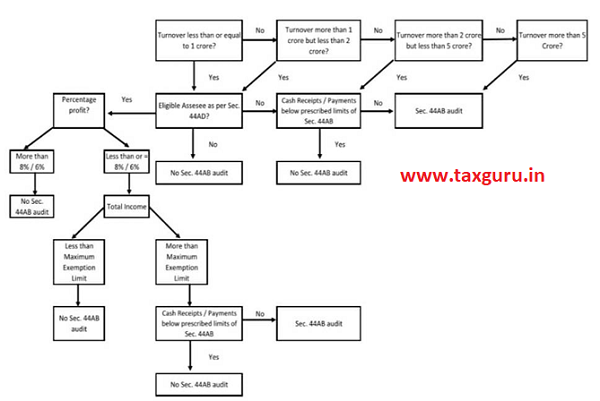

Article explains provision of Section 44AB and Section 44AD of Income Tax Act, 1961 with reference to Income Tax Audit.

While presenting the Union Budget for 2020-21, the Finance Minister announced that currently, businesses having turnover of more than one crore rupees are required to get their books of accounts audited by an accountant. In order to reduce the compliance burden on small retailers, traders, shopkeepers who comprise the MSME sector, she proposed to raise by five times the turnover threshold for audit from the existing Rs. 1 crore to Rs. 5 crore.

Further, in order to boost less cash economy, she proposed that the increased limit for mandatory tax audit shall apply only to those businesses which carry out less than 5% of their business transactions in cash.

New Provisions applicable under section 44AB & 44AD are summarized as below:-

Let’s discuss in detail:-

SECTION 44AB

a) BUSINESS

Every person carrying on business shall, if his total sales, turnover or gross receipts, in business exceed or exceeds “one crore rupees” in any previous year

Provided that in the case of a person whose—

(a) aggregate of all amounts received including amount received for sales, turnover or gross receipts during the previous year, in cash, does not exceed five per cent of the said amount; and

(b) aggregate of all payments made including amount incurred for expenditure, in cash, during the previous year does not exceed five per cent of the said payment,

this clause shall have effect as if for the words “one crore rupees”, the words “five crore rupees” had been substituted; or

b) PROFESSION

Every person carrying on profession shall, if his gross receipts in profession exceed “fifty lakh rupees” in any previous year; or

c) PRESUMPTIVE BUSINESS u/s. 44AE/44BB/44BBB

Every person carrying on the business shall, if the profits and gains from the business are deemed to be the profits and gains of such person under section 44AE or section 44BB or section 44BBB, as the case may be, and he has claimed his income to be lower than the profits or gains so deemed to be the profits and gains of his business, as the case may be, in any previous year; or

d) PRESUMPTIVE PROFESSION u/s. 44ADA

Every person carrying on the profession shall, if the profits and gains from the profession are deemed to be the profits and gains of such person under section 44ADA and he has claimed such income to be lower than the profits and gains so deemed to be the profits and gains of his profession and his income exceeds the maximum amount which is not chargeable to income-tax in any previous year; or

e) PRESUMPTIVE BUSINESS u/s. 44AD

Every person carrying on the business shall, if the provisions of sub-section (4) of section 44AD are applicable in his case and his income exceeds the maximum amount which is not chargeable to income-tax in any previous year,

Get his accounts of such previous year audited by an accountant before the specified date and furnish by that date the report of such audit in the prescribed form duly signed and verified by such accountant and setting forth such particulars as may be prescribed.

Provided that this section shall not apply to the person, who declares profits and gains for the previous year in accordance with the provisions of sub-section (1) of section 44AD and his total sales, turnover or gross receipts, as the case may be, in business does not exceed “two crore” rupees in such previous year

Provided further that this section shall not apply to the person, who derives income of the nature referred to in section 44B or section 44BBA, on and from the 1st day of April, 1985 or, as the case may be, the date on which the relevant section came into force, whichever is later :

Provided also that in a case where such person is required by or under any other law to get his accounts audited, it shall be sufficient compliance with the provisions of this section if such person gets the accounts of such business or profession audited under such law before the specified date and furnishes by that date the report of the audit as required under such other law and a further report by an accountant in the form prescribed under this section.

SECTION 44AD

1) PROFIT @ 8%

Notwithstanding anything to the contrary contained in sections 28 to 43C, in the case of an eligible assessee engaged in an eligible business, a sum equal to eight per cent of the total turnover or gross receipts of the assessee in the previous year on account of such business or, as the case may be, a sum higher than the aforesaid sum claimed to have been earned by the eligible assessee, shall be deemed to be the profits and gains of such business chargeable to tax under the head “Profits and gains of business or profession” :

PROFIT @ 6%

Provided that this sub-section shall have effect as if for the words “eight per cent”, the words “six per cent” had been substituted, in respect of the amount of total turnover or gross receipts which is received by an account payee cheque or an account payee bank draft or use of electronic clearing system through a bank account [or through such other electronic mode as may be prescribed] during the previous year or before the due date specified in sub-section (1) of section 139 in respect of that previous year.

2) DEDUCTIONS U/S. 30 TO 38

Any deduction allowable under the provisions of sections 30 to 38 shall, for the purposes of sub-section (1), be deemed to have been already given full effect to and no further deduction under those sections shall be allowed.

