Office of the

Commissioner of State Tax,

(GST), Maharashtra State,

8th floor, GST Bhavan,

Mazgaon, Mumbai-400010.

TRADE CIRCULAR

To,

No. JC/HQ-I/GST/Refund/2017-18/01/ADM-08 Mumbai,

Date 21st Feb. 2018

Trade Cir. No. 8 T of 2018

Subject : Manual filing and processing of claim of refund of inverted tax structure and deemed exports.

Ref. : (1) Order of Distribution of cases No. 1/2017-GST/Maharashtra dated the 22nd November 2017.

(2) CBEC Circular No. 14/14/2017-GST dated 6th November 2017.

(3) Trade Circular No. 49T of 2017 dated the 28th November 2017

(4) Trade Circular No. 52T of 2017 dated the 11th December 2017.

(5) CBEC Circular No. 24/24/2017-GST dated 21st December 2017.

(6) Trade Circular No. 1T of 2018 dated 1st January 2018.

Sir/Gentlemen/Madam,

1. Background:

1.1. Your attention is invited towards the Trade Circular No. 49T of 2017, 52T of 2017 and 1T of 2018 cited at Ref. (3), (4) and (6) above. These Trade Circular(s) explain the procedure for manual filing and processing of refund claims related to zero-rated supply of goods or services or both and refund of excess balance in electronic credit ledger.

1.2. As explained earlier, due to the non-availability of the refund module on the common portal, it has been decided, on the recommendations of the Council, that the applications /documents /forms pertaining to refund claims on account of inverted tax structure and deemed exports shall be filed and processed manually till further orders. In this regard, the undersigned, in exercise of powers conferred under section 168 (1) of the Maharashtra Goods and Services Tax Act, 2017 (hereinafter referred to as the “MGST Act”) hereby clarifies that the contents of the Trade Circular No. 49T of 2017 and Trade Circular No. 52T of 2017 [cited at Ref. (3) and (4) above] shall also be applicable to the refund claims on account of inverted tax structure and deemed exports inasmuch as they pertain to the method of submission of refund claim and its processing which is consistent with the relevant provisions of the MGST Act, 2017 and Maharashtra Goods and Services Tax Rules, 2017 (hereafter referred to as the “MGST Rules”).

2. Periodicity of submission of refund application:

2.1. It is clarified that refund claims on account of inverted tax structure and deemed exports shall be filed for a tax period on a monthly basis in FORM GST RFD-01A. In order to avoid the delay in grant of refund the Trade is advised to file the application for refund only after return in FORM-GSTR-1 is filed.

2.2. However, in case of registered taxable person having aggregate turn-over upto Rs. 1.5 Cr. in the immediately preceding financial year or, in the current financial year and who opts to file GSTR-1 quarterly (Notification No. 57/2017 (State Tax) dated the 15th November 2017 shall apply for refund on quarterly basis. In such cases where tax payer has opted to file GSTR-1 quarterly then the refund application shall be filed only after submission of GSTR-1 for that period.

3. Applicability of this Trade Circular:

3.1. The procedure and methodology laid down in this Trade Circular

shall be applicable to the claim of refund pertaining to the inverted

tax structure and deemed export.

3.2. The Trade Circular is divided into two parts as given below:

| Sr. No. | Particulars | Nature of Refund |

| 1. | PART-A

|

Refund of unutilised input tax credit on account of inverted tax structure. |

| 2. | PART-B

|

Refund of tax on account of supply of goods regarded as Deemed Export. |

PART-A

REFUND OF UNUTILISED INPUT TAX CREDIT ON

ACCOUNT OF INVERTED TAX STRUCTURE:

1. Eligibility to claim refund under this category:

1.1. The refund application under this category shall be filed in the cases where the credit has accumulated on account of rate of tax on inputs being higher than the rate of tax on output supplies (other than nil rated or fully exempt supplies).

1.2. The registered persons applying for refund shall give an undertaking to the effect that the amount of refund sanctioned would be paid back to the Government with interest in case it is found subsequently that the requirements of clause (c) of subsection (2) of section 16 read with sub-section (2) of sections 42 of the MGST Act have not been complied with in respect of the amount refunded.

