Saurabh Chhabra

STUDENTS GUIDE TO GST

Relevant for Nov 2017 Exams (CA-Final and CA-Inter)

The Hon’ble Chairman of BOS Shri Atul Kumar Gupta Ji has announced in the webcast on 25th May 2017, that ICAI will ask questions on GST in Nov 2017 Exams as well for 10 marks to test the basic knowledge of GST. ICAI has yet to announce the coverage, but I believe that it will not go beyond the coverage in this document. Best of Luck!!

Chapter 1

Introduction and Constitutional Amendments

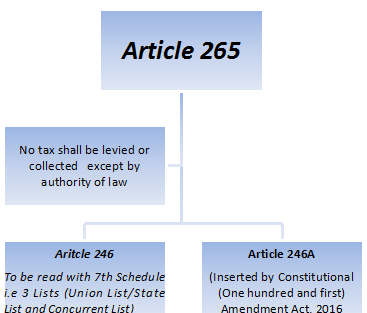

The Article 246 of Constitution of India read with schedule VII (3 Lists i.e Union List, State List and Concurrent List) provides for the division of taxation powers between the center and states. Currently, indirect taxes are imposed on goods and services. These include excise duty by center, sales tax by states, service tax by center, octroi and entry tax by states, customs duty by center etc. For taxes imposed by states, the tax rates may vary across different states.

The concept of Value Added Tax (VAT) was introduced for central excise duty (first as MODVAT and then as CENVAT). Prior to this, excise duty was levied on both inputs used and the output produced. This meant that an amount paid as tax on the input was subject to taxation again at the output level (with limited set offs). This was applicable to each intermediate good in the manufacturing process. This “tax on tax” led to cascading of taxes. This problem was sought to be addressed by the VAT regime under which tax paid on the inputs is deducted from the tax payable on the output produced. Similarly, sales tax also had a cascading effect through the distribution chain. All states have now adopted the concept of VAT for state sales tax. The issue of cascading taxation was partly addressed through the VAT regime. However, certain problems remained. For example, several central and state taxes were excluded from VAT. Further, goods and services were taxed differently, thereby making the taxation of products complex. Some of these challenges are sought to be overcome with the introduction of the Goods and Services Tax (GST).

The comprehensive GST regime intends to subsume most indirect taxes under a single taxation regime. In India GST will be value added tax levied across goods and services by both center and state on a common base. This is expected to help broaden the tax base, increase tax compliance, and reduce economic distortions caused by inter-state variations in taxes.

GST in India required Constitutional amendment

Currently, fiscal powers between the Center and the States are clearly demarcated in the Constitution with almost no overlap between the respective domains. The Center has the powers to levy tax on the manufacture of goods (except alcoholic liquor for human consumption, opium, narcotics etc.) while the States have the powers to levy tax on sale of goods. In case of inter-State sales, the Center has the power to levy a tax (the Central Sales Tax) but, the tax is collected and retained entirely by the originating States. As for services, it is the Center alone that is empowered to levy service tax. Since the States are not empowered to levy any tax on the sale or purchase of goods in the course of their importation into or exportation from India, the Center levies and collects this tax as additional duties of customs, which is in addition to the Basic Customs Duty. This additional duty of customs (commonly known as CVD and SAD) counter balances excise duties, sales tax, State VAT and other taxes levied on the like domestic product. Introduction of GST would require amendments in the Constitution so as to concurrently empower the Centre and the States to levy and collect the GST.

The assignment of concurrent jurisdiction to the Center and the States for the levy of GST would require a unique institutional mechanism that would ensure that decisions about the structure, design and operation of GST are taken jointly by the two. For it to be effective, such a mechanism also needs to have Constitutional force.

