Case Law Details

Shri Jai Singh Yadav Vs ACIT (ITAT Jaipur)

No addition can be made only on the basis of statements of the third party without providing the opportunity of cross-examination of the person when specifically asked by the assessee in whose hand the addition has been made

Facts-

The assessee filed his original ROI u/s 139(1)declaring a total income of Rs.3,08,160/. A search and seizure operation u/s 132 was carried out by Income Tax Department on 19/11/2016 at the premises. By virtue of search, a warrant was issued in the joint name of assessee Jai Singh Yadav and his brother Gopal Lal Yadav. In the course of the search, various documents were found and seized by the department.

On the same date, a search Search was also carried out by the department at the residence/ premises of Sh. Harpal Yadav and M/s Kedia Real Estate LLP or Sh. Nirmal Kumar Kedia. Consequent to the search proceedings, AO issued the notice u/s 153A, and in response thereto, the assessee filed his return of income declaring the total income at Rs.3,08,160/-, same as declared u/s 139(1).

AO stated that during the course of search the statements of Sh. Harpal Singh was confronted to the assessee and assessee Sh. Jai Singh Yadav has given his consent to the statement of Sh. Harpal Singh Yadav and admitted that he had purchased the shop at Kardhani in his sons name from sons of Sh. Kailash Bhutia at actual sale consideration of Rs.1,50,00,000/- and paid Rs.1,17,20,000/- as “On Money” in cash for purchase of this shop from his undisclosed income and offered for taxation in this year. Therefore, the AO issued a show cause notice dt. 19.04.2018 for purposing the addition of Rs.1,17,20,000/-.

AO held that the amount in the nature of ‘on money’ consideration and he made the addition of Rs. 1,17,20,000/- u/s 68 and invoked provisions of section 115BBE. CIT(A) also confirmed the addition.

Conclusion-

Held that When the assessee sought cross examination of Sh. Harpal Yadav the AO has straight away denied the same. When it is now a settled principle of law that no addition can be made only on the basis of statements of the third party without providing the opportunity of cross-examination of the person when specifically asked by the assessee in whose hand the addition has been made.

The Hon’ble Supreme Court in case of Andaman Timber Industries Vs. CCE 127 DTR 0241 dated 02.09.2015 wherein it has been held that denial of opportunity to the assessee to cross-examine the witnesses whose statements were made the sole basis of the assessment is a serious flaw rendering the order a nullity in as much as it amount to violation of principles of natural justice.

FULL TEXT OF THE ORDER OF ITAT JAIPUR

These are total three appeals and two of which are cross appeals filed against the order of the ld. CIT(A)-4, Jaipur dated 09-02-2022 for the assessment year 2016-17 and the Department has also filed another appeal in the case of Shri Gopal Lal Yadav against the order of the ld. CIT(A)-4, Jaipur dated 09-02-2022 for the assessment year 2016-17 wherein respective parties have raised following grounds of appeal.

ITA No. 125/JP/2022 – Jai Singh Yadav (Assesse)

‘’1. The impugned assessment order u/s 143(3) r.w.s. 153A dated 12-12-2018 as well as notices are bad in law and on facts of the case, for want of jurisdiction and various other reasons and hence, the same may kindly be quashed.

2. The search action taken u/s 132 is illegal, bad in law and on the facts of the case for want of jurisdiction and various other reasons against the provisions and procedure as per law and further contrary to the real facts of the case, hence all the consequent notices as well as subsequent proceedings invalid, illegal and bad in law hence liable to be quashed.

3. 1,17,20,000/-: The ld. CIT(A) has grossly erred in law as well as on the facts of the case in confirming the addition of Rs.1,17,20,000/- made by the AO u/s 68 on account of alleged On Money paid by the assessee on purchasing of property in the name of son and nephew and also erred in not considering the material and evidences available on record in their true perspective and sense and presumptions. Hence, the addition so made by the AO and sustained by the ld. CIT(A) is being totally contrary to the provisions of law and facts on the record and hence the same may kindly be deleted in full.

3.2. The ld. CIT(A) has also grossly erred in law as well as on the facts of the case in confirming the addition despite the fact as the AO had denied the cross examination of the persons and ignoring the retraction made by the assessee and proceeded on the third party statements. Hence, also the addition so made by the AO and sustained by the ld. CIT(A) is being totally contrary to the provisions of law and facts on the record and hence the same may kindly be deleted in full.

