India is 169th Country to implement GST. There were the following common aspects, when GST was introducing in each country.

- Unrest due to inflation after implementation of GST.

- Political Parties, which introduced GST, had lost the subsequent Election.

Perhaps, this might have in the reason, Govt. of India wish to take the safeguarding measures and introduced Section 171 of CGST Act 2017, very clearly specifying:

Quote

171. Anti profiteering measure.

(1) Any reduction in rate of tax on any supply of goods or services or the benefit of input tax credit shall be passed on to the recipient by way of commensurate reduction in prices.

(2) The Central Government may, on recommendations of the Council, by notification, constitute an Authority, or empower an existing Authority constituted under any law for the time being in force, to examine whether input tax credits availed by any registered person or the reduction in the tax rate have actually resulted in a commensurate reduction in the price of the goods or services or both supplied by him.

(3) The Authority referred to in sub-section (2) shall exercise such powers and discharge such functions as may be prescribed.

Unquote

After introduction of GST, it was expected that prices to come down but there is increase in rate of inflation. There is chaos among st the Consumers, Manufacturers, Traders, Service Providers and hardly there was any change in the prices except some sectors, but it was insignificant.

Anti-Profiteering Rules were notified and the frame work of the working of Anti-Profiteering Authority has been decided:

1. Standing Committee & Screening Committee will be formed consisting of State Govt & Central Govt Officers

2. Any person including consumer can make an application to Anti-Profiteering Authority w.r.t. non-reduction of prices

3. All applications from interested parties on issues of local nature shall first be examined by the State level Screening Committee and the Screening Committee shall, upon being satisfied that the supplier has contravened the provisions of section 171, forward the application with its recommendations to the Standing Committee for further action.

4. The Standing Committee shall, within a period of two months from the date of receipt of a written application, in such form and manner as may be specified by it, from an interested party or from a Commissioner or any other person, examine the accuracy and adequacy of the evidence provided in the application to determine whether there is prima-facie evidence to support the claim of the applicant that the benefit of reduction in rate of tax on any supply of goods or services or the benefit of input tax credit has not been passed on to the recipient by way of commensurate reduction in prices.

5. The findings of the Standing Committee will be placed before GST Council and if the benefit has not been passed, such amount may be levied as penalty, will be deposited in the Consumer Welfare Fund

The government has been continuously under pressure to increase vigilance over the MRP under GST across the nation. The GST council has earlier set up Anti Profiteering committee to check the tax evasion and any price related difference before and after GST from a particular product or a list of products. Under the GST, it was pre- decided that all the cost input saved after the returns of ITC benefit must be passed onto consumers in the form of a price decrease. If in case, the manufacturer of trader is not obedient to the rules, then the National Anti-Profiteering Authority can order for certain rules and provision nationwide i.e.

- Price Decrease announcement

- Benefit with 18 percent interest

- Penalty

- License cancellation of faulty manufacturer

The consumer can file his complaint to the committee and if the nature and effect of the complaint are nationwide than the Standing committee must be contacted while if in case the nature and effect of the complaint are on the regional level than the State screening committee will take a decision on the concerned matter.

It is the challenging task before any manufacturer or the dealer or the service provider to work out the additional Input Tax Credit and benefit on account of reduction of GST Rate. There are various factors to determine the prices e.g.

1. Competition in the market based on economic theory of demand & supply.

2. The cost of inputs and input services

3. The cost of Distribution and the margin of Distributors, Stockist, Wholesaler & Retailors etc etc

There has to be a mechanism and specified format to work out additional input tax credit and benefit on account of rate reduction as compared to earlier regime and subsequently. However, rule do not provide any format and therefore it is difficult to ascertain and come to the specific conclusion to determine whether benefit is pass on or otherwise.

Moreover, Legal Metrology Act provides the mandatory requirement on putting the MRP on each Package Commodity but there is no methodology in any act which determine how to fix the MRP.

The provision has been made so as to curtail exploitation of the consumer and majority of the products of Package Commodity are sold on MRP to the Consumer. It is important to understand the important provisions of Legal Metrology (Package Commodities) Rules 2011. Rule 2(m) provides the definition of “Retail Sale Price”

Quote :

(m) “Retail Sale Price” means the maximum price at which the commodity in packaged form may be sold to the ultimate consumer and the price shall be printed on the packages in the manner below :

“Maximum or Max. retail Price Rs. ________/- _______ inclusive of all taxes or in the form MRP Rs. ______/- ______ incl. of all taxes after taking into account the fraction of less than 50 paise to be rounded off to the preceding rupee and the fraction of above 50 paise and up to 95 paise to the rounded off to 50 paise.