Constitution (One Hundred and First) Amendment Act, 2016

To address all these and other issues, the Constitution (122nd Amendment) Bill was introduced in the 16th Lok Sabha on 19.12.2014. The Bill provides for a levy of GST on supply of all goods or services except for Alcohol for human consumption. The tax shall be levied as Dual GST separately but concurrently by the Union (central tax- CGST) and the States (including Union Territories with legislatures) (State tax- SGST)/ Union territories without legislatures (Union territory tax- UTGST). The Parliament would have exclusive power to levy GST (integrated tax- IGST) on inter-State trade or commerce (including imports) in goods or services. The Central Government will have the power to levy excise duty in addition to the GST on tobacco and tobacco products. The tax on supply of five specified petroleum products namely crude, high speed diesel, petrol, ATF and natural gas would be levied from a later date on the recommendation of GST Council.

A Goods and Services Tax Council (GSTC) shall be constituted comprising the Union Finance Minister, the Minister of State (Revenue) and the State Finance Ministers to recommend on the GST rate, exemption and thresholds, taxes to be subsumed and other features. This mechanism would ensure some degree of harmonization on different aspects of GST between the Center and the States as well as across States. One half of the total number of members of GSTC would form quorum in meetings of GSTC. Decision in GSTC would be taken by a majority of not less than three-fourth of weighted votes cast. Center and minimum of 20 States would be required for majority because Center would have one-third weight age of the total votes cast and all the States taken together would have two-third of weight age of the total votes cast.

The Constitution Amendment Bill was passed by the Lok Sabha in May, 2015. The Bill was referred to the Select Committee of Rajya Sabha on 12.05.2015. The Select Committee had submitted its Report on the Bill on 22.07.2015. The Bill with certain amendments was finally passed in the Rajya Sabha and thereafter by Lok Sabha in August, 2016. Further the bill had been ratified by required number of States and received assent of the President on 8th September, 2016 and has since been enacted as Constitution (101st Amendment) Act, 2016 w.e.f. 16th September, 2016.

Analysis of Constitutional Amendment bill, 2016

The GST Bill provides for the following changes in the existing Constitution of India

> Deletion of 1 Article

> Amendment of 10 Articles

> Amendment of 2 Schedules

> Insertion of 3 new Articles

♦ Article 246A: Special provision creating legislative competence to levy Goods and Services Tax

♦ Article 269A: Levy and collection of Goods and Service tax in the course or interstate trade and commerce

♦ Article 279A: Goods and Service Tax Council

Analysis of above amendments is as follows:

> Dual GST: Both the Center and States given concurrent powers to levy GST

> IGST: Center given exclusive powers to levy GST on supplies in the course of inter State trade and commerce and imports into India

> Taxable event will be supply: GST defined as any tax on supply of goods and services other than on alcohol for human consumption

> Center empowered to formulate rules for the Place of Supply

GST shall subsume various indirect taxes being levied by the Union and the State governments (Refer Point vii & viii below in the salient features of GST)

Taxing powers currently not merged in GST and therefore to continue with the Union or State as the case may be:

> Excise duty on petroleum products (Union) – To be merged in GST as per the recommendation of GST Council

> Tax on sale of petroleum products (State) – To be merged in GST as per the recommendation of GST Council

> Tax on alcoholic liquor for human consumption (State)

> Tax on entertainment and amusement levied and collected by Panchayat/Municipality/ Regional Council/ District Council

> Stamp Duties

Following Non- GST Taxes will continue to be levied by Center and State

Central ‘Non- GST’ Taxes

> Entry 83- Duties of customs including export duties(usually referred to as Basic Customs Duty)

> Entry 89- Terminal taxes on goods or passengers, carried by railway, sea or air; taxes on railway fares and freights

> Entry 90- Taxes other than stamp duties on transactions in stock exchanges and futures markets

> Entry 92A- Taxes on the sale or purchase of goods other than newspapers, where such sale or purchase takes place in the course of inter-State trade or commerce

> Entry 92B- Taxes on the consignment of goods (whether the consignment is to the person making it or to any other person), where such consignment takes place in the course of inter State trade or commerce

State ‘Non- GST’ Taxes

> Entry 49- Taxes on lands and buildings

> Entry 53- Taxes on the consumption or sale of electricity

> Entry 56- Taxes on goods and passengers carried by road or on inland waterways

> Entry 57- Taxes on vehicles, whether mechanically propelled or not, suitable for use on roads, including tramcars subject to the provisions of entry 35 of List III

> Entry 59- Tolls

> Entry 60- Taxes on professions, trades, callings and employments

> Entry 63- Rates of stamp duty in respect of documents other than those specified in the provisions of List I with regard to rates of stamp duty

Benefits of GST (Why GST)

> It would mitigate cascading or double taxation in a major way and pave the way for a common national market.

