Puneet Motwani

As we all know that India has already taken lead position in the area of digital payments because developing, adopting and scaling the UPI technology in a very short span of time has been done only by India and Covid 19 just help by adding fuel to the fire.

Before getting into detail of topic “FUTURE OF VIRTUAL CURRENCY V/S PHYSICAL CURRENCY”, let’s first understand what is virtual currency and physical currency?

Well, who can stop innovation and disruption anyway?

Today every problem opens thousands of ways for a new opportunity, and in the same way globally, when there was a tremendous boom phase of cryptocurrency, the leaders of countries around the world and their central bank consider the same as a serious concern.

As why would any country handover the monetary power of its country to an unknown and anonymous system?

But Indian Government consider the same as an opportunity and launched India’s own digital currency i.e., E- Rupee.

Let’s take an example:

If you have a Rs. 500 note in your wallet, the same is physical currency and if you have Rs. 500 in your Paytm wallet, will the same becomes virtual currency or amount equivalent to Rs. 500 kept as Bitcoin (a crypto currency) whether the same is virtual currency or Digital– Rupee of Rs. 500 which is launched by RBI is virtual currency?

Let’s understand one by one:

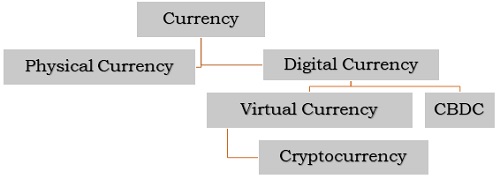

Physical Currency:

Physical Currency refers to the amount of cash–in the form of paper notes or coins–within a country that is physically used to conduct transactions between consumers and businesses.

Digital Currency:

Digital currency is a form of currency that is available only in digital or electronic form. It is also called digital money, electronic money, electronic currency, or cyber cash.

Virtual Currency:

Virtual currency, or virtual money, is a digital currency that is largely unregulated and issued and usually controlled by its developers and used and accepted electronically among the members of a specific virtual community.

A digital representation of value that is neither issued by a central bank or a public authority, nor necessarily attached to a fiat currency, but is accepted by natural or legal persons as a means of payment and can be transferred, stored or traded electronically. They are not legal tender as the same is not issued by Central Bank.

Ex: Crypto currency is a example of digital currency like bitcoin, etherum, etc

Cryptocurrencies:

Cryptocurrency, sometimes called crypto, is any form of currency that exists digitally or virtually and uses cryptography to secure transactions. Cryptocurrencies don’t have a central issuing or regulating authority, instead using a decentralized system to record transactions and issue new units.

Central Bank Digital Currencies:

On 1st November 2022, our Central Bank, RBI gave a big winter gift to India’s Economy and that is Central Bank Digital Currency. As the name itself suggests, it will be a currency in a digital form.

Currency in digital form?

Let’s understand with an example: Whenever you transact in cash like making payment to NBC for coffee, you make payment in exchange for the goods or services. If you look carefully at those currency notes, it is written that “I promise to give an amount of Rs. 100 to the holder”. Apart from this it also includes the signature of the RBI Governor. It means the same is approved by government that’s why it becomes fiat currency. Now in digital currency everything will be same like Govt approval etc. the only difference will be that instead of cash you can pay it digitally.

Digital Rupee is nothing but a virtual currency having the same intrinsic value of a physical rupee which is a fiat currency.

It is not a decentralized cryptocurrency like Bitcoin but shall be an RBI controlled centralized Blockchain. This implies that the Digital Rupee is not the same as a virtual digital asset and shall enjoy a privileged status of being the only recognized and legitimate digital currency in India. The Government and the RBI will never be comfortable with Crypto currency in the country as it has serious potential to undermine the country’s economy and may lead to high levels of tax evasion and money laundering.

Now the Question is whether amount of Rs. 500 in your Paytm wallet is a virtual currency?

Amount of Rs. 500 in Paytm wallet is not a variant of virtual currency or digital currency but the same is categorized as a physical currency because amount of Rs. 500 in Paytm wallet came when you deposit 500 note in your bank means Central Bank has originally issued Rs. 500 note which is a physical currency.

What Central Bank Digital Currency achieves?

- It can get rid of all paper cash and metal coins. That saves trees.

- It eliminates the hassles of going to an ATM to withdraw cash.

- It can be used even by those who do not have a bank account and who just stores cash in their cupboards or under their mattress.

- It is more secure and efficient.

But the point is all this were already being achieved by UPI based payments like Paytm, Gpay etc. then what is the need of digital currency as most people have gone cashless by using UPI. The success of UPI has been stupendous and UPI-based transactions have grown by 1000% in just three years. People use UPI to pay amounts from as low as a few rupees like paying Rs. 10 for Tea to few thousands like making payment for purchase of Car.