4. The AO has grossly erred in law as well as on the facts of the case in invoking the provisions of Section 115BBE for charging tax on higher without any show cause notice and not applicable. Hence, the provision so invoked and tax so charged at higher rate is also being totally contrary to the provisions of law and facts on the record and hence the same may kindly be deleted in full.

5. The AO has grossly erred in law as well as on the facts of the case in charging interest u/s 234B. The appellant totally denies its liability of charging of any such interest. The interest so charged being contrary to the provisions of law and facts may kindly be deleted in full.

ITA No. 168/JP/2022 – Jai Singh Yadav (Department)

1. The ld. CIT(A) has erred in law and on facts in deleting the addition of Rs,2,44,93,451/- on account of long term capital gains, resulting out of hitherto unreported cash receipts of Rupees Five Crore. In granting relief, the CIT(A) has ignored the vital facts/ evidence that the payer of money Shri Nirmal Kumar Kedia admitted in his statemnert u/s 132(4) as having paid this amount.

2. The ld CIT(A) has erred in law and in fact in granting relief to the taxpayer, ignoring the statement made by the buyer of the land. In doing, the ld. CIT(A) has failed to consider the law of human probabilities as laid down by Hon’ble Supreme Court in the cases of Sumati Dayal reported as 214 ITR 801SC and Durga Prasad More 82 ITR 540 (SC).

ITA No. 167/JP/2022 – Gopal Lal Yadav (Department)

1. The ld. CIT(A) has erred in law and on facts in deleting the addition of Rs,2,44,93,451/- on account of long term capital gains, resulting out of hitherto unreported cash receipts of Rupees Five Crore. In granting relief, the CIT(A) has ignored the vital facts/ evidence that the payer of money Shri Nirmal Kumar Kedia admitted in his statement u/s 132(4) as having paid this amount.

2. The ld CIT(A) has erred in law and in fact in granting relief to the taxpayer, ignoring the statement made by the buyer of the land. In doing, the ld. CIT(A) has failed to consider the law of human probabilities as laid down by Hon’ble Supreme Court in the cases of Sumati Dayal reported as 214 ITR 801SC and Durga Prasad More 82 ITR 540 (SC).

2.1 First of all, we take up the appeal of the assessee for adjudication of case wherein the ground of appeal Nos. 1,3 &,4 are related to one another and is being taken up together for adjudication

2.2 Briefly stated the facts of the case are that the assessee filed his original return of income u/s 139(1)declaring the total income of Rs.3,08,160/-. The assessee is engaged in the business of digging, tilling and levelling of agriculture farm and commission on sale of agriculture produce of other farmers and also other sources income. In the case of assessee i.e. Jai Singh group a Search and seizure operation u/s 132 was carried out by Income Tax Department on 19/11/2016 at the premises of assessee. By virtue of search, a warrant was issued in joint name of assessee Jai Singh Yadav and his brother Gopal Lal Yadav. In the course of search various documents were found and seized by the department. On the same date a Search was also carried out by the department at the residence/ premises of Sh. Harpal Yadav and M/s Kedia Real Estate LLP or Sh. Nirmal Kumar Kedia on the very same day. Consequent upon the search proceedings, the AO issued the notice u/s 153A on 17.02.2017 and in response thereto, the assessee filed his return of income on 30.06.2017 declaring the total income at Rs.3,08,160/-, same as declared u/s 139(1) . The AO in his assessment order stated that some documents were found and seized at page No.7 of Exhibit No.2 of Annexure-AS at the premises of Sh. Harpal Yadav relating to details of transaction in the name of ‘Kailash Bhutia- Jobner Walon Ka Hisab’ wherein the details of cash payment of Rs.1,27,50,000/- and cheque payment of Rs. 30,50,000/- is mentioned vide page 2 of the assessment order., Sh. Harpal Yadav statement was recorded u/s 132(4) at his premises wherein he has stated about the sale of shop at Kardhani by Kailash Bhutia to Gopal Yadav & Jai Singh Yadav for Rs. 1.50 crore. He also stated that the said transactions took place approx 2-3 years back and that he had no role in this transaction. He also stated that registry of this transaction was done approx 2 years back vide Que Ans. 11 at page 2 of assessment order. The AO also noted that during the course of search sale deed dt.06.08.2015 was found from the residential premises of the assessee which was marked as Page No. 88-89 of Exhibit-2 of annexure-AS. This sale deed was executed between Sh. Satya Prakash Buhtia & Jitendra Bhutiya sons of Sh. Kailash Chand Bhutiya (as seller) and Sh. Manoj Yadav, Sh. Shankar Lal Yadav, Sh. Raj Kumar Yadav & Sh. Kailash Yadav sons of Sh. Jai Singh Yadav(as purchasers) for sale of Shop No.16 at Kardhani, Govindpura, B-Block Kalwar Road Jaipur for consideration of Rs.32,80,000/-. Further, the AO stated that during the course of search the statements of Sh. Harpal Singh was confronted to the assessee and assessee Sh. Jai Singh Yadav has given his consent to the statement of Sh. Harpal Singh Yadav and admitted that he had purchased the shop at Kardhani in his sons name from sons of Sh. Kailash Bhutia at actual sale consideration of Rs.1,50,00,000/- and paid Rs.1,17,20,000/- as “On Money” in cash for purchase of this shop from his undisclosed income and offered for taxation in this year. Therefore, the AO issued a show cause notice dt. 19.04.2018 for purposing the addition of Rs.1,17,20,000/-.