> The biggest advantage would be in terms of a reduction in the overall tax burden on goods, which is currently estimated around 30 Percent.

> Introduction of GST would also make Indian products competitive in the domestic and international markets.

> It would instantly spur economic growth

> This tax, because of its transparent character, would be easier to administer

Salient Features of GST

The salient features of GST are as under:

(i) Supply would be the Taxable event:GST would be applicable on supply of goods or services as against the present concept of tax on the manufacture of goods or on sale of goods or on provision of services(Refer Section 7 of CGST Act, 2017)

(ii) Destination Based Taxation:Consuming state will gain due to this shift from origin based taxation to destination based taxation; Parliament shall by law, on recommendation of GST council, provide for compensation to states for loss of revenue arising on account of implementation of GST upto 5 years as per clause 18 of the constitutional (One hundred and First) amendment Act, 2016

(iii) Dual Taxing Structure: The new Article 246A intends to grant concurrent powers to the Union and state legislatures to make laws with respect to GST. The power to make laws in respect of supplies in the course of inter-state trade or commerce will be vested only in the Union Government. States will have the right to levy GST on intra- state transactions including services.It would be a dual GST with the Center and the States simultaneously levying it on a common base. The GST to be levied by the Center would be called Central GST (CGST) and that to be levied by the States would be called State GST (SGST)

(iv) Integrated GST (IGST):It would be levied on inter-State supply (including stock transfers) of goods or services. This would be collected by the Centre so that the credit chain is not disrupted

(v) BCD + IGST on Imports of Goods:Itwould be treated as inter-State supplies and would be subject to IGST in addition to the applicable customs duties (BCD)

(vi) IGST on Import of Services:Import of services would be treated as inter-State supplies and would be subject to IGST.

(vii) Rates Schedule Released by GST Council :In the 14thMeeting of GST Council held in Srinagar on 18th and 19th May 2017, Council has released the consolidated rates of GST for 1211 Goods and 568 Services Classified under 124 Groups of 32 Headings under 5 Sections (5 to 9)

|

Goods |

Services |

| 6 Slab Rates will be applicable on Taxation of Goods under GST i.e. 0%, 5%, 12%, 18%, 28% and 28% + Compensation Cess | 4 Slab Rates will be applicable on Taxation of Services under GST i.e. 5%, 12%, 18% and 28% |

| Nothing recommended under Reverse charge yet for Goods | 13 Services are placed under Reverse charge Mechanism |

| Exemption List yet to be released for Goods | 83 Services are placed under Exemption List (Broadly Negative List and Exemption List of Service Tax merged with few changes) |

| HSN Codes will be used to classify the goods (HSN Codes released)* | SAC Codes will be used to classify the Services (SAC Codes released)* |

*Here is an important update on HSN/ SAC under Indian GST Regime (On Every Invoice under GST Regime– These codes needs to be provided, further while registering for GST we need to register for these codes)

The HS code consists of 6-digits. The first two digits designate the HS Chapter. The second two digits designate the HS heading. The third two digits designate the HS subheading. HS Nomenclature beyond 6 digits is also allowed and some countries have extended Six Digit Code to Eight Digit Code and India is also one such country which use Eight Digit Code

In Indian Context, a taxpayer having a turnover exceeding Rs 5 crore is required to follow the HSN code of 4 digits. In return form, rate of tax shall be auto populated based on the HSN codes used in furnishing invoice level purchase or sale information. After completing first year under GST, the turnover for previous year will be considered as baseline for using HSN codes of 4 digits.

