Month: May 2026

2,201 articlesIncome Tax

Income Tax

Important Income Tax Return Due Dates for Financial Year 2025-2026

Corporate Law

Corporate Law

Corporate Law Reforms for Viksit Bharat 2047

DGFT

DGFT

DGFT Permits Self-Declaration for India-UK CETA Certificates of Origin

Company Law

Company Law

Provisional List of 1314 Audit Firms Missing NFRA-2 Filings for 2024-2025

SEBI

SEBI

FAQs on SEBI – IVCA Annual Activity Report (AAR) for AIFs

Corporate Law

Corporate Law

Politics of Expediency and Tamil Nadu Coalition Shift

Corporate Law

Corporate Law

Resolution Plan Approved After Re-Voting as Initial Vote Failed to Meet 66% Threshold: NCLT Mumbai

Company Law

Company Law

NCLT Rejects Confidentiality Breach Plea as Email to Bidder Was Found Inadvertent

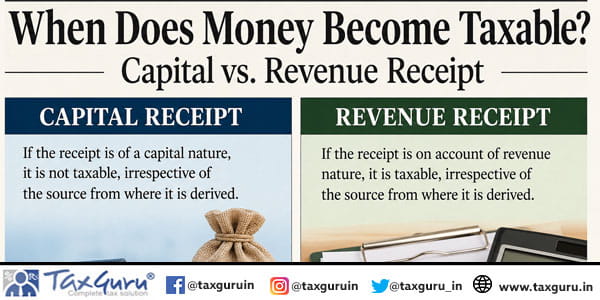

Income Tax

Income Tax

When Does Money Become Taxable? Capital vs. Revenue Receipt

Finance

Finance