Un Quote

In other words, the packages of Commodity containing the quantity less than 25 Kg or Litres but more than 10 ML or 10 gm are covered under the said Rules except for Cement and Fertilizer for which Packaging is upto 50 Kg and Packaging Commodity meant for Industrial Consumers.

It is mandatory under Rule 6 of the said Rules to declare the MRP on each packages. Provisions of Rule 6 are given below :

Quote :

Rule 6 Declarations to be made on every package :

(1) Every Package shall bear thereon or on label securely affixed thereto, a definite, plain and conspicuous declaration made in accordance with the provisions of this chapter as to :

a. The name and address of the manufacturer, or where the manufacturer is not the packer, the name and address of the manufacturer and packer and for any imported packages the name and address of the importer shall be mentioned.

Explanation I : if any name and address of a company is mentioned o the label without any qualifying words “Manufactured by” or “Packed by”, it shall be presumed that such name and address shall be that of the manufacturer and the liability shall be determined accordingly.

Explanation II : If the Brand name and address of the brand owner appear on the label as a marketer, then the brand owner shall be held responsible for any violation of these rules and action as may be required shall be initiated against the deemed manufacturer and in the event of more than one name and address appearing in the label, prosecution shall be launched against the manufacturer indicated on the label in the first place and not against all of them.

Explanation III : In respect of packages containing food articles, the provisions of this sub-rule shall not apply and instead , the requirement of the prevention of Food Adulteration Act, 1954 (37 of 1954) and the rules made there under shall apply.

b. The common or generic names of the commodity contained in the package and in case of packages with more than one product, the name and number or quantity of each product shall be mentioned on the package

c. The net quantity in terms of the standard unit of weight or measure, of the commodity contained in the package or where the commodity is packed or sold by number of the commodity contained in the package shall be mentioned.

d. The month and year in which the commodity is manufactured or pre- packed or imported shall be mentioned in the package.

Provided that for packages containing food articles, the provisions of the Prevention of Food Adulteration Act 1954 (37 of 1954) and the rules made there under shall apply;

Provided further that nothing in this sub-clause shall apply in case of packages containing seeds which are labeled and certified under the provisions of the Seeds Act, 1966 (54 of 1966) and the rules made there under;

*Provided that a manufacturer may indicate the month and year using a rubber stamp without overwriting.

* Provisio will stand withdrawn wef 01.07.2012 vide GSR 748(E) dated 24.10.2011

Provided also that for packages containing cosmetics products, the provisions of the Drugs and Cosmetics Rules, 1945 shall apply.

(e) the retail sale price of the package;

Provided that for packages containing alcoholic beverages or spirituous liquor, the State Excise Laws and the rules made there under shall be applicable within the State in which it is manufactured and where the state excise laws and rules made there under do not provide for declaration of retail sale price, the provisions of these rules shall apply.

(f) Where the sizes of the commodity contained in the package are relevant, the dimensions of the commodity contained in the package and if the dimensions of the different pieces are different, the dimensions of each such different piece shall be mentioned.

(g) such other matter as are specified in these rules:

Provided that —

(A) no declaration as to the month and year in which the commodity is manufactured or pre- packed shall be required to be made on–

(i) any package containing bidis or incense sticks;

(ii) any domestic liquefied petroleum gas cylinder of 14.2kg or 5kg, bottled and marketed by a public sector undertaking;

(B) where any packaging material bearing thereon the month in which any commodity was expected to have been pre- packed is not exhausted during that month, such packaging material may be used for pre- packing the concerned commodity produced or manufactured during the next succeeding month and not there after, but the Central Government may, if it is satisfied that such packaging material could not be exhausted during the period aforesaid by reason of any circumstance beyond the control of the manufacturer or packer as the case may extend the time during which such packaging material may be used, and , where any such packaging material is exhausted before the expiry of the month indicated thereon, the packaging material intended to be used during the next succeeding month may be used for pre- packing the concerned commodity;

Provided that the said provision shall not apply to the packages containing food products, where the ‘Best before or Use before’ period is ninety days or less from the date of manufacture or packing.’