Indian authorities have further categorized six digit HSN into another two digit sub chapter, thus making total number of digit to be eight. This eight digits code will be mandatory in case of export and imports under the GST regime

(viii) Central taxes that would be subsumed within the GST

> Central Excise duty (Entry 84)

> Duties of Excise (Medicinal and Toilet Preparations) (Entry 84)

> Additional Duties of Excise (Goods of Special Importance) (Entry 84)

> Additional Duties of Excise (Textiles and Textile Products) (Entry 84)

> Additional Duties of Customs (commonly known as CVD) (Entry 83)

> Special Additional Duty of Customs (SAD) (Entry 83)

> Service Tax (Entry 92C)

> Cesses and surcharges insofar as far as they relate to supply of goods or services (Article 271)

(ix) State taxes that would be subsumed within the GST

> State VAT (Entry 54)

> Central Sales Tax (Entry 54)

> Purchase Tax (Entry 54)

> Luxury Tax (Entry 62)

> Entry Tax (All forms) (Entry 52)

> Entertainment Tax (not levied by the local bodies) (Entry 62)

> Taxes on advertisements (Entry 55)

> Taxes on lotteries, betting and gambling (Entry 62)

> State Cesses and surcharges insofar as far as they relate to supply of goods or services

(x) Potable Alcohol Excluded: GST would apply to all goods and services except Alcohol for human consumption (Constitutional Exclusion)

(xi) Petroleum products also excluded for the time being: GST on petroleum products would be applicable from a date to be recommended by the Goods & Services Tax Council in terms of clause 5 of Article 279A

(xii) Tobacco and tobacco products:They would be subject to GST. In addition, the Center could continue to levy Central Excise duty (Excise duty + GST)

(xiii) No more entry tax & octroi: There is a provision to remove imposition of entry tax/ Octroi across India

(xiv) Entertainment tax: The tax imposed by states on movie, theater, etc., will be subsumed in GST, but taxes on entertainment at panchayat, municipality or district level will continue

(xv) GST on Sale of Newspaper and advertisements: GST is likely to be levied on the sale of newspapers and advertisements and this will give the Government access to substantial incremental revenues

(xvi) Stamp Duties will continue: Stamp duties, typically imposed on legal agreements by the state, will continue to be levied by the states

(xvii) Administration of GST will be the responsibility of the GST Council, which will be the apex policy-making body for GST: It will recommend Rates, rate bands, base, thresholds, taxes to be subsumed; Special provisions for Arunachal Pradesh, Assam, J&K, Manipur, Meghalaya, Mizoram, Nagaland, Sikkim, Tripura, Himachal Pradesh and Uttarakhand; Date for application of GST to petroleum products etc.

(xviii) Members of the GST Council are Central and State ministers in charge of the finance portfolio: In the GST Council, the Center will have a one-third vote and all states combined will have two-third vote. Quorum for GST Council is 50% of total members and for majority of Council decisions 75% of the weighted votes of the members present and voting

(xix) GST Council (GSTC): Newly inserted Article 279A in the constitution of India provides for the constitution of GST Council (GSTC) by the president within 60 days from the date of the passing of the Bill and also provides for the appointment of members of the GST Council and its composition and powers to make recommendations

The GSTC has been notified with effect from 12th September, 2016. GSTC is being assisted by a Secretariat. Fourteen meetings of the GSTC have been held so far. The following major decisions have been taken by the GSTC:

- The threshold exemption limit would be Rs. 20 lakh. For special category States enumerated in article 279A of the Constitution, threshold exemption limit has been fixed at Rs. 10 lakh.

- Composition threshold shall be Rs. 50 lakh. Composition scheme shall not be available to inter-State suppliers, service providers (except restaurant service) and specified category of manufacturers.

- Existing tax incentive schemes of Central or State governments may be continued by respective government by way of reimbursement through budgetary route. The schemes, in the present form, would not continue in GST.