1.3. This undertaking should be submitted manually along with the application in FORM GST RFD-01A.

1.4. The application (in FORM GST RFD-01A) for refund in such cases shall accompany the Statement-1 and 1A. The format is given in the latter part of this Trade Circular.

1.5. The refund of accumulated credit on account of rate of tax on inputs being higher than rate of tax on output supplies shall be available except in following circumstances,-

(a) supplies of goods as notified in Notification No.: 5/2017 State Tax (Rate) dated 29th June 2017 as amended by Notification No. 29/2017 State Tax (Rate) dated the 25th September 2017 and Notification No. 44/2017 dated the 14th November 2017.

(b) supplies of services as notified in Notification No. 15/2017-State Tax (Rate) dated 29th June 2017. [Construction Services: Point 5(b) Schedule II]

1.6. As per the provisions of section 54(3)(ii) the aforesaid categories of supplies of goods or services are barred from seeking refund of the un-utilized or accumulated inputs.

2. Preparation of Application for Refund:

2.1. The registered taxable person who desires to get the refund on account of inverted tax structure is required to file an application manually in FORM GST RFD-01A (as notified in the MGST Rules vide Notification No. 55/2017 –State tax dated 15.11.2017 and as amended from time to time). All the details in the said form is to be filled appropriately.

2.2. The applicant who desires to get the aforesaid refund shall access the common portal i.e. www.gst.gov.in and fill the appropriate details, of claim of refund, in in Statement-1 made available on the common portal with the use of appropriate Log-in Id and password.

2.3. The process flow diagram is given below:

Login Id>password>Services>Refund> Application for Refund> >Select the refund type>select from drop-down the month>select Create application>fill the application>submit the application at GSTN portal> take print out>submit the printout to designated GST Officer.

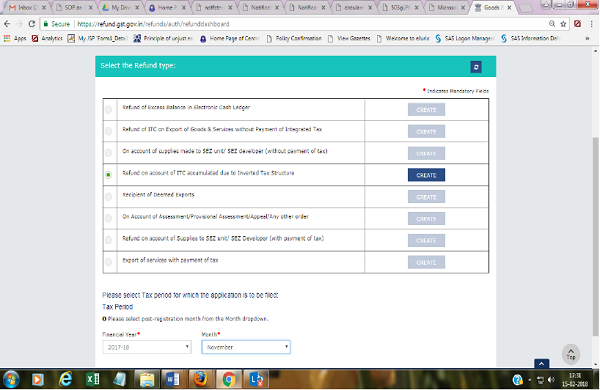

2.4. After log-in the tax payer shall use option Services>“Application for refund” available at the common portal. The applicant would be directed to next screen which would appear as given below:

2.5. This screen displays the list of Refund Type(s). From the said list select the type of refund as “Refund on account of ITC accumulated due to Inverted Tax Structure” and then press the “CREATE” button displayed in front of the said row.

2.6. This will take the applicant to the next screen where the following will appear.

Refund on account of ITC accumulated due to Inverted Tax Structure

Kindly enter values in statement 1 below for the Tax Period for which Refund is being claimed:

Computation of Refund to be claimed

Statement 1

ITC accumulated due to inverted tax structure

[Clause (ii) of first proviso to section 54(3)]

| Tax | Turnover of inverted rated supply of goods (1) |

Tax payable on such invertedrated supply of goods(2) |

Adjusted total turnover (3) |

Net input tax credit

(4) |

Maximum Refund amount to be claimed (5) [(1×4÷3)-2] |

| Integrated tax |

|||||

| Central Tax | |||||

| State/UT tax |

|||||

| Cess |

2.7. As it appears from the above table i.e. Statement-1, the details of turnover of supply inverted tax structure of goods is to be filled in column (1) above. The said turnover of inverted tax structure supply of goods may be taken from appropriate column of FORM-GSTR-3B/GSTR-1. The appropriate figures of Net input tax credit (ITC) in column (4) from the FORM-GSTR-3B may be taken.

2.8. The applicant is also required to determine the output tax liability on account of supply of such inverted tax rated goods. The output liability so determined is to be filled in the column (2) above Statement-1.

