Understand the new Electronic Credit Reversal and Re-claimed Statement in GST for efficient ITC reversal and re-claim. Learn about reporting, amending, and validating opening balances, with a deadline and amendment limitations. Stay compliant, reduce errors, and enhance transparency. Check your Electronic Credit Reversal and Re-claimed Statement on the GST portal for accurate ITC claims.

The Goods and Services Tax (GST) regime has introduced a new electronic statement for taxpayers to reverse and re-claim input tax credit (ITC). The statement, called Electronic Credit Reversal and Re-claimed Statement, is a statement that shows the ITC claimed, reversed and re-claimed by the taxpayers during the specific return period.

The purpose of this statement is to simplify the process of ITC reversal and re-claim, and to reduce the errors and mismatches that may arise in the regular returns. The statement is generated on the basis of the information furnished by the suppliers in their GSTR-3B returns. The taxpayers can view and download the statement from the GST portal.

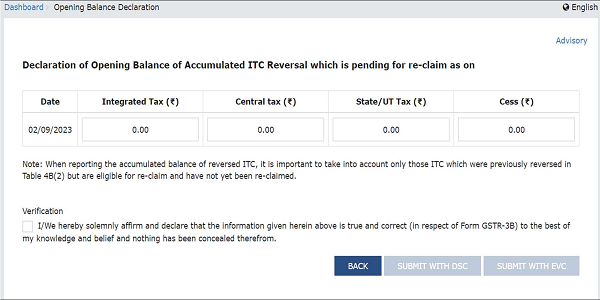

The statement presents information obtained from Table 4A(5)-All other ITC Claimed, Table 4B(2)- ITC reversed which can are re-claimable and Table 4D(1)-ITC reclaimed, of form GSTR-3B. Taxpayers are required to report opening balance of Re-claimable ITC reversed during earlier periods till 30th November, 2023. Option to report opening balance will be removed from the portal after 30th November 2023, and it will be assumed that the taxpayer has no ITC reversal balance to report.

The taxpayers will have the option to amend the reported Opening balance until 31st December 2023, Any reported balance after this date will be considered final and cannot be further amended. After 31st December 2023, the updated value shall be frozen with no further attempts provided to the taxpayers to amend their ITC Reversal Balance and this ITC Reversal value will be sent to the Jurisdictional Tax Officer for review. Due diligence should be done while reporting/amending the ITC reversal opening balance, because only 3 time amendment is allowed.

The opening balance that has been reported or amended by the taxpayers shall be credited to the “Electronic Credit Reversal and Re-claimed Statement”. This statement will be used to validate the taxpayer’s ITC Re-claimed amount in Table 4A(5) & 4D(1) of form GSTR-3B. The Closing Balance section of the statement will indicate the remaining amount of ITC Reversal balance that can be claimed again in form GSTR-3B.

The introduction of Electronic Credit Reversal and Re-claimed Statement is expected to bring more transparency and accuracy in the ITC reversal and re-claim process. It will also help in reducing the compliance burden and litigation issues related to ITC reversal and re-claim. The taxpayers are advised to check their Electronic Credit Reversal and Re-claimed Statement regularly and take appropriate actions to avail the correct amount of ITC.

Author Bio