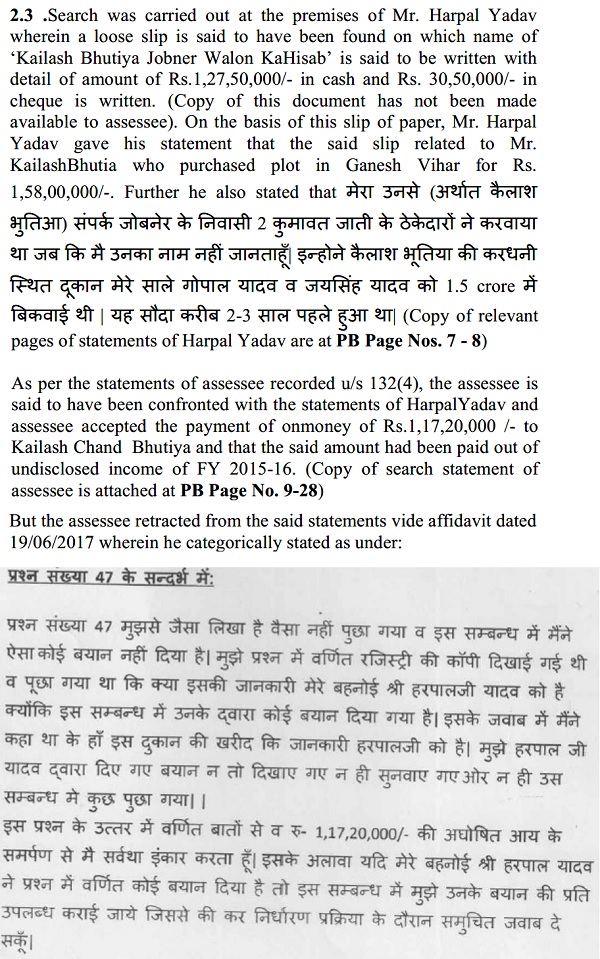

2.3 The assessee replied this show cause notice vide page -2 of the assessment order as well as letter placed at PB 73, wherein he had stated that the assessee had retracted from the statement through the affidavit placed at PB 1-6 and also asked the AO to provide cross examination of Sh. Harpal Yadave and also to provide the seized documents found at Sh. Harpal Yadav Premises. However, the AO has not accepted the request of the assessee and stated that request of assessee for cross examination is not acceptable as the right of cross examination is not an absolute right. The AO has also stated that the affidavit in respect of retraction against statement u/s 132(4) is not found acceptable because the statement of assessee were recorded in the presence of two witnesses. The AO had drawn inference that the practice of “on money” payment in cash is widely prevalent in the real estate market. The AO also observed that the claim of misrepresentation was not made by the assessee as well as his group till seven months after the search. The AO held that the claim made by assessee in the affidavit is merely unsubstantiated allegation which can only be considered as an afterthought since the same is neither supported by any evidence nor reported to the department anytime during the search and even after the passage of considerable time of 7 months and same is hereby rejected. Thus the AO held that this amount in the nature of ‘on money” consideration and he made the addition of Rs.1,17,20,000/- u/s 68 and also invoked the provision of Sec. 115BBE of the Act.