(C) no declaration as to the retail sale price shall be required to be made on

(i) any package containing bidi;

(ii) any domestic liquefied petroleum gas cylinder of which the price is covered under the Administrative Price Mechanism of the Government.

Explanation I: The month and the year in which commodity is pre- packed may be expressed either in words, or by numerals indicating the month and the year, or by both.

(2) Every package shall bear the name, address, telephone number, e mail address, if available, of the person who can be or the office which can be, contacted, in case of consumer complaints.

(3) It shall not be permissible to affix individual stickers on the package for altering or making declaration required under these rules:

Provided that for reducing the Maximum Retail Price (MRP), a sticker with the revised lower MRP (inclusive of all taxes) may be affixed and the same shall not cover the MRP declaration made by the manufacturer or the packer, as the case may be, on the label of the package.

(4) It shall be permissible to use stickers for making any declaration other than the declaration required to be made under these rules.

(5) Where a commodity consists of a number of components and these components are packed in two or more units, for sale as a single commodity, the declaration required to be made under sub-rule (1) shall appear on the main package and such package shall also carry information about the other accompanying packages or such declaration may be given on individual packages and intimation to that effect may be given on the main package and if the components are sold as spare parts, all declarations shall be given on each package

Competition Act was passed to protect the interest of consumers and the same was amended in 2007 and 2009. This is an act to establish a commission, protect the interest of the consumers and ensure freedom of trade in markets in India-

- To prohibit the agreements or practices that restricts free trading and also the competition between two business entities,

- To ban the abusive situation of the market monopoly,

- To provide the opportunity to the entrepreneur for the competition in the market,

- To have the international support and enforcement network across the world,

- To prevent from anti-competition practices and to promote a fair and healthy competition in the market.

However, this act also will not provide relief to the consumer. The anti-profiteering clause of new indirect taxation structure seems like ineffective with no powers. The government has not framed restrict rules or regulations under this, in fact, suo moto will do more research on the anti-profiteering provision of GST Regime.

As per the anti-profiteering rules, When the company or trader has asked or raised any query related to the undue profit by not providing the benefit of lower tax incidence because of GST than the query or complaint would be further passed to the standing committee which is appointed by the Council.

The committee will be decided whether the inquiry or complaint should further proceed or not. The new profiteering authority will do more research on complaint or inquiry, once when the committee approves. The complaint or inquiry report along with answers or advice will revert to the standing committee. The official further added that any penalty or action will be borne either by the Committee or the Council.

Currently, excluding Trai, all regulators and the Competition Commission of India (CCI) have the authority to impose punishment if in the case of any violation of a rule or a law. The GST anti-profiteering authority can be treated as the institution and it will not hold the same powers.

GST Council has nominated members to the state wise Anti-Profiteering Screening Committee. National Anti-Profiteering Authority have received the cabinet nod on 16th November 2017, especially on the background that in spite of reduction in tax rate of more than 200 items by 10% hardly any Manufacturer or Retailor or Service Providers have passed on the benefit. National Anti-Profiteering Authority is an assurance to the consumers of India and if any consumer feels that benefit of tax rate cut is not being pass on then he can file the complaint to the Anti-Profiteering Screening Committee. National Anti-Profiteering Authority consist of 5 members headed by Cabinet Secretary Shri. P K Sinha comprising Revenue Secretary Shri Hasmukh Adiya, CBEC Chairman Mrs. Vanja Sharma and Chief Secretaries of Two States. Chairman will be elected by these members. This body will function for 2 years from the date on which Chairman assumes the charges. Standing Committee will be at National level and all the complaints of national level will first go to these bodies and local level will go to Screening Committee. If those bodies find merit in the complaint, they can refer for further investigation to the Directorate General of Safeguards who will need to submit the report within 3 months to complete the investigation and send the report to Anti-Profiteering Authority. The Authority will decide on the methodology to evaluate if the benefit of lower taxes under GST including those arising due to seamless input tax credit have not been passed to the consumer.

Details of Anti-Profiteering Screening Committee of the State and Union territory are as per Annexure A.

