Government supplies under GST

Supplies made by Government to a business entity are generally covered in GST under the Reverse charge mechanism (RCM) basis. However, there is a twist to the tale wherein certain supplies are liable to GST under Forward charge mechanism (FCM) as well.

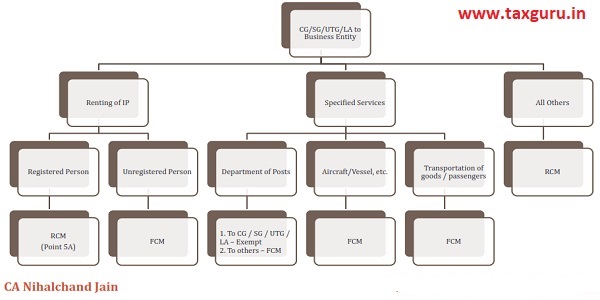

In this article, I would like to clarify Entry No. 5 and 5A of Notification No. 13/2017 dated 28th June 2017. The bare text is reproduced as under:

5. Supplies of Services by the Central Government, State Government, Union territory or local authority to a business entity, except –

(1) Renting of immovable property, and

(2) The services specified below-

(i) Services by the Department of Posts by way of speed post, express parcel post, life insurance, and agency services provided to a person other than Central Government, State Government or Union Territory or local authority;

(ii) Services in relation to an aircraft or a vessel, inside or outside the precincts of a port or an airport;

(iii) Transport of goods or passengers.

5A. Services supplied by the Central Government, State Government, Union territory or local authority by way of renting of immovable property to a person registered under CGST Act, 2017.

We now discuss the same, point by point:

1. Renting of Immovable Property:

When provided to a registered person, liable under FCM (Point 5).

When provided to an unregistered person, liable under RCM (Point 5A).

2. Department of Posts:

Speed Post, express parcel, etc.

a. Provided to CG/SG/LA – Exempt

b. Provided to Others – FCM

3. Aircraft/Vessel, etc. – FCM

4. Transportation of goods/passengers – FCM.

Also, find attached the same in a diagram form for quick reference.

Author Bio

I have plans to supply some Engineering items to Govt. what should I opt – RCM or FCM

what is the GST cess

Mr. Jain

you have written that:

1. Renting of Immovable Property:

When provided to a registered person, liable under FCM (Point 5).

When provided to an unregistered person, liable under RCM (Point 5A).

I think it should be:

1. Renting of Immovable Property:

When provided to a registered person, liable under RCM.

When provided to an unregistered person, liable under FCM.

Very good