- There would be four tax rates namely 5%, 12%, 18% and 28%. Besides, some goods and services would be under the list of exempt items. Rate for precious metals is yet to be fixed. A cess over the peak rate of 28% on certain specified luxury and demerit goods would be imposed for a period of five years to compensate States for any revenue loss on account of implementation of GST. The Council has released rates of various goods and services fitted in these four slabs keeping in view the present incidence of tax in its 14th

- The five laws namely CGST Law, UTGST Law, IGST Law, SGST Law and GST Compensation Law have been recommended.

- In order to ensure single interface, all administrative control over 90% of taxpayers having turnover below Rs. 1.5 crore would vest with State tax administration and over 10% with the Central tax administration. Further all administrative control over taxpayers having turnover above Rs. 1.5 crore shall be divided equally in the ratio of 50% each for the Central and State tax administration.

- Powers under the IGST Act shall also be cross-empowered on the same basis as under CGST and SGST Acts with few exceptions.

- Power to collect GST in territorial waters shall be delegated by Central Government to the States.

- Formula and mechanism for GST Compensation Cess has been finalized.

- Four rules on input tax credit, composition levy, transitional provisions and valuation have been recommended. Further five Rules on registration, invoice, payments, returns and refund, finalized in September, 2016 and as amended in light of the GST bills introduced in the Parliament, have also been recommended.

(xx) Minimum Exemptions: The list of exempted goods and services would be kept to a minimum and it would be harmonized for the Center and the States as far as possible(83 Exemptions recommended for Services and less than 100 expected to be recommended for Goods)

(xxi) Threshold exemption: A common threshold exemption would apply to both CGST and SGST. Taxpayers with a turnover below it would be exempt from GST. A compounding option (i.e.to pay tax at a flat rate without credits) would be available to small taxpayers below a certain threshold. The threshold exemption and compounding provision would be optional. (The threshold exemption limit would be Rs. 20 lakh. For special category States enumerated in article 279A of the Constitution, threshold exemption limit has been fixed at Rs. 10 lakh. Composition threshold shall be Rs. 50 lakh. Composition scheme shall not be available to inter-State suppliers, service providers (except restaurant service) and specified category of manufacturers.)

(xxii) Exports would be zero- rated (Refer Section 16 of IGST Act, 2017)

(xxiii) Input Credit: Credit of CGST paid on inputs may be used only for paying CGST on the output and the credit of SGST paid on inputs may be used only for paying SGST. In other words, the two streams of input tax credit (ITC) cannot be cross utilised, except in specified circumstances of inter-State supplies, for payment of IGST.

The credit would be permitted to be utilised in the following manner:

- a) ITC of CGST allowed for payment of CGST;

- b) ITC of SGST allowed for payment of SGST;

- c) ITC of CGST allowed for payment of CGST & IGST in that order;

- d) ITC of SGST allowed for payment of SGST & IGST in that order;

- e) ITC of IGST allowed for payment of IGST, CGST & SGST in that order.

(xxiv) Accounts would be settled periodically between the Centre and the State: It is to ensure that the SGST used for payment of IGST is transferred by the Center to the Destination State where the goods or services are eventually consumed. Similarly the IGST used for payment of SGST would be transferred by the originating State to the Centre.

(xxv) Harmonized Law: The laws, regulations and procedures for levy and collection of CGST and SGST would be harmonized to the extent possible.

(xxvi) Input Tax Credit (ITC) to be broad based by making it available in respect of taxes paid on any supply of goods or services or both used or intended to be used in the course or furtherance of business.

(xxvii) Electronic filing of returns by different class of persons at different cut-off dates.

(xxviii) Various modes of payment of tax available to the taxpayer including internet banking, debit/ credit card and National Electronic Funds Transfer (NEFT) / Real Time Gross Settlement (RTGS).

(xxix) TDS under GST: Obligation on certain persons including government departments, local authorities and government agencies, who are recipients of supply, to deduct tax at the rate of 1% from the payment made or credited to the supplier where total value of supply, under a contract, exceeds two lakh and fifty thousand rupees (Rs. 2.5 lac).

(xxx) Refund of tax to be sought by taxpayer or by any other person who has borne the incidence of tax within two years from the relevant date.

