Objective of the Standard:-

♦ Ind AS 41, Agriculture is the first standard that specifically covers the Accounting and Reporting requirements for the Primary sector. Prior to this standard, there were no established guidance on Agriculture and Allied Industry.

♦ This standard introduces a Fair Value model to Agriculture accounting which is a major shift away from the traditional cost model widely applied in Primary Industry.

♦ This standard sets out the Accounting for Agricultural activity, the management of the Transformation of biological assets into Agricultural produce.

Scope:-

a) Biological Assets

i. Living Animals- Ind AS 41

ii. Plant

- Bearer Plant- Ind AS 16

- Other than Bearer Plant- Ind AS 41

b) Agricultural Produce

i. At the point of Harvest- Ind AS 41

ii. Harvested- Ind AS 2

c) Government Grant

i. Related to Living Animal- Ind AS 41

ii. Related to Bearer Plant – Ind AS 20

iii. Related to Plant other than Bearer Plant- Ind AS 41

d) Land related to Agricultural Activity- Ind AS 16

e) Intangible Asset related to Agricultural Activity- Ind AS 38

Terms to be Understood:-

a) Agricultural Activity:-

Refers to Management by an Entity of Biological Transformation and harvest of Biological Asset for:-

i. Sale

ii. Conversion into Agricultural Produce

iii. Conversion into Additional Biological Asset (Calf from Cow)

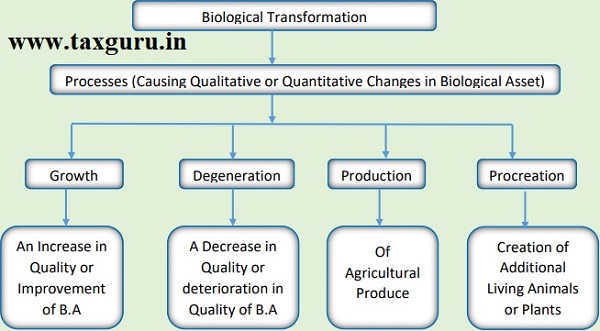

b) Biological Transformation:-

Comprises of

a. Process of Growth; Degeneration; Procreation; Production

b. That causes changes in Qualitative or Quantitative of Biological Asset

c) Agricultural Produce:-

Means which is a Harvested product of the Entity’s Biological asset.

d) Harvest:-

e) Biological Asset:-

Is defined as a Living Animal and Plant (Including Bearer Plant)

f) Bearer Plant:-

a. Is a plant that is used in the production or supply of Agricultural produce

b. Expected to bear produce for more than One Period

c. Has a remote likelihood of being sold as Agricultural produce, except for Incidental Scrap Sales.

g) Fair Value:-

Is the price that would be received to sell an Asset or paid to transfer a Liability in an Orderly transaction between the Market Participants at the Measurement date (As per Ind AS 113)

Recognition of Biological Asset:-

Biological assets are recognized as an Asset when and only when All the following conditions are satisfied:-

i. Entity has Control of such Asset.

ii. It is Probable that Future Economic benefits will flow to the Entity

iii. Fair Value or Cost can be measured reliably.

Measurement of Biological Asset:-

a) For Biological Asset:

a. At Initial Recognition:

Fair Value[1] less Cost to Sell

b. At Subsequent Recognition (@ Measurement Date):

Fair Value less Cost to Sell

Example:

Situation 1: When Biological Asset is Acquired:-

| 01-04-2019 | 31-03-2020 | 31-03-2021 | 31-03-2022 |

- On 01-04-2019, date of acquisition of an Biological Asset @ 1000/- (Cost Price)

- Now Initial recognition in books of accounts will be @ Fair Value less cost to sell

- Cost to sell 100/- (say)

- Initial recognition will be at (1000-100) = 900/-

- Now on 31-03-2020, i.e. on subsequent measurement recognition in books of account will be as follows:

- Suppose Fair value on 31-03-20 is 1100/-; cost to sell is 100/-

- This increase in fair value less cost to sell i.e. 100/-(1000-900) is transferred to Profit & Loss A/c.

