Equity investors had a long tax holiday as the capital gains were not taxed and were exempt under section 10(38) until assessment year 2018-19.

But Capital Gains on sale of equity shares in a listed company or unit of an equity oriented mutual fund (hereafter both are referred to as shares in this article) held for more than a year becomes taxable from Assessment Year 2019-20. The charging section is 112 A read along with section 55(ii)(ac).

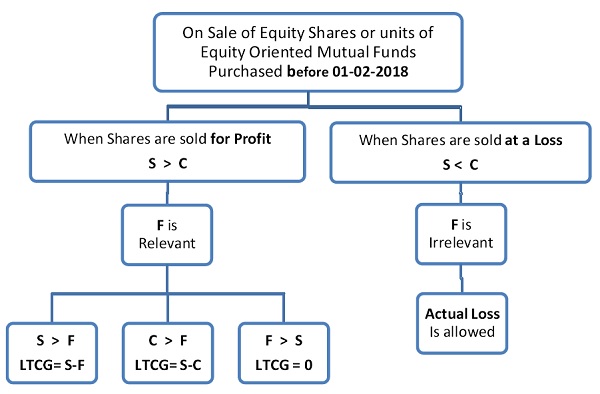

While section 112 A states that the rate of tax is 10 % above a threshold of Rs.1,00,000/ -, section 55(ii)(ac) provides us with the method of arriving at the cost of acquisition of such shares for computing the capital gains.

If the shares were bought by the investor on or after 01-02-2018, then Capital Gains is the difference between the selling price and the actual cost of acquisition, as no indexation benefit is provided under section 112A.

But if the shares were bought prior to that date, then cost of acquisition for computing capital gains has to be arrived by the method provided in section 55(ii) (ac).

According to this section, the cost of acquisition is arrived by a 2 step process.

1st Step- Compare the sale price of the share (S), with the fair market value (F) of the share on 31-01-2018, which is the highest traded price of the share in any of the recognized stock exchanges i.e. BSE or NSE and find out whichever is lower. Let this be denoted as “ X ”.

2nd Step- Compare the result of the 1st Step“ X “ with the actual cost of acquisition (C) and find out whichever is higher. Let this be denoted as “ Z ”.

The result of 2nd Step is the cost of acquisition as per section 55(ii)(ac) that is to be used for calculating the long term capital gains (LTCG) under section 112A.

This article attempts to explain the complex methodology provided in section 55(ii) (ac) in a simple tabular form, so that an investor is able to understand the tax implications before effecting such sale.

To summarize the above different possible scenarios-

Even though the capital gain of the long term equity investor is taxed now, the government had enacted the tax provisions that are more than fair to the tax payer. This is evident from the fact that while the government is not taxing the gains in scenario 3 even though the investor has actually made a profit; but is allowing the entire loss incurred by the investor in scenarios 4, 5 & 6.

Sir

Kindly clarify below query.

I purchased many scrips through Karvy which is closed now. As I do not have the purhase values for many scrips, I understand FMV as on 31Jan2018 has to be applied.

But, my actual purchase price is much higher than the FMV as on 31Jan2018. How to calculate LTCG in this case.

Also note that I had gifted the stocks around 10 years ago to my wife and do not have that transfer date too.

Actual purchase in my name – than transferred to my wife account – sold from my wife account.

Kindly help

Regards

Fantastic, your article is among the only one available online, that shows that only if the expert understands the matter well, can he/she elaborate on it so well.

Excellent analysis and explanation of LTCG scenarios. Yours is the only article I have come across so far that explains all the six possible scenarios. Elsewhere, only four scenarios are discussed. Good show.

Pl elabrote on cost of acquisition. In case the such equity was bought long back say 5 years back is the cost of acquisition is calculated with indexation. Pl advise.

Latest Capital Gains Tax structure simplified for easy understanding.Let your service continue.

shall be thankful to please guide for taking the expense charges as ‘DEMAT HOLDING ‘ (BEING TAKEN AS GENERALLY 25/= PER SALE TRANSACTION) DEBITED ON SALE POINT FOR CALCULATING LTCG. THANKS.

LTCG/Loss calculation:(listed shares)

Your essay is informative but could be shorter. As it contains a lot of avoidable stuff.

However, more importantly, you have NOT stated how exactly the total cost of acquisition of share or its sale, are to be calculated because the bill received from the broker, while selling/buying shares, includes a number of taxes, charges & levies whereas only few of these are allowed for each calculation.

Cost of acquisition = Total sale price-STT.

Sale price= Total sale price-STT-brokerage.

Plz include these calculations too, in your essay.

Thx..//

Very well explained

Thank you