The issues addressed in the guideline outlined in Circular No. 20 of 2023-Income Tax dated December 28, 2023 by CBDT are as follows:

Issue 1: Who should deduct tax at source where there are multiple E-Commerce operators (ECO) involved in a transaction?

Resolution for Issue 1:

Let’s create 2 situations and understand with an example:

Situation 1: Where multiple ECOs are engaged in a single transaction on an ECO platform for the sale of goods or services, with the seller-side ECO not being the actual seller, the buyer-side ECO facilitates the buyer, and the seller-side ECO facilitates the seller.

For a visual representation to enhance comprehension, refer to the below image:

Conclusion: Under section 194-O of the Act, compliance lies with the seller-side ECO responsible for the payment to the actual seller. Tax deduction occurs on the gross amount of sales or services, done by the seller-side ECO at the time of credit or payment to the seller, whichever is earlier. Seller ECO completes the TDS return in Form 26Q and issues a Form 16A certificate to the seller.

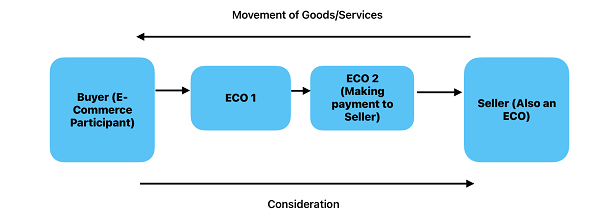

Situation 2: Where the seller-side ECO is the actual seller, consider a situation where ECO-1 facilitates the buyer, and on the selling side, the seller itself, ECO-2, directly interacts with another ECO.

For a visual representation to enhance comprehension, refer to the below image:

Conclusion: In compliance with section 194-O of the Act, the responsibility lies with the ECO making the payment to the seller, which, in this case, is ECO-2. Tax deduction occurs on the gross amount of the sale at the time of credit or payment to the seller, whichever is earlier. ECO-2 then files the necessary TDS return in Form 26Q and issues a Form 16A certificate to the seller.

Issue 2: E-commerce operators may impose convenience fees or commission per transaction, and sellers might apply logistics and delivery fees. Payments to the platform or network provider, like ONDC, facilitating the transaction are also common. Do these elements constitute part of the “gross amount” for TDS purposes under section 194-O of the Act?

Resolution for Issue 2:

Let’s understand with some examples:

Example 1:

A buyer makes a Rs 100 purchase from a seller, choosing home delivery. The seller adds Rs 5 for packing, Rs 10 for shipping, and Rs 3 as a convenience charge (covering fees from both buyer-side ECO and seller-side ECO). The seller issues a Rs 118 invoice (Rs 100 + 5 + 10 + 3) to the buyer. Shipping, packaging, and convenience fees are separately billed. In this case, what will be the gross amount on which TDS u/s 194-O is to be deducted?

Solution 1:

The TDS should be calculated based on the entire invoice amount of Rs. 118, as it encompasses the total value of the transaction, including the original purchase, packaging, shipping, and convenience fees.

The conclusion drawn from the example is that convenience fees, transaction commissions, as well as logistics and delivery charges, are considered part of the gross amount. Payments made to the platform or network provider, such as ONDC, which facilitates the transaction, will also be included in the gross amount subject to TDS under Section 194-O.

Issue 3: How are GST, state levies, and other taxes treated when calculating the gross amount under section 194-O of the Act?

Resolution for Issue 3:

As outlined in Circular no. 13 of 2021 (Para 4.3.2) for TDS on purchase of goods, if GST is separately indicated in the invoice and tax is deducted at the time of credit, it should be done on the amount credited excluding GST. Similar clarification applies to state levies and taxes in Circular No. 20 of 2021 (Para 5.2.3).

Under section 194-O, if tax is deducted at the time of credit and the GST/state levies and taxes are indicated separately, deduction is on the credited amount without including these components. However, if deducted on a payment basis (earlier than credit), it’s on the entire amount as identifying components for future invoicing is not possible.

Issue 4: How will adjustments for purchase -returns take place?

Resolution for Issue 4:

For purchase-returns under section 194-Q, as clarified in circular No. 13 of 2021, if tax is deducted before the return, it can be adjusted against the next purchase from the same seller. No adjustment is needed for replaced returns.

Similarly, under section 194-O, tax must be deducted before a purchase-return. If tax is deducted and refunded due to a return, it can be adjusted against the next transaction with the same seller in the same financial year, and the deducted and deposited tax serves as credit to the seller. No adjustment is necessary if the return is replaced by goods, completing the transaction.

Issue 5: How will discounts given by seller as an e-commerce participant or by any of the multiple e-commerce operators be treated while calculating “gross amount”?

Resolution for Issue 5:

Treating Discounts in the Calculation of “Gross Amount”:

A) Seller Discount:

When the seller provides a discount, it reduces the product or service price. For instance, if a product is labeled at Rs 100, and the seller offers a Rs 10 discount, the buyer pays Rs 90. Consequently, the invoice is for Rs 90, and TDS is calculated on this amount.

B) Buyer ECO or Seller ECO Discount:

In scenarios where the buyer ECO or seller ECO offers a discount, the seller generally receives the full consideration, with part paid by the buyer and the remainder by the ECO. For example, if the seller quotes Rs 100 and the buyer ECO gives a Rs 10 discount, the buyer pays Rs 90, and the ECO settles the remaining Rs 10. The invoice is for Rs 100, and TDS is deducted by the seller-side ECO on this gross sales amount of Rs 100.

For a more in-depth understanding, please consult the circular using the provided link: https://rb.gy/i1yyeq

Author Bio