Situation 2: When Biological Asset is Produced:–

I.e. Additional Biological Asset is produced from the Original Biological Asset (Calf from Cow)

| 01-04-2019 | 31-03-2020 | 31-03-2021 | 31-03-2022 |

- On 01-09-2019, date when additional biological asset is born will be measured at Fair Value less Costs to Sell

- In this case no cost is incurred, so will be measured at fair value less cost to sell

- Entire fair value is transferred to Profit & Loss A/c. as Gain.

- Now on subsequent measurement any change in fair value is transferred to P&L A/c.

Exception to above:

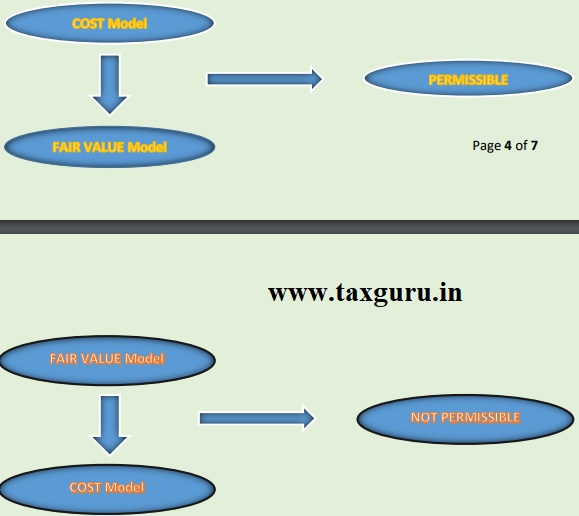

- If Fair value of Biological asset cannot be measured reliably, then it will be measured at

| Particulars | Amount |

| Cost of Asset | |

| (-) Accumulated Depreciation | |

| (-) Accumulated Impairment Loss | |

| Carrying Amount |

Note:-

- Once fair value of such biological asset becomes measurable then it shall be measured @ Fair Value less Cost to Sell.

2) Cost may Approximate to FAIR VALUE in the following situations:-

♦ There is a little Biological Transformation since the Date of Acquisition.

Ex: – Newly acquired Biological Asset immediately before Reporting date

On 26-03-2020, purchased a Cow and is recognized @ 100/- (Fair Value less Cost to Sell) and on 31-03-2020 still the Cow Fair value will be 100/- (FVCS)

♦ Biological Transformation impact on PRICE is very less or insignificant throughout its life.

Ex: – Pine Plantation Life cycle (Used for decoration only)

Measurement of Agricultural Produce:-

- Measured @ Fair Value less Costs to Sell (FVCS) at the Point of Harvest

- This FVCS will become COST Price for applying IND AS 2

Government Grant:-

Disclosures:-

1) General Disclosures:-

♦ Entity shall disclose the Aggregate Gain/Loss arising in Current Period

– On Initial Recognition

– From changes in Fair Value less Cost to sell on subsequent recognition of Biological Asset & Agricultural Produce.

| Particulars | Amount |

| Carrying Amount as the year Beginning | |

| (+) Purchases during the year | |

| (-) Sales during the Year | |

| (+/-) Gain/Loss due to changes in FVCS | |

| (-) Decrease in Fair Value due to Harvest | |

| Carrying Amount as the year End |

Entity shall present a Reconciliation statement of changes in Carrying Amount of Biological Asset:

2) Additional Disclosures:-

If Biological Assets are measured at COST Model then the following disclosures are required to be given:

i. Description of such Biological Asset

ii. Explanation why Fair value cannot be determined

iii. Depreciation method used

iv. Useful life of Biological asset and Depreciation rate

3) Government Grant:-

i. Nature and Extent of amount of Government Grant recognized.

ii. Any unfulfilled conditions attached.

Notes:

[1] Measured as per Ind AS 113 Fair Value Measurement

Author Bio