC must be reversed by the ISD or specific recipient GSTINs?

Ans – ISD is required to distribute credit, it does not claim or utilise ITC in itself. The credit if any must be reversed at the recipient GSTIN. Legally, the department must also raise notice to respective GSTINs for ITC reversal, although this remains a grey area presently. Under Service Tax regime, decisions on ineligible ITC were to be made at the recipient locations’.

Q-17 Whether ITC must be distributed to unregistered locations/wholly exempt locations?

Ans – Yes, the ITC must be distributed to such units as per computation, and as such ITC would not be eligible would be revenue to respective Govt. Even if there is an unregistered location (which has no outward/inward/RCM supply), ISD ITC must still be distributed.

Q18 – Where ISD distributed short ITC, can it raise ISD Debit Note for the balance?

Ans – No. ISD Debit Note is not provided in the CGST Rules. ISD Invoice may need to be raised to rectify this anomaly, as a procedural lacunae cannot take away substantive rights.

5) Benefits and drawbacks

Since the ISD in made mandatory from April 2025, it is important to know what benefits and drawbacks it accompanies and to take the benefits as a force of motivation for compliant implementation while keeping drawbacks in mind to be prepared for all the legal, financial, and procedural changes it poses.

To discuss briefly, following are the benefits and drawbacks of ISD implementation.

Benefits:

1) ISD may lead to proper, justified and efficient distribution of ITC between all the parties involved as turnover is a good base to judge as to how much credit should be given to a party.

2) ISD ensures that benefit of ITC is dispersed between all the parties which are entitled to it and results in no loss of credit in the process as available and distributed ITC should remain same.

3) Cross charges between entities for services poses certain problems and raises department’s eyebrows as cross charges are often associated with manipulation of accounts for illegal tax planning.

4) It also ensures smooth flow of credit especially in a multi-State organisation.

5) Helps to avoid departmental disputes and possible disallowance of common credits.

Drawbacks:

1) The ISD implementation leads to several administrative burdens such as tracking all the input services, communicating with vendors to issue invoices with ISD’s GSTIN, training accounting team to account regular and ISD invoices separately which in turn increases workload and complexity in business and often such administrative changes take time to get accepted by the team which in turn further leads to mistakes and non-compliance.

2) The ISD is only available for input services and not for inputs (goods) and capital goods (goods capitalised in books) which nullifies its benefit of proper credit allocation with relation to credits for the latter two.

3) As ISD implementation requires change at an organisation level which consumes a lot of time and resources and sometimes require external consultancy for proper implementation which in turn increases compliance cost

4) As discussed before, due to ISD to be treated as a separate entity for bookkeeping it is quite common that it is confused as a regular entity, which may lead to unwanted errors and discrepancies in accounts which might lead to issues in year-end ITC reconciliations. Which may further lead to incorrect distribution and attract penalties under GST law.

In conclusion, the ISD is being made mandatory soon, this article describes a wholesome approach as to how one should understand, prepare, file and weigh in the benefits and drawbacks (impacts) of the ISD implementation.

Disclaimer – The views expressed in this article are personal to the authors and are an attempt to interpret the nascent GST law. We recommend professional assistance where required.

Queries or Feedback – anuj@hnaindia.co.in & akshay@hnaindia.com.

Author Bio

Please refer R54(1A) CGST Rules

Also refer Section 20 of IGST Act.

In the flowchart, it is mentioned that the regular GSTIN in the same state in which ISD can transfer the credit of common service under forward charge to ISD by issuance of the invoice on ISD, whereas no specific provision is provided u/r 39 or in Sec. 20 of CGST Act, 2017. Under which provision can the same be distributed? Please also clarify how the IGST ITC under RCM from regular GSTIN to ISD GSTIN is to be transferred, as no specific mechanism is available on GSTIN portal.