2.4 In first appeal, the assessee filed the detailed WS (PB49-56) alongwith various case laws which is also mentioned at pages No. 3-11 of the ld. CIT(A)’s. The ld. CIT(A) after considering the same confirmed the additions and action of the AO by observing that in this case incriminating documents substantiating the unaccounted transactions were found and seized which were further corroborated by the sale deed as well as the aforesaid statement of assessee and Sh. Harpal Yadav. The ld. CIT(A) has also referred some judgments in his order vide page 15 to 18. Thus the ld. CIT(A) by relying upon on the statements of Shri Harpal Yadav and assessee recorded during the course of Search, had confirmed the addition .

2.5 The assessee has filed an appeal against the order of the ld.CIT(A) before us.

However, during the course of hearing, following written submission were placed by the AR of the assessee.

“1. No addition can be made without cross examination: 1.1 Firstly we would like to submit that the ld. AO has made the addition only on the basis of statements of Sh. Harpal Yadav third party and the documents found in his premises i.eat third party. As the statement of Harpal Singh Yadav has not been seen to the assessee. The assessee had requested for the statement on dt.11.01.2017 to the ADIT again on 21.03.2017 and the same was received on 11.05.2017 and after examining all the thing and statement assessee has retracted from the same through his affidavit cum retraction on dated 19/06/2017(PB1-6). The ld. AO has also recorded the statements of the assessee on dt. 03.05.2018(PB43-47) at both the time the assessee has clearly stated that he had not been asked question no. 47 as stated in his Statements recorded during search proceedings. He had been shown registry of shop and was asked that whether it was in the knowledge of Sh. HarpalYadav, to which he replied in affirmation. He had not stated anything regarding surrender of Rs. 1,17,20,000/-.

In fact the property purchased i.e. Shop No. 16 had been purchased jointly by sons and nephews of assessee. The said transaction does not relate to the assessee. Shop was purchased in year Aug.,2015 while as per alleged statement of Sh. Harpal Singh the transaction is said to have been done 2-3 years back which itself is contradictory. No addition can be made merely on the basis of statements of third person without documents substantiating the said transaction/income. The assessee had, in his retraction statement, requested for providing the copy of statements of Sh. HarpalYadav but it has not been provided to him. Further assessee also seeks copy of relied upon documents in respect of said transaction so that further explanation with reason may be given. Assessee also asked to the ld. AO to give an opportunity to cross examine Mr. HarpalBYadav and any other person who claims to have paid amount exceeding the transaction amount as per purchase deed but the same has been rejected admittedly. Assessee has not surrendered any undisclosed income on this account.

1.2 Covered by the Honble Supreme Court: And it is very settled law that no addition can be made only on the basis of third party statements and the statements which has been retracted and when no incriminating documents has been found during the course of search in the possession of assessee. And no addition can be made on the basis of documents found at the premises of third parties until and unless the same is not provides and confronted to the person in his hand the additions are proposed . The Hon’ble Supreme Court in decision dated 02.09.2015 in case of Andaman Timber Industries Vs. CCE 127 DTR 0241 held that denial of opportunity to the assessee to cross-examine the witnesses whose statements were made the sole basis of the assessment is a serious flaw rendering the order a nullity in as much as it amount to violation of principles of natural justice. Copy of order is enclosed.

The assessee also referred the following judgments in his supports

In Pullangode Rubber Produce Co. Ltd. vs State of Kerela [1973]19 ITR 18 (SC).

In CIT v. Lavanya Land (P.) Ltd. [2017] 83 taxmann.com 161 (Bom.) Where seized documents were not in name of assessee no action could have been undertaken in case of assessee under section 153C and further entire decision being based on huge amounts revealed from seized documents not being supported by actual cash passing hands, additions under section 69C were not sustainable. Upheld by Supreme Court in Principal Commissioner of Income-tax, Central III vs. Krutika Land (P) Ltd. [2019] 103 taxmann.com 9 (SC)

In CIT -1 vs. Mantri Share Brokers (P) Ltd. [2018] 96 taxmann.com 279 (Rajasthan)

Upheld by Supreme Court in Commissioner of Income-tax-1 vs. Mantri Share Brokers (P) Ltd. [2018] 96 taxmann.com 280 (SC)

In CIT Vs. Bhanwar Lal Murwatiya[2008] 215 CTR 489 (RAJ.), In CIT v/s Ashok Kumar Soni 291 ITR 172 (Raj.), The jurisdictional Rajasthan High Court has observed that ‘It is trite to say that admissions are relevant piece of evidence and are not conclusive proof of fact. An admission can always be explained once this position is accepted, the question remains of appreciating evidence which is on record, which includes the evidence in the form of attending circumstances and the statements by which the previous statement is sought to be explained.’

