Related Section & Rule:-

Section:- 61 Scrutiny of Returns.

Rule :- 99 Scrutiny of Returns.

What is GST ASMT-10:-

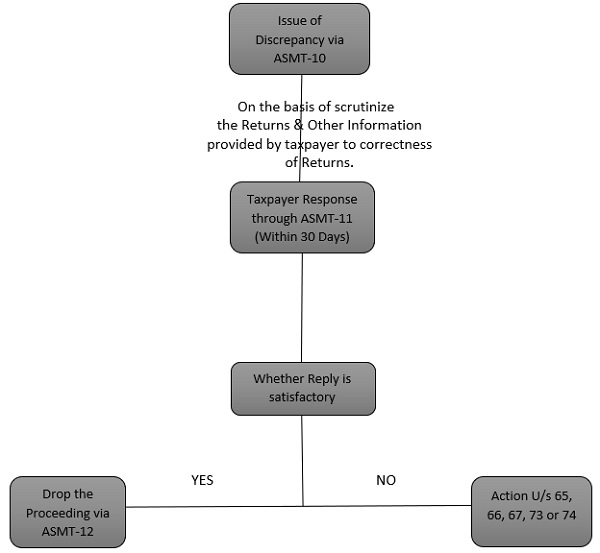

As per Section 61 read with Rule 99, a GST Officer is scrutinize the returns & related information furnished by the tax payer to verify the correctness of returns. If the assessment indicates a high risk of default or any indication of fraud, a scrutiny notice in the form of GST ASMT-10 is issued for seeking an explanation for the same. Tax Officer may indicate the same via SMS or Email registered with the department.

GST ASMT-10 is merely a notice where discrepancies are found and intimated to the taxpayers. Hence there is no personal hearing in ASMT-10.

ASMT-10 may specify the amount of tax, interest or any other amount payable by the taxpayer.

Content of ASMT-10:-

- Name, GST No. of Taxable Person & Tax Period for which discrepancies found.

- Details about discrepancies PARA wise.

- Details of the Tax officer issuing notice like Division, Zone, Final Desk.

Some of the most common discrepancies against which scrutiny notice can be issued are as follows:-

- Difference in Tax Liability reported in GSTR-1 and GSTR-3B

- Difference in ITC claimed in GSTR-3B and GSTR-2B/GSTR-2A

- Difference in Tax Liability as per E-Way Bill and GSTR-3B & GSTR1.

Response to ASMT-10:-

The taxpayer is required to file a reply within 30 days of its issuance via GST ASMT-11. However, on request of the tax payer officer may grant extension of not more than 15 days.

Response from Department:-

Scenario 1:-

Tax officer satisfied with the response of taxpayer and drop the proceeding & Intimate the same via ASMT-12 to taxpayer.

Scenario 2:-

Tax officer does not satisfy with the response of taxpayer and he may take appropriate action under Section 65, 66, or 67 and proceed to take action under section 73 or 74.

Section 65:- Audit by tax authorities.

Section 66:- Special Audit.

Section 67:- Inspection, search or seizure

Section 73:- Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized for any reason other than fraud or any wilful misstatement or suppression of facts.

Section 74:- Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilized for any reason of fraud or any wilful misstatement or suppression of facts.

There is no timeline for the issue of GST ASMT-12. The proceedings get concluded with the receipt of GST ASMT-12.

PROCESS:-

How to view Scrutiny Notice on Portal:-

GST Portal >> Services >> User Services >> View Additional Notices and Orders.

How to file a reply to ASMT-10:-

Scenario 1:-

Taxpayer agreed with the discrepancies and pay Tax, Interest, any other amount mentioned in ASMT-10 via DRC-03 and informed via ASMT-11.

Scenario 2:-

Taxpayer do not agree with the discrepancies noted. In such a case, he may provide explanation along with supporting documents to the Proper Officer via ASMT-11.

How to file a reply:-

- Select the ‘replies’ tab on the case details page.

- Click on ‘Notice’ to add a reply.

- Enter reply and payment details.

- Click on ‘ADD’ for more details.

- Choose a file to upload along with the reply.

- Check the verification checkbox and choose authorized signatory.

- Check details using the ‘Preview’ option and then click on ‘File’.

- Reply can be filed using EVC or DSC.

A success message will be generated on filing reply. The Replies tab will get updated to show “Reply Furnished, pending with Tax Officer.”

Recommendation:-

Even though no physical presence is required but it is advisable to submit all the documents along with reply in GST ASMT-11 with the proper officer manually also to be on safer and explain the case. The reason being that the taxpayer can be convincing regarding his arguments while explaining the relevant facts and circumstances.

Summary:-

Author Bio