2.9. Once the information as stated above is filled then the figures in column (3) above i.e. of adjusted turn-over is required to be determined as given in rule 89(4) of the MGST Rules. After entering the requisite information as explained above the refund amount will get auto calculated as given in the Column (5) above.

2.10. The formula used to calculate the Maximum Refund Amount is given below:

Maximum Refund Amount= [(Turn-over of inverted rated supply of Goods) X Net ITC/Adjusted Total Turn-over]-Tax payable on such inverted rated supply of goods.

2.11. It is to be kept in mind that the term “Net ITC” and “Adjusted Total Turnover” shall have the same meaning as assigned to it in rule 89(4) of the MGST Rules, 2017.

2.12. For better understanding same is re-produced below:

Where,-

(B) “Net ITC” means input tax credit availed on inputs and input services during the relevant period other than the input credit availed for which the refund is claimed under sub-rule (4A) and 4(B) or both;

(E) “Adjusted Total turnover” means the turnover in a State or a Union territory, as defined under clause (112) of section 2, excluding,-

(a) the value of exempt supplies other than zero-rated supplies and

(b) the turn-over of supplies in respect of which refund is claimed under sub-rule (4A) and 4(B) or both, if any. during the relevant period.

2.13. After entering the appropriate figures in the above table i.e. Statement-1, the amount of refund will get auto populated in the column (5) of the said TABLE.

2.14. Further, there is another TABLE below the Statement-1 (at GSTN portal>refund tab) where the amount of eligible refund will get auto calculated as also the amount of refund claim. The said TABLE appears on the GSTN portal as given below. The figures in this TABLE are auto populated.

| Value As per Statement-1 in Rs. |

Balance in Electronic Credit Ledger in Rs. |

Tax Credit availed during the period in Rs. |

Eligible Refund amount (Lowest of all) | |

| (1) | (2) | (3) | (4) | |

| Integrated tax | ||||

| Central tax | ||||

| State tax | ||||

| Cess |

2.15. The system compares the value of refund amount calculated as per Statement-1, the Balance available in the Electronic Credit Ledger and the Net ITC availed during the period for which the refund application is created. The lowest of these three values is calculated as eligible refund amount. The final amount eligible for refund is given in the column (4) above under each Act i.e. MGST, CGST, IGST and Cess.

2.16. Apart from duly entering the appropriate information the applicant is also required to select from drop-down the Bank Account Number given in the application for registration.

2.17. In case, an applicant desires to get the refund amount in another preferred bank account which is not appearing in the drop down list then applicant is requested to add that bank account with the use of amendment functionality available at GSTN portal i.e. non-core amendment. For this purpose, the applicant, may go the >Registration>Non-core amendment> and add details including Bank Name, Branch Name, IFS Code. The facility given for choosing the Bank IFSC may be used so that no error is made while entering said information. Once the Bank details gets updated at GSTN portal then the refund amount determined as per the provisions of the law will be disbursed and credited to the said preferred Bank account. This is absolutely essential in order to ensure that the refund is credited to the appropriate bank account as desired by the applicant.

(1) It may please be noted that,-

(a) Once the applicant has entered all the details in Table i.e. Statement-1 above please save the form before you proceed to Submit.

(b) Please correct any errors occurred during preparation and do not forget to save the said FORM before proceeding to submit.

(c) It may please be kept in mind that once “Proceed” button is clicked and form is submitted, no modification will be allowed. Therefore due care may please be taken before pressing the “Proceed” button.

(d) The Electronic Credit ledger balance visible here is the current balance in the Electronic Credit ledger.

(e) Application can be saved at any stage of completion for a maximum time period of 15 days. If the same is not submitted within 15 days from the date of form creation, the saved draft will be purged from the GST database.

The applicant after 15 days may follow the same procedure for creation and submission of refund Application in FORM-RFD-01A.

(2) Needless to say that the applicant shall first discharge the outstanding liability, if any, in respect of IGST, CGST, SGST and cess as also the recovery of the dues (under the MVAT, CST Act, Luxury Tax etc.) not stayed by the appellate forum and then only seek the refund on account of inverted rated supply of goods.