KrishanLal Shiv Chand Raivs Commissioner Of Income-Tax 1973 88 ITR 293 P H-

In Gajjam Chinna Yellappa Vs Income tax Officer [2015] 59 taxmann.com 69 (Andhra Pradesh and Telangana)

In case of Chitra Devi v/s ACIT (2002) 28 Tax-world 454 (ITAT JP)

Shri PawanLashkary ITA No 808/JP/2011 dated 06.01.2012 –

Agarwal Warehousing & Leasing Limited VsCIT(2002) 257 ITR 235 (MP)

State of Kerala v. K T. Shaduli Yusuf (1977) 39 STC 478, Kishan Chand Chellaram v. CIT (1980) 125 ITR 713 (SC) Monga Metals Pvt. Ltd. v. ACIT 67 TT] 247 (All.)

In case of Smt. Sunita Dhadda vs DCIT [2013] 33 Taxmann.com 639 (Jaipur – Trib.),Hon’ble tribunal ruled that Where Assessing Officer, while making addition on account of ‘on money’ received by assessee on sale of land to a builder group, relied upon statement of director of that group and did not allow assessee to cross-examine said person, there was violation of principle of natural justice and, therefore, addition could not be sustained. The same has been upheld by Hon’bleRajsthan High Court on 31/07/2017 and SLP by Revenue in Supreme Court has been dismissed.

The jurisdictional Jaipur ITAT has consistently followed principles as laid down by Supreme Court in case of Andaman Timber Industries and gave relief to the assesses.

As far as case laws referred by learned AO, on one side all those have been over ruled by the latest decisions of Supreme Court and High Courts and on other side those case are not applicable in case of the assessee. The circumstances of the case of assessee are such that addition has been made only on the basis of statements of other persons and cross examination was essential to bring out correct facts and to discredit the testimony of those persons.

Manorama Singhal vs. ITO ITA No. 130/Ind/2020 21-Sep-2021 (2021) 63 CCH 0096 IndoreTrib

Thus no addition can be made looking to the above facts and judicial pronouncements.

2. Retraction with Affidavit filed by assessee cannot be discarded without corroborative material evidences:

2.1 The ld. AO has ignored blindly that the whole of the retraction affidavit is relevant in this appeal.The ld. AO has made addition of Rs.1,17,20,000/-in income on the basis of statements of the assessee and statement of Mr. Harpal Yadav which were recorded u/s 132(4) during search proceedings in his case behind the back of assessee and there is no incriminating document found at the premises of assesseeto substantiate the finding of AO. The assessee has retracted from his search statements by filing an affidavit dated 19/06/2017(PB1-6). But the ld. AO has not rebutted the same with the help of any contrary evidence rather he has recorded the statement of the assessee u/s 131 on dt. 03.05.2018 (PB 43-47). As also stated in his retraction that the search statement were not recorded properly. Details are mentioned in retraction affidavit.

2.1.1. Further the contention made in the letter of affidavit should be accepted as truth unless rebutted. Because these affidavits have not been rebutted by lower authority by bring any contrary evidence or without examining. It is very settled legal position that in the cases where affidavit has been filed yet the contents thereof have not been rebutted by the AO/authority, the facts mentioned therein have to be read as the facts binding upon the Income Tax authorities. Kindly refer Mehta Pareek& Co. 30 ITR 181 (SC), ITO v. Dr. Tejgopal Bhatnagar 20 TW 368 (Jp) Paras Cotton Company vs. CIT (2003) 30 TW 168 (JD)., CIT v/s Lunard Dimond Ltd. 281 ITR 1 (Del). Recently in CIT v/s Bhawani Oil Mills (P) Ltd 239 CTR 445/49 DTR 212(Raj.)- It has been held that contents of affidavit could not be treated as of a lesser importance than the statement given by the creditor before the AO.