(xxxi) Obligation on electronic commerce operators (Flipkart/ Amazon etc.) to collect ‘tax at source’, at such rate not exceeding two per cent. (2%) of net value of taxable supplies, out of payments to suppliers supplying goods or services through their portals.

(xxxii) System of self- assessment of the taxes payable by the registered person.

(xxxiii) Audit of registered persons to be conducted in order to verify compliance with the provisions of Act.

(xxxiv) Limitation period for raising demand is three (3) years from the due date of filing of annual return or from the date of erroneous refund for raising demand for short-payment or non-payment of tax or erroneous refund and its adjudication in normal cases.(Bona- fide Cases)

(xxxv) Limitation period for raising demand is five (5) years from the due date of filing of annual return or from the date of erroneous refund for raising demand for short-payment or non-payment of tax or erroneous refund and its adjudication in case of fraud, suppression or willful mis- statement. (Mala- fide Cases)

(xxxvi) Arrears of tax to be recovered using various modes including detaining and sale of goods, movable and immovable property of defaulting taxable person.

(xxxvii) Officers would have restrictive powers of inspection, search, seizure and arrest.

(xxxviii) Goods and Services Tax Appellate Tribunal would be constituted by the Central Government for hearing appeals against the orders passed by the Appellate Authority or the Revisional Authority. States would adopt the provisions relating to Tribunal in respective SGST Act.

(xxxix) Advance Ruling Authority would be constituted by States in order to enable the taxpayer to seek a binding clarity on taxation matters from the department. Center would adopt such authority under CGST Act.

(xI) An anti- profiteering clause has been provided in order to ensure that business passes on the benefit of reduced tax incidence on goods or services or both to the consumers.(Refer Section 171 of CGST Act, 2017)

(xIi) Elaborate transitional provisions have been provided for smooth transition of existing taxpayers to GST regime. (Refer Chapter 20 of CGST Act, 2017)

***************************************

Now let us study section by Section in brief….!

Short title, extent and commencement (Section 1 of CGST Act/ IGST Act 2017)

|

Section 1 of these acts provides that this act will not apply to state of Jammu and Kashmir

|

The State of Jammu and Kashmir enjoys a special status in the Indian Constitution in terms of Article 370 of the Indian Constitution. The Parliament has power to make laws only on Defence, External Affairs and Communication related matters of Jammu and Kashmir. As regards the laws related on any other matter, subsequent ratification by the Government of Jammu and Kashmir is necessary to make it applicable to that State.

Therefore, the State of Jammu & Kashmir will have to pass special laws to be able to implement the Goods and Services Tax Acts as its current Constitutional status does not mandate the applicability of the Goods and Services Tax Acts in the State. Once the laws are passed by the State of Jammu & Kashmir, the Union Government will have to amend these acts to delete the phrase that such provisions do not apply to the State of Jammu & Kashmir. |

| The CGST Act/ IGST Act will to come into operation on the date appointed by the Central Government by means of a notification in the Official Gazette. A provision has been made to notify different dates for commencement of different provisions of the Act. | Tentatively 1st July, 2017 |

About the Author

Saurabh Chhabra, Sr. Executive Finance and Taxation at LexisNexis (A division of RELX India Pvt Limited) brings more than 5 years of practical Tax compliance & consultancy experience to his role as a Tax Specialist.

He is highly dedicated & motivated tax professional, and continuously contributing analytical content to upgrade the professional domain.

He is a Semi qualified, Chartered Accountant and Delhi University graduate. He has recently qualified CA-Final (first group) & also appeared for the Second Group in May 2017 exams.

He has recently secured Six Sigma Yellow Belt certification from LexisNexis Australia, His strength is his interpretation skills of Tax laws and he has successfully designed and implemented various procedures to automate the Tax reports in the ERP’s and ensuring accurate and timely reporting of exceptions. (Specialization in integrating Tax compliance with regular accounting to reduce the compliance cost)

He had gained extensive tax compliance experience through Tax Analyst roles for a variety of companies including PSU’s, banking companies and CA firms located in the Delhi/NCR.

Note- Copyright of the article remains with the Author.

Author Bio