(3) It may also be noted that the amount claimed as refund is subject to recovery of the dues, if any, by the department. Hence, the applicant is advised to discharge the aforesaid outstanding liability at the earliest.

2.18. UPLOAIDNG OF THE INFORMATION IN STATEMENT-1 REALTED TO REFUND OF INVERTED TAX STRUCTURE AT GSTN PROTAL:

(1) Once the aforesaid steps are followed and application is saved then the message as “Saved successfully” will appear at the top left hand side of the Table. After doing so the “PROCEED” button will get activated. Press the said button. You will be taken to the next window, where, after checking the Box for declaration. The applicant is required to submit the said application with the EVC or, as the case may be, Digital Signature Certificate (DSC), whichever is applicable.

(2) After successful submission, the amount of eligible refund as stated in the column (4) of the TABLE above will get debited from the Electronic Credit Ledger and ARN receipt will be generated. As the Eligible Refund Amount calculated at the GSTN portal gets debited from the Electronic Credit Ledger, therefore, due care should be taken, this will enable the Department to process the refund application in given time period.

2.19. SUBMISSION OF REFUND APPLICATION IN FORM-RFD-01A:

2.19.1. The printout of the ARN receipt generated at common portal shall be submitted to the appropriate authority as explained below.

2.19.2. The cases which are assigned to the State vide order of distribution of tax payer cited at Ref. (1) above, the application in FORM-GST-RFD-01A complete in all respect alongwith ARN receipt generated at common portal the printout of the same shall be submitted to the appropriate Official in the office of the concerned Joint Commissioner of State tax and in case, the office of the Joint Commissioner of State tax, does not exist then to the head of the location. The location wise list where the application is to be submitted is given in the ANNEXURE-B of the Trade Circular No. 49 of 2017 dated 28th November 2017.

2.19.3. The tax payer who is neither assigned to the State Tax Authority nor to the Central Tax Authority and who desires to submit the application for refund to the MGSTD, then under such circumstances, the refund application shall be accepted,-

(i) in case the registered place of business of the said tax payer is situated in Brihan Mumbai, then in the Office of the Joint Commissioner of State tax (MUM-VAT-F-001), Nodal-1, 5th Floor, “E-Wing”, New Building, GST Bhavan, Mazgaon, Mumbai-400010.

(ii) at Pune location, in the office of the Joint Commissioner of State tax (PUN-VAT-F-001), 201, 2nd Floor, Off. Golf Club, Air Port Road, Yerawada, Pune-411006.

(iii) at the location other than Brihan Mumbai and Pune in the office of the Joint Commissioner of State tax where such office exists and in any other case in the office of the head of the location.

2.20. STATEMENTS TO BE ATTACHED AND UNDERTAKING TO GIVEN WITH REFUND APPLICATION FORM-GST-RFD-01A:

(1) After preparation of application and Statement-1 for refund as above, the applicant shall prepare the Statement-1A as given in rule 89(2)(h) of the MGST Rules, 2017 and attach the same with the refund application. The said statement contains the details of invoices of inward supplies received and tax paid on inward supplies as also the details of invoices of outward supplies issued and tax paid on outward supplies.

(2) The details of inward supplies invoice number date, value and tax on inputs and corresponding details of outward supplies made.

(3) The Statement as given below shall be filled correctly and completely.

Statement-1A [rule 89(2)(h)]

Refund Type: ITC accumulated due to inverted tax structure [clause (ii) of first proviso to section 54(3)]

| Sr. No. | Details of invoices of inward supplies received |

Tax paid on inward supplies | Details of invoices of outward supplies issued |

Tax paid on outward supplies |

||||||||

| (1) | No.

(2) |

Date

(3) |

Taxab le Value(0) |

Integrated Tax (0) | Central Tax

(1) |

State/ Union Territor y Tax(1) |

No.

(0) |

Date

(1) |

Taxab le Value(2) |

Integr ated Tax(3) |

Centr al Tax

(4) |

Stat e/U nion Terri tory Tax

(0) |

(4) The applicant shall also furnish the appropriate undertakings and declarations as given in the FORM-GST-

RFD-01A (Format for the same is given in the latter part of this Trade Circular).