3) DEPRECIATION

The written down value of any asset of an eligible business shall be deemed to have been calculated as if the eligible assessee had claimed and had been actually allowed the deduction in respect of the depreciation for each of the relevant assessment years.

4) LOCK-IN PERIOD

Where an eligible assessee declares profit for any previous year in accordance with the provisions of this section and he declares profit for any of the five assessment years relevant to the previous year succeeding such previous year not in accordance with the provisions of sub-section (1), he shall not be eligible to claim the benefit of the provisions of this section for five assessment years subsequent to the assessment year relevant to the previous year in which the profit has not been declared in accordance with the provisions of sub-section (1).

5) MANDATORY AUDIT

Notwithstanding anything contained in the foregoing provisions of this section, an eligible assessee to whom the provisions of sub-section (4) are applicable and whose total income exceeds the maximum amount which is not chargeable to income-tax, shall be required to keep and maintain such books of account and other documents as required under sub-section (2) of section 44AA and get them audited and furnish a report of such audit as required under section 44AB.

6) SECTION 44AD NOT APPLICABLE

The provisions of this section, notwithstanding anything contained in the foregoing provisions, shall not apply to—

(i) a person carrying on profession as referred to in sub-section (1) of section 44AA;

(ii) a person earning income in the nature of commission or brokerage; or

(iii) a person carrying on any agency business

7) ELIGIBLE ASSESSEE

(i) an individual, Hindu undivided family or a partnership firm, who is a resident, but not a limited liability partnership firm as defined under clause (n) of sub-section (1) of section 2 of the Limited Liability Partnership Act, 2008 (6 of 2009); and

(ii) who has not claimed deduction under any of the sections 10A, 10AA, 10B, 10BA or deduction under any provisions of Chapter VIA under the heading “C. – Deductions in respect of certain in-comes” in the relevant assessment year;

8) ELIGIBLE BUSINESS

(i) any business except the business of plying, hiring or leasing goods carriages referred to in section 44AE; and

(ii) whose total turnover or gross receipts in the previous year does not exceed an amount of two crore rupees.

SECTION 44ADA

(1) PROFIT @50%

Notwithstanding anything contained in sections 28 to 43C, in the case of an assessee, being a resident in India, who is engaged in a profession referred to in sub-section (1) of section 44AA and whose total gross receipts do not exceed fifty lakh rupees in a previous year, a sum equal to fifty per cent of the total gross receipts of the assessee in the previous year on account of such profession or, as the case may be, a sum higher than the aforesaid sum claimed to have been earned by the assessee, shall be deemed to be the profits and gains of such profession chargeable to tax under the head “Profits and gains of business or profession“.

(2) DEDUCTIONS U/S. 30 TO 38

Any deduction allowable under the provisions of sections 30 to 38 shall, for the purposes of sub-section (1), be deemed to have been already given full effect to and no further deduction under those sections shall be allowed.

(3) DEPRECIATION

The written down value of any asset used for the purposes of profession shall be deemed to have been calculated as if the assessee had claimed and had been actually allowed the deduction in respect of the depreciation for each of the relevant assessment years.

(4) MANDATORY AUDIT

Notwithstanding anything contained in the foregoing provisions of this section, an assessee who claims that his profits and gains from the profession are lower than the profits and gains specified in sub-section (1) and whose total income exceeds the maximum amount which is not chargeable to income-tax, shall be required to keep and maintain such books of account and other documents as required under sub-section (1) of section 44AA and get them audited and furnish a report of such audit as required under section 44AB.

Disclaimer: The contents of this article are for information purposes only and does not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

Article Contributed by: Sagar Gambhir | FCA, DISA (ICAI) | casagargambhir@gmail.com

Author can be reached at casagargambhir@gmail.com for any queries, issues & recommendations relating to article.

Author Bio

If firm’s TO is 3 cr with less than 5% cash receipts and payment,having profit almost NIL or loss.Will tax Audit be applicable,never used 44AD so far every year Tax Audit got done .plz reply if convenient.

Not liable

An eligible partnership firm has Turnover which is less than 1 crore during A.Y. 2020-21. It maintains proper books of accounts as specified by the Act. And its profit is 3%. Is the firm eligible for audit u/s 44AB.

An eligible partnership firm has Turnover which is less than 1 crore during A.Y. 2020-21. It maintains proper books of accounts as specified by the Act. And its net profit is 3 %. IS the firm eligible for audit u/s 44AB

Respected sir

Please guide, if T.O is less then 5cr cash transaction is less then 5% or NIL, but profit is below 6% / 8%, then audit applicable???, and if NO then why same is not applicable for T.O less then 2cr who come out from 44AD and get there books audited u/ 44AB for profits less then 6% / 8%

Thanks giving

Sir

Please keep in mind that the firm starts the business at the beginning of fy 2019-20.

Sir

Could you please explain the following issue.

An eligible partnership firm has Turnover which is less than 1 crore during A.Y. 2020-21. It maintains proper books of accounts as specified by the Act. But it

incurrs loss in the initial year. Whether it is mandatory to get audited by a CA due to the deemed concept u/s 44 AD.

I am studant

THANKS