Introduction: Corporate guarantees play a vital role in financial transactions, offering security for lenders. However, within the realm of Goods and Services Tax (GST), their implications and applicability have been subject to scrutiny. This article provides comprehensive insights into corporate guarantees within the GST sphere.

Page Contents

- 1. What is Corporate Guarantee?

- 2. Corporate Guarantee VS Bank Guarantee

- 3. GST applicability on Corporate Guarantee

- 4. Corporate Guarantee by Indian Holding Company to Foreign Subsidiary Company

- 5. Corporate Guarantee by Foreign Holding Company to Indian Subsidiary Company

- 6. Eligibility of Input Tax Credit

1. What is Corporate Guarantee?

A Corporate Guarantee is a guarantee, in which a corporate, agrees to be responsible for the financial obligations of, or the performance of contractual obligations by the principal debtor to the creditor, in the event the principal debtor fails to discharge his obligation to the creditor. These transactions usually include intra-group corporate guarantees amongst related parties in a group entity.

A corporate guarantee serves as a financial backup for lenders. It offers assurance that if the borrower defaults on their loan obligations, the guarantor—typically a company—will step in to fulfil those responsibilities. This backup arrangement mitigates the lender’s risk and provides them with a layer of protection against potential losses.

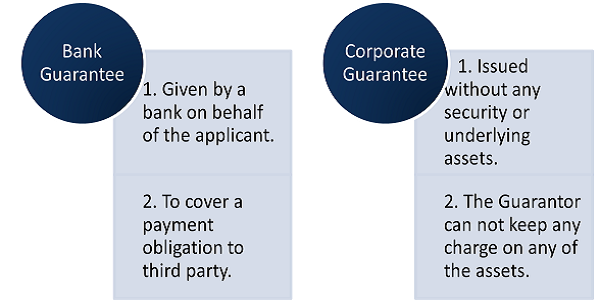

2. Corporate Guarantee VS Bank Guarantee

> Bank Guarantee is a guarantee given by a bank on behalf of the applicant to cover a payment obligation to a third party.

> Corporate guarantees are issued without any security or underlying assets. But unlike a loan where you give something as backup, like your car for a car loan, with a corporate guarantee, there’s no such backup. So, if the guarantee is needed, the company making the promise has to pay up without asking for anything from the other company.

3. GST applicability on Corporate Guarantee

The confusion surrounding how GST affects corporate guarantees has now been resolved and clarified by the insertion of sub-rule (2) in Rule 28 of the Central Goods and Services Tax Rules, 2017 vide Notification No. 52/2023 – Central Tax dated 26.10.2023 pursuant to the recommendations of the 52nd Goods and Services Tax Council meeting held on 07.10.2023 which prescribes the value of corporate guarantees to be 1% of the guarantee amount or actual consideration, whichever is higher.

Analyzing the rule in detail, it indicates that GST is levied on Corporate Guarantees, the provision guides us to determine the Value of Supply as 1% of the amount of such guarantee offered, or the actual consideration, whichever is higher.

4. Corporate Guarantee by Indian Holding Company to Foreign Subsidiary Company

In this case the question arises whether the supply is treated as “Export of Services” or not. To answer the same, we should refer the definition of the “Export of Services”.

∴ Section 2(6) of IGST Act, 2017 defines “export of services” as the supply of any service when :-

1. The supplier of service is located in India;

2. The recipient of service is located outside India;

3. The place of supply of service is outside India;

4. The payment for such service has been received by the supplier of service in convertible foreign exchange or in Indian rupees wherever permitted by the Reserve Bank of India and

5. The supplier of service and the recipient of service are not merely establishments of a distinct person in accordance with Explanation 1 in section 8

In this situation, there are two scenarios: if the payment for the service has been received, it can be considered as an export of services, and the Holding company can avoid GST liability if it has a Letter of Undertaking (LUT). However, if the payment hasn’t been received, it can’t be classified as an export of services, and the Holding company would be liable to pay GST.

5. Corporate Guarantee by Foreign Holding Company to Indian Subsidiary Company

When a parent company outside India provides a guarantee for a loan taken by its subsidiary in India, it’s considered an ‘import of services’ under GST. According to Notification No. 10/2017- Integrated Tax (Rate), the Indian entity is required to pay the GST on a reverse charge basis for such imported services. If the Indian subsidiaries haven’t been paying GST under reverse charge for these guarantees until October 26, 2023, they need to review and calculate the GST liability based on Rule 28(1) and pay it under reverse charge. For transactions after October 26, 2023, the valuation follows Rule 28(2), and the GST liability still needs to be paid on a reverse charge basis.

6. Eligibility of Input Tax Credit

Where the services of issuance of corporate guarantee is used by the registered entity (subsidiary company) for the purpose of taxable supplies, then input tax credit will be eligible and if the service is used for exempt supplies, then the input tax credit will be ineligible. In case the services of corporate guarantee are considered as common services (applicable when both taxable and exempt supplies are made by the subsidiary company), only the proportionate Input Tax Credit relevant to taxable supplies will be considered eligible.

Conclusion: Corporate guarantees, while fundamental in financial transactions, undergo specific GST treatment. Understanding their GST implications is crucial for entities involved in domestic and international transactions to ensure compliance and manage tax liabilities effectively. These insights provide clarity on navigating the GST landscape concerning corporate guarantees.

****

Authors: Sachin Ostwal | Associate Consultant | Email: blogs@bilimoriamehta.com | Contact: +91 98709 25375, +91 99305 98581

Author Bio

What about the taxability on corporate guarantees prior to 26/10/2023. If it is taxable, on what value?