Forms 1042, 1042-S, and 1042-T are U.S I.R.S taxation forms dealing with dealings with foreign persons, including non-resident aliens, foreign entities, etc.

Forms 1042 and 1042-S need to be filed separately. The main difference between these forms is that form 1042-S is concerned with payments made to foreign nationals, while form 1042 is concerned with determining how much income will be withheld for tax withholding purposes. Also, Form 1042-S must always be filed together with Form 1042-T.

Eligibility Of Form 1042, 1042S:

Every withholding entity, agent, or intermediary, whether registered in the U.S.A. or not, who is entitled to any fixed or determinable U.S. source income from any foreign persons, must file these forms with the IRS. For example, employers that employ non-resident individuals need to file a 1042-S Form with the IRS and send a (completed) copy of that form to the non-resident individuals.

A separate Form 1042-S is required for:

(i) Each recipient of income whether you withheld tax or not.

(ii) Each tax rate of a specific type of income that you paid to the same recipient.

(iii) Each type of income that you paid to the same recipient.

Due Date for Filing These Forms:

Recipient Copy up to March 15, 2022

IRS Paper Filing up to March 15, 2022

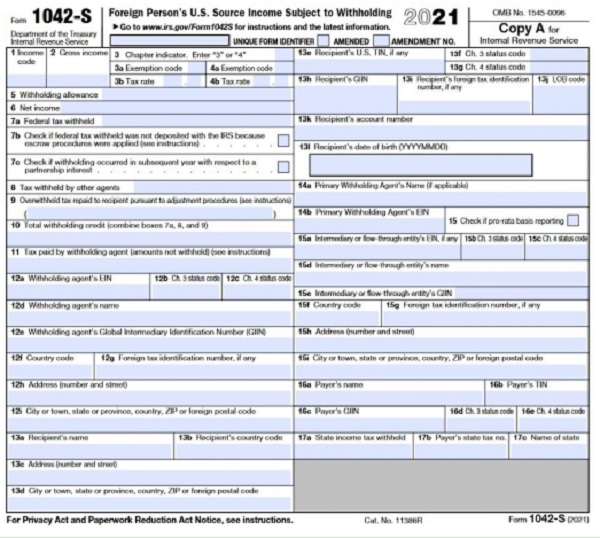

Format Of Form 1042S

Author Bio