And in the present case in support the assessee had filed his affidavit and the ld. AO has not rebutted the contents of the affidavit even he examined to the person it mean either he was satisfied or he has no material to disprove the same. If the AO has failed to give any comments thereon, then in-absence of the same how some comments can be made on the same without asking any question from the assessee for clarifications if any in the amount. An affidavit is the important piece of evidence, should not be taken in light and if there is any wrong affidavit is given by any of the party or person the same is offence and may be punished under the law. In absence of the same the same cannot be discarded but is the evidence of the acceptance. The affidavits are evidence until and unless not disproved by the authority who alleging the same.

As Section 191 of the Indian Penal Code stipulates:

“Whoever being legally bound by an oath or by an express provision of law to state the truth, or being bound by law to make a declaration upon any subject, makes a statement which is false, and which he either knows or believes to be false or does not believe it to be true, is said to give a false affidavit”

Section 193 of the Indian Penal Code, 1860 lays down the punishment for false evidence- whosoever intentionally gives a false evidence for the purpose of being used in a judicial proceeding, shall be punished with imprisonment which may extend up to 7 years and shall also be liable for payment of fine.

In light of the above, it can be concluded that an affidavit is a document of extreme importance and value. Although, it can be signed by Principal Officers as well as their authorized representatives, it is expected that it is signed only by persons who are fully aware of the facts and circumstances of the case.Affidavit is treated as “evidence” within the meaning of Section 3 of The Evidence Act.

In the case of Prashant Vs. Muncipal Council Bhadravat AIR 2009 BOM 144 it has been held The provisions of Civil Manual, Chapter XXVI,para 506 read thus -506. The person who may administer oaths to deponents must be duly authorised under Section 139 of the Civil Procedure Code to do so. It would thus mean that the persons who may administer oath to the deponents are to be the persons who are authorized under Section 139 of C.P.C. to do so. Therefore, the result is obvious that the Notaries are authorized to administer oath to the deponents.11The affidavits which are to be under the Code, can be sworn by on administering the oath to the deponents by any Notary appointed under the Notaries Act and under Order 18, Rule 4 of the C.P.C., there is no bar requiring to exclude the affidavits sworn before the Notaries for taking them on record as an examination in chief. Thus, such affidavits sworn before Notaries can be accepted as evidence by the Civil Court. The cumulative sequel would render the impugned order to be incorrect and illegal at law. As such liable to be quashed and set aside.

Thus the silver ornaments, utensil etc. weresince past more than hundred years. None of the silver ornaments or utensils were acquired during the search period. Looking to the status of the family and the system and culture prevailing in the society the claim of 84458 gm. silver utensil belonging to family members should have been accepted and should not be doubted.

2.2 Statements u/s 131 has been ignored: Furthermore it is very important to note that during the course of assessment proceedings, to verify the truth of the retraction affidavit filed by assessee, the statements of assessee were recorded u/s 131 on dt. 03.05.2018 by the ld. AO. In those statements, the assessee reiterated the contents of retraction affidavit and stated that he had not surrendered any undisclosed income as alleged in statements recorded on 19/11/2016. However the ld. AO has not spoken a single word on the statements recorded by him u/s 131 on dt. 03.05.2018 in the assessment order nor he stated that the statements u/s 131 are not correct or not acceptable, rather he rejected his retraction concealing or ignoring these vital facts and evidences and proceeded to make addition solely on basis of statements dated 19.11.2016. It shows the contradictory approach of the ld. AO. If there was any wrong in the statement u/s 131 the ld. AO should have initiated the penal proceedings. Both the statements must be read together.

Also clearly denied in the statements recorded u/s 131

3. Correct Facts and Transactions: While overall looking to the search statements of assessee and his retraction affidavit, statement of Harpal Yadav and submissions during the assessment proceedings and the assessment order, the correct facts that emerges and the submission of assessee is as follows:

Shop No. 16, Kardhani, Govindpura, has been purchased by sons and nephews of assesseeviz. Manoj, Rajkumar, Kailash and Shankar for Rs. 32,80,000/- and whole of the consideration had been paid vide 4 cheques of Rs. 8,20,000/- each. The assessee has himself not purchased that property. During assessment proceedings the assessee vide letter dated 05/11/2018, submitted the copies of the bank statements and ITRs of his sons and nephews to establish the transaction having been done by them on their own account. It was not that the assessee purchased shop for them. The learned AO did not bring this submission of assessee on record.