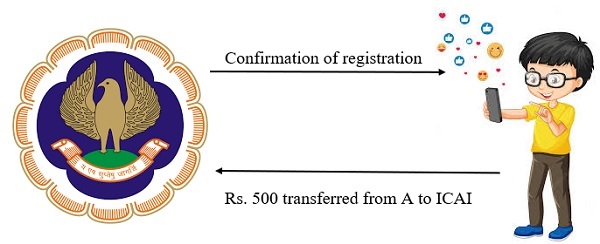

Okay well let’s take an example to understand this:

Many of you had make payment for attending student conference through online mode. Now say Rs. 500 was paid by Student A (having SBI Bank) to ICAI (having BOB Bank) and the transaction was taken place yesterday. So, when A got a message that Rs. 500 was debited from his account whether the same was transferred from SBI Bank to BOB bank.

The answer is No and here comes the Interesting fact that amount of Rs. 500 not actually transferred at the moment the payment was made because in reality there are millions of transactions takes place in a single day through UPI and it is not possible to exchange money for each and every transaction. Therefore, banks exchange money on a specified interval for settling the transactions means there is a time lag between time of settlement and time of transaction.

So now if the same transaction was carried out using RBI Digital currency, then there is no requirement for settling the transactions as the time when amount of Rs. 500 is debited the same will be transferred from A RBI Bank account to ICAI RBI Bank Account.

That’s why the Reserve Bank’s upcoming digital currency is so important and so different.

Other differences of UPI and CBDC:

- UPI is just a payment mechanism whereas e-rupee is actually cashless digital currency.

- The UPI still requires you to have a bank account for know your customer (KYC) compliant and so on.

- The e-rupee is stored directly in an account with the RBI. It is based on blockchain technology, the same used by Bitcoin which uses decentralized ledgers.

Benefits of Virtual Currency over Physical Currency:

1. Central banks believe that cost of issuing digital currency is much lower than the cost of printing and distributing physical cash.

2. The Central banks can track the transactions of digital currency as it is based on block chain technology, unlike the physical currency which may be a hurdle to adopt for people as it may affect their privacy concerns. According to a recent report, 81 countries, representing over 90% of global GDP, are exploring launching their own central bank digital currencies.

3. The International Monetary Fund (IMF), the World Bank, and the Bank of International Settlements (BIS) say CBDCs “have the potential to enhance the efficiency of cross-border payments, as long as countries work together.”

4. Promoting financial inclusion by providing easy and safer access to money for unbanked and underbanked populations;

5. Introducing competition and resilience in the domestic payments market, which might need incentives to provide cheaper and better access to money.

6. Increasing efficiency in payments and lowering transaction costs;

Whether Virtual Currency will be able to replace Physical Currency?

As even after 6 years of Demonetization, no doubt UPI and Digital payments had gained the pace but dependency on cash has not yet reduced till now. The currency with the public, which was at Rs 17, trillion just before the demonetization exercise, was at a record-high Rs 30.8 trillion as on October 21, 2022.

So, it will be wrong to say that virtual currency will replace physical currency any time sooner however as like RBI had already backed Rs. 2000 currency notes and in current market, we hardly see any 2000 currency note. Just like that it might be possible that RBI will back remaining currency and replace the same with digital currency and make the complete system online.

Future of Crypto currencies:

Cryptocurrencies like bitcoin have exploded in value, but they are largely used for speculation or to buy other speculative assets. Although there have been some signs of merchant adoption in countries like El Salvador, the high volatility and complexity of these currencies make them impractical for most daily applications.

Another possible application is in central bank digital currencies, which could be issued by a country’s bank or monetary authority. These would be used and stored in online wallets, similar to cryptocurrencies, but allowing the central bank to issue and freeze tokens at will.

Future of Digital Currency:

Digital Currency Is Not Private Crypto:

CBDC will be different from cryptocurrencies because compared to CBDC, they are not authorized means of payment and do not have a legal backing.

Clarity on ownership:

In case of digital currency as the same is backed by Central Bank so even if something go wrong — say, in the IT system, or some other unforeseen contingency — the holder of that bank’s currency, whether in physical or digital form, has confidence that the value of that currency will be available to him at all times.

Retail Payments in India:

In recent years, India’s retail payments system has grown more sophisticated, more dynamic, and much larger. The broad payment space includes several payment system operators, wallet companies, and the providers to operators and card companies. These companies have grown more profitable as customers enjoy more choice.

Conclusion:

> As we have seen different versions of money from Barter system to physical cash to digital cash and each time money has change a lot.

> Managing physical cash becomes a challenging task for us as well as for government as we all know that during the course of demonetization, various black money fraud instances were caught. As we all are aware that UPI has made our life much easier.

> RBI clearly said that right now digital rupee will not replace current monetary system but compliment current monetary system and Just to test waters, 1 CBDT pilot launched for wholesale banking segment and probably the same will be launched for the Retail sector by next month.

> If India’s goal is to become a superpower with a large GDP, the faster the movement of money the better, and if speed is the goal, digitization is the route. Newer digital forms that are safe, secure, convenient, and easy to use will power India into the future. The coming digital currency from India’s central bank will be a major step in that direction.