A Government notification has now allowed such unsold pre- packed items to be marketed to consumers with an add-on sticker indicating the revised price. The old MRP will have to be clearly on display along with the revised MRP sticker. But from 1 October, all pre- packed goods will have to have just one MRP including the GST. Since, MRP is printed on the packages, it cannot be tampered with and therefore there has to be amendment in the Act relaxing to reduce MRP to the extent of reduction in tax rates. Otherwise, there will be a violation of Provisions of Legal Metrology Act.

Though rules have been framed, the methodology to work out and the benefit on account of reduction in tax Rate and seamless flow of credit has not been given. Therefore, there has to be a notification prescribing the formats of working out the benefit and mechanism to pass on the benefit. When GST was introduced, manufacturer have worked out the incremental ITC in GST Regime and pass on the benefit to the dealer but hardly any MRP was changed and therefore consumer have never got benefit, which was expected to get.

As NPPA has allowed us to increase MRP to adjust the additional Tax burden, there will be no impact on us as working results the same amount of PTR for the company as illustrated below:

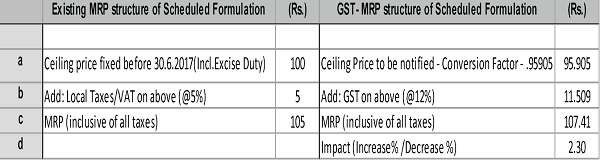

MRP of Scheduled Formulations- in case of schedule formulations, which are products from excise duty free zones, the revised ceiling price exclusive of applicable GST rates would be calculated by applying a factor of 0.95905 to the existing notified ceiling price. The factor has been worked out as follows :

As NPPA has allowed us to increase MRP to adjust the additional Tax burden , still there will be an impact on us as working results the different amount of PTR for the company as illustrated below:

It is very clear that PTR as on date is Rs. 80.00 which will be Rs. 76.72 resulting a reduction of 4.1% in PTR.

In case of schedule formulations, which are exempted from excise duty, no multiplication factor would be applicable. The existing notified ceiling price would be the ceiling price exclusive of GST rates as applicable.

| EXISTING: VAT & ED | GST @ 5% | |||

| CEILING PRICE | 100 | CEILING PRICE | 100 | |

| ADD VAT (@ 5%) | 5 | ADD GST (@5%) | 5 | |

| MRP (INCLUSIVE OF ALL TAXES) | 105 | MRP (INCLUSIVE OF ALL TAXES) | 105 | |

| EXCISE DUTY (6% ON 65% OF MRP) | 0.00 | |||

| MRP LESS E.D. LESS VAT = (A) | 100.00 | MRP LESS GST = (A) | 100.00 | |

| PTR EXCL ED (A*0.8) = (B) | 80.00 | PTR (A * 0.8) = (B) | 80.00 | |

| PTR (INCL ED) = B + E.D. | 80.00 | PTR (INCL ED) = B + E.D. | 80.00 | |

| PTS EXCL ED (B * 0.9) = C | 72.00 | PTS (B * 0.9) = (C) | 72.00 | |

| PTS (INCL ED) = C + E.D. = D | 72.00 | PTS (INCL ED) = C + E.D. = D | 72.00 |

Incremental benefit of additional Tax Credit can be ascertain based on the Bill of Material of the Product and credit available in earlier regime and GST Regime and thereafter work out the operational cost in GST Regime and add other cost of distribution and promotion to ascertain maximum retail price, which should include reduced GST rates and MRP needs to be reduced to that extent. Until such mechanism prevails, it will be very difficult to curtail the inflation.

It is very pertinent to note, the period prescribed for Screening Committee is 2 months and 3 months for the Directorate General of Safe Guards and thereafter decisions will be taken and hence whether this mechanism will help to reduce inflation on account of Anti-Profiteering, will be the Big Question Mark. However, value of goods or services or both should not include any taxes and then only seamless flow of credit will be pass on and consumer will bear GST at the rate notified by the Govt and the same will be reflected in the invoice. Then only the objective of Anti Profiteering will be truly achieved.

Details of Anti- Profiteering Screening Committee in States/UTs

CMA Ashok Nawal

Founder of Bizsolindia Services Pvt. Ltd.

Central Council Member of Institute of Cost Accountants of India

Email : nawal@bizsolindia.com

Author Bio