The ferocity of the novel COVID-19 virus has not been abated yet and the Nation as a whole has come together to fight against it. The virus not only impacted the health and life of the people but to the economy as a whole. Many governments and private offices and organizations are functioning with 50% of its manpower. The government has also taken various liberal reforms to promote ease of business in this pandemic situation.

Department of Revenue, Ministry of Finance, Central Board of Direct Taxes, New Delhi, Vide Notification No. 35/2020-Income Tax//F.No. 370142/23/2020-TPL dated 24.06.2020, the due date for filing the tax audit report had been extended up to 31.10.2020 and that for filing the returns of income up to 30th November 2020.

Subsequent to this The Ministry of Corporate Affairs also granted a major relief to All the Companies by granting an extension of 3 months of Holding Annual General Meeting (AGM) for the F.Y. ending 31.03.2020.

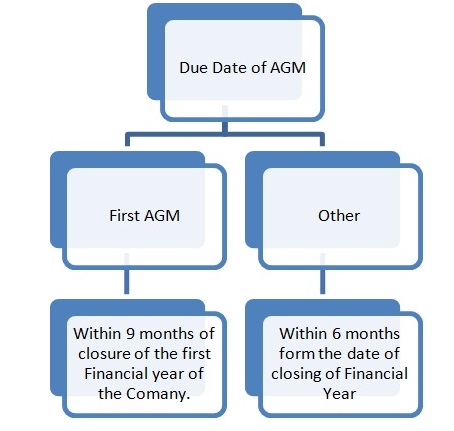

Existing Provision on AGM under section 96(1) of Companies Act, 2013

♦ Every company other than OPC shall in each year hold in addition to any other meeting, a general meeting as its annual general meeting, and shall specify the meeting as such in the notices calling it.

♦ The gap between the Two AGM shall not exceed 15 months.

♦ The due date of AGM are as follows

For Example:

If the first financial year of any company is closed on 31.03.2020, then the last date until the company needs to convene AGM is 31.12.2020 i.e. 9 months from 31.03.2020.

In the case of companies whose financial year ends as on 31.03.2020, the last date till the company needs to convene AGM is 30.09.2020 i.e. 6 months form 31.03.2020.

♦ The Registrar of Companies may, if application made in e-form GNL-1 for special reason may extend the due date for any AGM except First AGM for a period not exceeding 3 months.

AGM Due date Extension Granted to Companies

Earlier Last month the MCA issued a Clarification letter stating that those companies who are finding it difficult to hold AGM may apply with their ROC on or before 29th September 2020, in form GNL-1 for seeking an extension of holding AGM. But many companies find it difficult to get approval from ROC and made representation to MCA to grant a general relief.

Subsequent to which MCA granted the following reliefs:

♦ The time within which the AGM of the F.Y. ended 31.03.2020 (i.e. 30.09.2020) has been extended for 3 months from the due date from which the AGM ought to be held without the filing of E-form GNL-1.

For Example: if the due date of holding AGM of any company is 30.09.2020 then a general extension of 3 months is granted and it can hold its AGM till 31.12.2020.

♦ This extension is not for the first AGM of any company. Therefore still the last date for holding 1st AGM of any company is 9 months from the closure of the first financial year.

For Example: if the first financial year of any company is closed as on 31.03.2020 then the last date to hold AGM is 31.12.2020 it should not be taken as 31.03.2021.

♦ The extension shall cover all the pending applications filed in form GNL- 1 for extension of AGM for the F.Y. ending 31.03.2020, which are yet to be approved.

FAQs on AGM Due Date Extension

1. Is there required to file a separate GNL-1 for the general extension?

NO, there is no requirement to file any separate GNL-1 for the extension. It shall be deemed to have been granted an extension of 3 months for all the companies.

2. If any prior approval for the extension is granted via. E-form GNL-1 for a term less than 3 months then what shall be the last date to hold AGM?

It shall be deemed that the extension was granted for 3 months revoking the earlier extension.

3. Whether any refund will be granted for any earlier approved GNL-1 file?

No, there shall be no refund to be granted.

4. Is Extension for all types of Companies?

The Extension is granted to all types of Companies except OPC.

5. Whether the gap between 2 AGM can extend for more than 15 months?

NO, as per the sub-section (1) of section 96 of the Companies Act, 2013 that not more than 15 months shall be elapsed between the date of One AGM of a company, and that of the Next AGM.

Let’s take 2 examples

i. In case the last AGM of ABC Pvt. Ltd. held on 30.09.2019 then the due to hold AGM shall be 31.12.2020 as the Gap between the Two AGM is of 15 months.

ii. In case if the last AGM of the ABC Pvt. Limited held on 30.07.2020 then the due date to hold AGM shall be 30.10.2020 (12 months + 3 months)

Therefore the time Gap between the Two AGM shall not exceed 15 months in any case.

Author Bio

Dear Sir,

Time gap can be exceed 15 months in extension case.

For FY 1819, if the company has filed for extension and held the agm on 30/12/19, then what will be due date for AGM in FY 1920?

I am astonished to See date 31/09/2020. Please re draft

Item no. 5, you are wrong. Please read the section throughly before writing your opinion.

The date is extended by 3 months so the due dates as per Section 96(1) has been extended and it will cover gap period also so the gap may be more than 15 months

Dear Sir,

Since the AGM is not applicable for One Person Company, whether any extension is given to them or they still have to file their annual report within 180 days from the end of the financial year?

Also, is there any extension for LLPs where the turnover is above 40 Lakhs and Audit is applicable as per LLP Act?

Regards

CA Sumit Anshani

Sir, Power has been assigned to ROC by virtue of third proviso to section 96(1) for extension of three months in excess of 15 months.

Dear Sir,

Time gap can be exceed 15 months in extension case.

Thank You Mukul Ji

For Updating in such a great way.

Please mention the relevant Notification No. with date. There is no official notification as yet. There had been instances that Notifications do not match the assurances in GST and probably in MCA also.