2.21. RECEIPT OF REFUND APPLICATION:

(1) As explained above, the application shall be submitted to the Office of the Joint Commissioner of State tax and in case the office of the Joint Commissioner does not exist then to the head of the Location. The details of the locations and authority responsible for receipt of refund applications are given in the ANNEXURE-B annexed to the Trade Circular No. 49T of 2017 cited at Ref. (3) above. It is informed that the applicant shall submit the application in FORM-RFD-01A in duplicate so that the suitable receipt of the application is given.

(2) After receipt of the application, the concerned authority will verify that the application is in order and requisite details as given in this Trade Circular are attached. After it is found that the application is in order and the refund ARN printout is enclosed then a receipt will be given by putting appropriate stamp and date of receipt of the application.

(3) If it is noticed that the particular tax payer is not assigned to that Nodal Division or the LTU division then the applicant may be directed to submit application to appropriate jurisdiction. 2.22.

2.22. ACKNOWLEDGEMENT FOR REFUND OF APPLICATION:

(1) The application received in the concerned office of the Joint Commissioner of State tax or, as the case may be, head of the location shall be forwarded to the concerned Nodal officer on the same day or in any case not later than next working day.

(2) After receipt of the application, the concerned Nodal officer shall verify the debit entry made in the Electronic Credit Ledger and verify that the refund claimed is commensurate to the amount so debited. Nodal Officer shall also verify the liability outstanding, if any, under of the MGST Act and shall first adjust it and remaining amount of refund, if any, may be processed as per the provisions of the MGST Act. As explained above, the outstanding liability which is not stayed by the Appellate forum pertaining to the existing law shall also be adjusted against the refund remaining, if any.

(3) Once the completeness in all respect is ascertained an acknowledgment in FORM-RFD-02 as given in Rule 90(1) of the MGST Rules, shall be issued within 15 days from the date of submission of application.

(4) In case the application so submitted is found deficient in certain aspects then the concerned officer shall issue deficiency memo in FORM-RFD-03 within 15 days from the date of receipt of the application.

(5) In other words, the concerned officer after due verification is required to issue either FORM-RFD-02 or FORM-RFD-03 not later than 15 days from the date of receipt of application. All the supervisory authorities are hereby directed to monitor that these timelines are strictly followed.

2.23. ISSUANCE OF DEFICIENCY MEMO IN CASE OF REFUND OF APPLICATION IS DEFICIENT:

(1) As explained above, in case an application for refund is deficient then the Deficiency Memo should be issued. It should be complete in all respects and only one Deficiency Memo shall be given. Submission of application after Deficiency Memo shall be treated as a fresh application. Re-submission of the application, after rectifying the deficiencies pointed out in the Deficiency memo, shall be made by using the same ARN and debit entry number generated originally.

(2) It shall be kept in mind that as of now, there is no provision at the GSTN portal to again create and submit the application for refund and generate the ARN and submit the application at GSTN portal after removal of deficiencies.

(3) If the application is not filed afresh within thirty days of the date of receipt of communication of the deficiency memo, the concerned Nodal officer shall pass an order in FORM GST PMT-03 and re-credit the amount claimed as refund through FORM GST-RFD-01B.

PART-B

REFUND OF TAX ON SUPPLY OF GOODS REGARDED

AS DEEMED EXPORTS:

1. The State Government, on recommendations of the GST Council has in exercise of the power conferred under section 147 of the Maharashtra Goods and Services Tax Act, 2017 issued a notification (Finance Department Notification No. 48/2017 dated 18th October 2017) and notified the supplies that is to be treated as Deemed Exports.

2. Accordingly following supplies of goods have been regarded as deemed export:

2.1. Supply of goods by a registered person against Advance Authorisation;

2.2. Supply of capital goods by a registered person against Export Promotion Capital Goods Authorisation;

2.3. Supply of goods by a registered person to Export Oriented Unit;

2.4. Supply of gold by a bank or Public Sector Undertaking specified in the notification No. 50/2017-Customs, dated the 30th June, 2017 (as amended) against Advance Authorisation.

