Rule 36(4) of CGST Rules

Input tax credit to be availed by a registered person in respect of invoices or debit notes, the details of which have not been uploaded by the suppliers under sub-section (1) of section 37, shall not exceed 20 per cent of the eligible credit available in respect of invoices or debit notes the details of which have been uploaded by the suppliers under sub-section (1) of section 37.

Do Not take 20% of ITC Availed in GSTR 3B

Exclusions –

1. ITC on Imports of Goods & Services – 3A1 & 3A2 of GSTR 3B

2. ITC on RCM – 3A3 of GSTR 3B

3. ITC on ISD Invoices – 3A4 of GSTR 3B

Do Not Even take 20% of ITC Availed in 3A5 – All Other ITC

Exclusions from 3A5 : All Other ITC

1. ITC on inward supplies of Goods from SEZ – However Services Received from SEZ are eligible

2. Reclamation of ITC after reversal invoking 2nd provisio to Sec 16(2)

3. Excess reversal of ITC restored back under Rule 42(2) after final calculation

4. ITC travelling directly to Credit ledger like through ITC-01, ITC02, TRAN-1, TRAN-2 and TRAN-3 is also outside the purview of Rule 36(4)

| Month for which return is filed | Eligible ITC available in Purchase register | Remarks | |

| Invoice Dated | ITC Eligible in GSTR-2A | ||

| Month for which return is filed : Apr’19 to Sep’2019 | |||

| Apr’19 to Sep’2019 | 100 | 200 | The entire 200 has been availed till Sep’19 |

| Month for which return is filed : Oct’19 | |||

| Oct’19 | 80 | 300 – consisting of the following-

a. 200 for Apr’19 to Sep’19 |

– 20 has already been availed till Sep’19. Hence it has to be excluded first |

| Apr’19 to Sep’2019 | 20 | 120% of 80 = 96 can be availed for Oct’19 | |

| Month for which return is filed : Nov’19 | |||

| Nov’19 | 70 | 400 – consisting of the following- a. 200 for Apr’19 to Sep’19 b. 100 for Oct’19 c. 100 for Nov’19 |

– 20 has already been availed till Sep’19. Hence it has to be excluded first |

| Oct’19 | 20 | What to Avail –

1. 120% of 70= 84? 2. [120% of 70 = 84 ] + [balance of Oct’19 (20-16) i.e. 4] = 88 ? 3. [120% of 90] = 108? 4. [120% of 170] – 96 = 108 SUBJECT TO 104. But System Has No Way To Track This Anomaly. But Interest Liability May Be There During Assessment |

|

| Apr’19 to Sep’2019 | 20 | ||

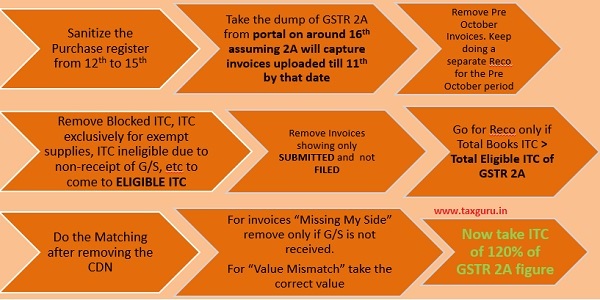

Process to be Followed Month on Month

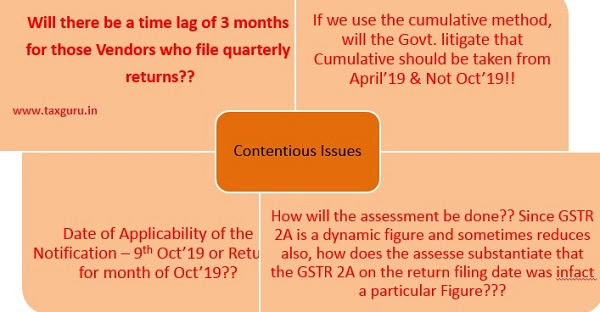

Contentious Issues