The Finance Act, 2020 tightened the existing provisions for those who have not been filing income tax returns. This will be applicable from July 1, 2020. Section 194N for deduction of tax at source (TDS) on cash withdrawals exceeding Rs.1 crore was introduced by the Finance Minister in the Union Budget 2019.

This section applies to an aggregate of sums withdrawn from a particular payer in a financial year. The Government has introduced Section 194N in the Union Budget 2019 with the objective to discourage cash transactions in the country and promote the digital economy.

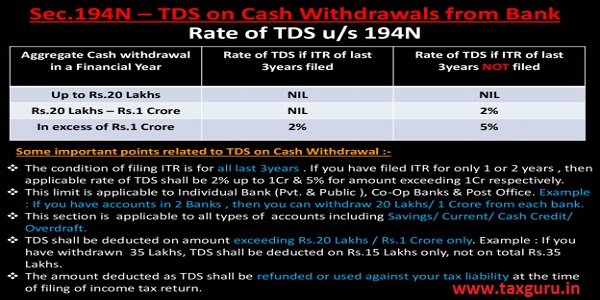

Section 194 N of the Income Tax Act has been amended vide clause 84 of the Finance Act 2020. The Scope of TDS on cash withdrawal has been extended under the amended Section 194 N. TDS at the rate of 2% is required to be deduced if the withdrawer has not filed his tax return for three years and withdrawal during the year exceeds Rs 20 lakhs but less than Rs 1 crore. For withdrawal more than Rs 1 crore TDS at the rate of 5% is required to be deducted.

The Amendment of Section 194N will be with effect from July 1, 2020. The section will apply to withdrawals made by taxpayers who are an individual, A Hindu Undivided Family (HUF), a Company, a partnership firm, or an LLP, a local authority, an Association of Person (AOPs) or Body of Individuals (BOIs). However, this section will not be applicable to government bodies, banks including co-operative banks, business correspondents of a banking company, white-label ATM operator of any bank, farmers whom the Central Government specifies the commission agent or trader. CBDT exempts cash withdrawal by the authorized dealer and its franchise agent and sub-agent, and Full-Fledged Money Changer (FFMC) licensed by the Reserve Bank of India and its franchise agent from TDS under Section 194N The person (payer) making the cash payment will have to deduct TDS under Section 194N, which includes any bank (both public or private), a co-operative bank, and post office.

TDS under Section 194N tax shall be required to be deducted only when the aggregate amount of cash withdrawal during the previous year by a person from one or more of his bank or post office account, as the case may be, exceeds Rs.20 Lakhs and the said person has not filed his Income Tax Returns for the last three years.

Further, the tax shall be required to be deducted only on the amount exceeding Rs.20 Lakhs.

For example, if Mr. ‘Y’ has filed all his returns and if he withdraws cash up to Rs.1 Crore then no TDS will be applicable. In case Mr. ‘Y’ withdraws cash which is more than Rs. 1 Crore then only 2% TDS will be applicable. On the other hand if Mr. ‘Z’ has not filed all his returns and if he withdraws cash from Rs. 20 Lakh to Rs. 1 Crore then 2% of the TDS will be applicable. In case Mr. ‘Z’ withdraws cash which is more than Rs. 1 Crore then 5% TDS will be applicable.

TDS will be deducted by the payer while making the cash payment over and above Rs 1 crore in a financial year to the payee. If the payee withdraws a sum of money on regular intervals, the payer will have to deduct TDS from the amount, once the total sum withdrawn exceeds Rs 1 crore in a financial year. The TDS will be done on the amount exceeding Rs 1 crore.

In the example, Mr. ‘Y’ withdraws 45 Lakhs in the aggregate in the financial year and in the next withdrawal, an amount of Rs 1.25 crores is withdrawn, the TDS liability is only on the excess amount of Rs.70 Lakhs.

Author Bio

The company was started in F.Y.2017-18. and till now we have filed two returns F.Y.17-18 & F.Y.18-19, whereas we have time to efile the F.Y.19-20 return upto nov 2020. as efiling time has not expired how the bank can deduct 2% TDS now…