3. Evidences required to be produced by the supplier of deemed export supplies for claiming refund:

3.1. The State Government has also issued a notification (Finance Department Notification No. 49/2017 dated 18th October 2017) and notified the evidences that are required to be produced by the supplier of deemed export supplies claiming refund. These evidences are as given below:

| S. No. | Evidence |

| (1) | (2) |

| 1. | Acknowledgment by the jurisdictional Tax officer of the Advance Authorisation holder or Export Promotion Capital Goods Authorisation holder, as the case may be, that the said deemed export supplies have been received by the said Advance Authorisation or Export Promotion Capital Goods Authorisation holder, or a copy of the tax invoice under which such supplies have been made by the supplier, duly signed by the recipient Export Oriented Unit that said deemed export supplies have been received by it. |

| 2. | An undertaking by the recipient of deemed export supplies that no input tax credit on such supplies has been availed of by him. |

| 3. | An undertaking by the recipient of deemed export supplies that he shall not claim the refund in respect of such supplies and the supplier may claim the refund. |

3.2. As stated above, the State Government has issued aforesaid notifications and notified certain supplies to be deemed export. Further third proviso to rule 89(1) of the MGST Rules, 2017 allows the recipient or supplier to file the application for refund under this category. In other words the refund on account of Deemed Export may be claimed either by the supplier or by the recipient of the Deemed Export supplies.

3.3. In case such refund is sought by the supplier of deemed export supplies, the documentary evidences as specified in Notification No. 49/2017-as stated above, are also required to be furnished which includes an undertaking by the recipient of deemed export supplies that he shall not claim the refund in respect of such supplies and that no input tax credit on such supplies has been availed of by him.

3.4. The undertaking should be submitted manually along with the refund application in FORM-GST-RFD-01A.

3.5. Similarly, in case the refund is filed by the recipient of deemed export supplies, an undertaking by the supplier of deemed export supplies that he shall not claim the refund in respect of such supplies is also required to be furnished manually.

3.6. However, it may please be kept in mind that at present the GSTN portal has provided the facility to submit the refund applications under this category by the recipient of the of deemed export supplies only.

3.7. As and when the GSTN portal make available the facility to claim refund by the supplier of the deemed export, the application for refund in this behalf may be made by the supplier subsequently, provided that the recipient has not filed the applications for refund.

3.8. The procedure regarding procurement of supplies of goods from DTA by Export Oriented Unit (EOU) / Electronic Hardware Technology Park (EHTP) Unit / Software Technology Park (STP) Unit / Bio-Technology Parks (BTP) Unit under deemed export as laid down in Circular No. 14/14/2017-GST dated 06.11.2017 issued by the CBEC needs to be complied with.

4. PREPARATION OF REFUND APPLICATION AT GSTN PORTAL.

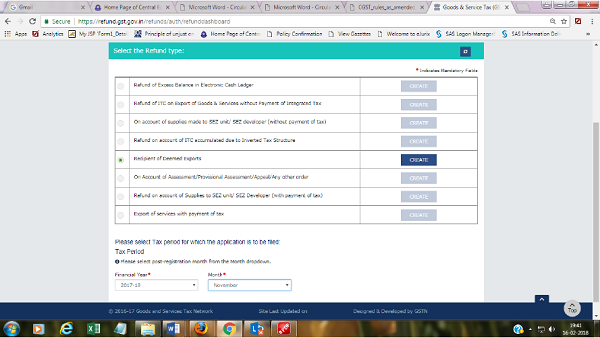

4.1. As explained above, the applicant shall access the GSTN portal

with the use of Log-in ID and password and create the applications for refund under the category of Recipient of Deemed Export supplies.

4.2. Select the month for which the refund is requested. The screen shot of the said template is given below:

4.3. After pressing the CREATE button the following screen will appear. The applicant is required to fill the details appropriately. The screen will appear as under:

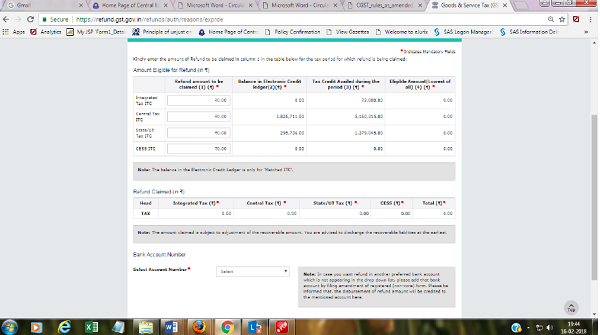

4.4. The requisite information is to be filled in the TABLE given below:

Amount Eligible for Refund (in Rs.)