Further it was Satya Prakash Bhutiya and Jitendra Bhutiya who sold the shop to sons and nephews of assessee. Kailash Bhutiya was not the seller of the shop.

Neither the name of assessee is written on the loose slip nor the nature of transaction is written on this paper. But learned AO, on the basis of this slip, has stated in the assessment order (para 5) as follows:

Considration of Rs. 1.50 crores around 2 year back. Shri Harpal Yadav admitted that Rs. 1,27,50,000/- were paid in cash and Rs. 30,50,000/- were paid by cheque by Shri Jai Singh Yadav to Bhutias. Relevant Part of his statement is reproduced below:

It may also be noted that there was no cheque of Rs. 30.50 lakh being given for purchase of shop by assessee’s sons and nephews. It clearly establishes that the said slip of paper does not in any way relate to assessee.

Further Mr. Harpal has also stated that there were 2 contractors who were mediators in the deal of sale of shop by KailashBhutia to GopalLalYadav and Jai Singh Yadav. It is not clear that when Mr. Harpal was himself not a part of the alleged deal, then how could he state that the sale of shop was done for Rs. 1.50 crore and the reason is best known to him. The assessee asked for cross examination of Mr. Harpal Yadav, but it was not granted by learned AO.

Further Mr. HarpalYadav has stated that the deal of sale of shop was done 23 years back, but Shop No. 16 has been purchased by sons and nephews of assesses in Aug, 2015 which was just more than a year back. This again shows that Mr. HarpalYadav seems to be confused or trying to say something else.

4. No additions can be made without any material found during the course of search or no incriminating documents found during the course of search: Further we have to submit that no additions were called for in the assessment u/s 153A or 143(3) for the year under consideration, in the present case, admittedly no incriminating material has been found or seized from the premises of assessee which could substantiate or corroborate the payment of on money in the said transaction of purchase of shop. The learned AO has also not brought on record any material or corroborative evidence which could establish the alleged payment of on money by the assessee to Sh. Kailash Bhutiya. Thus considering the fact that there was no material evidence found during the course of search admittedly. As per settled law and legal position, as there was no incriminating documents/material found during the course of search hence no addition can be made in the assessment u/s 153A. This legal issue has been decided in so many cases and becomes a settled law by now according to which no addition can be made in the assessment u/s 153A in absence of any incriminating documents or material from which it can be inferred or which can suggest that there was income derived by the assessee in the year under consideration which was not disclosed by him prior to the date of search. Even no addition can be made in the assessment u/s 153A on the basis of statement u/s 132(4) in absence of incriminating material found during the course of search. Addition towards undisclosed income without establishing the basis found during the course of search could not be sustained. The assessment u/s 153A should focus on the basis of material and evidences gathered during the course of search. In this respect assessee relied upon the following judgments:

(i) CIT V/s Deepak Kumar Agrawal and others (2017) 299 CTR(Bom) 62

(ii) CIT and Anr V/s Lancy Constructions (2017) 295 CTR (Kar)

(iii) CIT V/S KABUL CHAWALA(2016) 380 ITR 573.The ratio of above judgment is also followed in the case reported at (2017) 295 CTR (DEL) 466.

(iv) PCIT V/s Saumya Construction P Ltd. (2017) 297 CTR(Guj) 387

If in relation to the assessment year, no increment material is found, no addition and disallowance can be made in relation to that assessment year in exercise of power u/s 153A and the earlier assessment shall have to be reiterated.

Covered matter: Here also the same position because admittedly in the present case there is no incriminating documents have been founds admittedly and the ld. AO has made the addition on the basis of documents and statements of third party which have not been confronted despite the request made by the assessee. Hence the above matter is directly covered matter by the following judgments.

In the group cases the Honble ITAT Jodhpur Bench Jodhpur in the case of Chhoga La lJain(Maroo), Leela Devi Jain(Maroo) and Vijay Jain v/s DCIT Central Circle-1 Udaipur in ITA No. 128,129,130,131,132/Jodh//2019 dt. 28.11.2019

Rathi Rathi Steel Ltd. &ANR. vs. ACIT&ANR. 31st May, 2019 (2019) 56 CCH 0102 DelTrib.