TABLE-1

| Refund amount to be claimed |

Balance in Electronic Credit ledger |

Tax Credit Availed during the period |

Eligible Amount (Lowest of all) | |

| (1) | (2) | (3) | (4) | |

| Integrated Tax ITC | ||||

| Central Tax ITC |

||||

| State/UT Tax ITC | ||||

| CESS ITC |

Refund Claimed (in Rs.)

TABLE-2

| Head | Integrated Tax |

Central Tax | State/UT Tax |

CESS | Total |

| TAX |

Note: The amount claimed is subject to adjustment of the recoverable amount. You are advised to discharge the recoverable liabilities at the earliest

4.5. The applicant once enters the figure of the amount of refund to be claimed, in column (1) of TABLE-1 above, the figures in column (2), (3) and (4) of the said TABLE-1 gets auto populated.

4.6. After filling the appropriate information and submission of applications at GSTN portal the ARN receipt gets generated.

4.7. The amount refund claimed under each Act will be shown in TABLE-2 above.

5. STATEMENTS TO BE ATTACHED AND UNDERTAKING TO BE GIVEN WITH REFUND APPLICATION-GST-RFD-01A:

5.1. The application shall be accompanied by a statement 5B of the FORM-GST-RFD-01A as given below.

5.2. It shall contain details of invoices of outward supplies if the

refund is claimed by the supplier and the details of invoices of

inward supplies in case refund is claimed by the recipient. 5.2.1. It should also contain the details of the taxable value and the

taxes paid thereon.

Statement-5B [rule 89(2) (g)

Refund Type: On account of deemed exports

| Sr. No. | Details of invoices of outward supplies in case refund is claimed by supplier/Details of invoices of inward supplies in case refund is Claimed by recipient | Tax paid | |||||

| (1) | No.

(2) |

Date

(3) |

Taxable Value

(4) |

Integrat ed Tax

(5) |

Central Tax

(6) |

State/Union TerritoryTax(7) |

Cess

(8) |

6. The applicant seeking refund on account of Deemed Exports shall prepare application for refund as given in the Para-2 above. The procedure in relation to uploading of refund application, its submission, issuance of defect memo, re-submission of application after correcting defects to the Nodal Authority etc. shall be applicable as it applies to the seeking refund for inverted tax structure. For this please refer Para-2 above which pertains to the refund on account of inverted rated supply.

7. DECLARATIONS AND UNDERTAKING TO BE SUBMITTED WITH REFUND APPLICATION IN FORM-GST-RFD-01A:

7.1. The applicant who desires to the claim the refund under different categories as given under section 54 in general and particularly with regards to the refund on account of inverted tax structure and deemed export shall submit the requisite declaration and the undertaking as given in the FORM-GST-RFD-01A.

7.2. The details are given as under;

DECLARATION [ second proviso to Section54(3)]

I hereby declare that the goods exported are not subject to any export duty,

I also declare that I have not availed any drawback on goods services or both and that I have not claimed refund of the integrated tax paid on supplies in respect of which refund is claimed.

Signature

Name-

Designation/Status

DECLARATION [Section 54(3) (ii) ]

I hereby declare that the refund of ITC claimed in the application does not include ITC availed on goods or services used for making ‘nil’ rated or fully exempt supplies.

Signature

Name-

Designation/Status

[ DECLARATION [rule 89(2)(g)]

( For recipient /supplier of deemed export )

In case refund claimed by recipient □

I hereby declare that the refund has been claimed only for those invoices which have been detailed in statement 5B for the tax period for which refund is being claimed and the amount does not exceed the amount of input tax credit availed in the valid return filed for the said tax period. I also declare that the supplier has not claimed refund with respect to the said supplies.

In case refund claimed by supplier □

I hereby declare that the refund has been claimed only for those invoices which have been detailed in statement 5B for the tax period for which refund is being claimed and the recipient shall not claim any refund with respect of the said supplies and also, the recipient has not availed any input credit on such supplies.

Signature

Name

Designation/Status

DECLARATION

[rule 91(1)]

I/ We———————–(Applicant) having GSTIN/temporary Id—————————,solemnly affirm and declare I/We———————-have not been prosecuted for any offence under the Act or under an existing law where the amount of tax evaded exceeds two hundred and fifty lakh, during any period of five years immediately preceding the tax period for which the claim of refund relates.

Signature

Name

Designation/Status]

UNDERTAKING

I hereby undertake to pay back to the Government the amount of refund sanctioned along with interest in case it is found subsequently that the requirements of clause (c) of sub-section (2) of section 16 read with sub-section (2) of section 42 of the CGST/SGST Act have not been complied with in respect of the amount refunded

Signature

Name

Designation/Status]

SELF-DECLARATION [RULE 89(2(1))

I/ We_______(Applicant) having GSTIN/temporary Id_ _ _ _, solemnly affirm and certify that in respect of the refund amounting to Rs. _ _ _/with respect to the tax, interest, or any other amount for the period from_ _ _to_ _ _, claimed in the refund application, the incidence of such tax and interest has not been passed on to any other person.

Signature

Name-

Designation/Status

(This Declaration is not required to be furnished by applicants, who are claiming refund under clause (a) or clause (b) or clause (c) or clause(d) or clause (f) of sub-section (8) of section 54.)

VERIFICATION

I/we< Taxpayer Name> hereby solemnly affirm and declare that the information given herein above is true and correct to the best of my/our knowledge and belief and nothing has been concealed therefrom.

I/we declare that no refund on this account has been received by me/us earlier.

Place

Date

Signature of Authorised

Signatory

(Name)

Designation/ Status

8. In order to process the refund smoothly and to avoid delay the applicant is requested to provide the soft copy of the Statement-1A (Inverted tax structure) or Statement 5B (Deemed Exports) whichever is applicable. This will enable the officer to quickly cross-check the details of the inward supply and outward supply as also the tax paid on such supplies.

9. It is reiterated that the procedure laid down in earlier Trade Circular No. 49T of 2017 dated 28th November 2017 and Trade Circular No. 52T of 2017 dated 11th November 2017 shall be followed so far it relates to the Grant of Provisional Refund, Final Refund, adjustment of outstanding recovery etc. rejection of the refund and re-credit of the refund so rejected and time limit for the same.

10. The registered persons applying for refund under aforesaid categories shall give an undertaking to the effect that the amount of refund sanctioned would be paid back to the Government with interest in case it is found subsequently that the requirements of clause (c) of subsection (2) of section 16 read with sub-section (2) of sections 42 of the MGST Act have not been complied with in respect of the amount refunded. This undertaking should be submitted manually along with the refund claim till the same is available in FORM GST RFD-01A on the common portal.

11. In case the refund application is found in order then the applicant shall receive the due refund in the Bank account available in the registration record with common portal.

12. Needless to state that any refund amount which the applicant is not entitled or has claimed wrongly or inappropriately then it shall be recovered along with the interest or may face prosecution for the serious breach of the provisions of the MGST Act.

13. This circular is clarificatory in nature and cannot be made use of for interpretation of provisions of law. If any member of trade has any doubt, he may refer the matter to this office for further clarification.

Yours faithfully,

(RAJIV ALOTA)

Commissioner of State Tax (GST) Maharashtra State, Mumbai.

No. JC/HQ-I/GST/Refund/ 2017-18/01/ADM-08

Trade Cir. No. o8 T of 2018

Mumbai, Date 21/02/2018

Copy forwarded for information to,

(1) The Joint Commissioner of State Tax, (MAHAVIKAS) with a request to upload this Trade circular on MSTD web-site.

(2) Deputy Secretary, Finance Department, Mantralaya, Mumbai.

(3) Accounts Officer, Sales Tax Revenue Audit, Mumbai and Nagpur.

(Vilas Indalkar)

Additional Commissioner Of S ate Tax (GST 2),

Mazgaon, Mumbai