PCIT v/s Meeta Gutgutia Prop. Ferns Patel &Ors 395 ITR 526(Del). Further the SLP filled by the revenue has been dismissed by the Honble Supreme Court vide order dated 02.07.2018 257 Taxman 441(SC)

Pr. CIT. Dharampal Premchand Ltd.(2018) 408 ITR 0170 (Delhi).

Pr.CIT-18 vs Ms. Lata Jain [2017] 81 Taxmann.com 83 (Delhi)- In Pr.CIT-V vs Vikas Gutgutia [2017] 88 taxmann.com 605 (Delhi)-

Hence, we request your good self to please delete the addition in this ground alone.

The ld. AO has not brought on record material or corroborative evidence any to prove that assessee had any other source of income other than that declared by him and that assessee earned more than what he had declared in his return of income.There is nothing on record which could establish the earning of Rs. 1,17,20,000/- even from undisclosed source. There has to be at-least a way out of which assessee may have earned the amount in FY 2015-16 itself. The amount of Rs.1,17,20,000/- is a huge amount and the assessee is not involved in any activity which could generate this sum in cash.The learned AO has not made any findings rather has mechanically added the amount while she ought to have supported the addition by findings on the basis of seized material.

5. No addition or action in the hands of the seller: The transaction of sale couldn’t be one way. If assessee had paid on-money, then Mr. KailashBhutiya must have received it as his undisclosed income. But it can be noted that no such fact has been brought on record by the learned AO and no action have been taken against Mr. KailashBhutiya. The assessee had requested the cross examination of person who says that assessee had paid the onmoney, but it was not given, which could only be for the reason that there is no person who received the alleged onmoney.

6.Covered matter on “On money”:Further when the ld. AO herself made the addition of 5.00 crore in the hands of assessee and Sh. Gopal Lal Yadav on account of on money received by the assessee from M/s Kedia Real Estate LLP where the director Sh. NirmalKedia has stated in his statements recorded u/s 132 (4) on dt. 19/20.11.2016 itself that he has paid on money of Rs.5.00 crore to Sh. Jai Singh (assessee) for purchase of 3 bhiga 18 biswa land from Sh. Jai Singh. And the addition has also been made in the hands of M/s Kedia Real Estate LLP ( although the additions have been deleted in the appellate proceedings). Then when no addition has been made in the hands of the seller then why the addition should be made in the hands of the assessee. It means the ld. AO has deemed or accepted that no on money was received by Sh. Kailash Bhutiya otherwise he could have recorded the statements of Kailash Bhutiya or addition could have also been made in his hands as undisclosed income. It clearly shows the contradictory approach of the ld. AO and also proved that the addition of Rs.1,17,20,000/- is baseless and on surmises and conjectures, without any material and liable to be deleted. The ld. CIT(A) has also ignored all these above facts and submission all together.

Further under the same facts and circumstances and under the same search the this Honble ITAT has deleted the addition on account of On Money vide order in In the case of ACIT Central Circle- Jaipur v/s M/s Kedia Real Estate LLP in ITA No. 127 & 289/Jp/2019 dt.03.06.219 copy is enclosed.

Directly covered matter: It is further submitted that the above matter is now directly covered by the decision of Honble ITAT Jaipur and jodhpur Bench wherein under the same facts and circumstance and in same matter the honble ITAT Jaipur bench has deleted the addition in the case of Gauri Shankar Sharma v/s ITO Ward 2(1), Jaipur in ITA No. 35/Jp/2018 dt. 10.04.2019 copy is enclosed. Also refer Dhirendra Singh V/s ITO in ITA No. 1273/Jp/2018 dt. 25.03.2019.

Mukesh Choudhary vs. ITO (2020) 58 CCH 0363 JodhTrib

Jiterndra Ojha vs. ITO (2020) 58 CCH 0369 JodhTrib

Further we would like to submit that the case laws relied upon in this order and arguments given in this order both may also be considered as cited or given by us before your honor. We are not repeating the same to avoid multiplicity.

7. The ld. AO has contended that after receiving the copy of search statement of Harpal Yadav the assessee did not submit to prove the contrary. But it may be noted that the assessee had asked for the copy of the slip on the basis of which HarpalYadav gave his statement and also requested for cross examination. The assessee believed that it was only after the receipt of required document and opportunity to cross examine that he could logically bring out the correct facts and mere objecting to statements may be of no use. But when these facts had come before the ld. CIT(A) she could have asked the ld. AO to produce the slip but she also did not commented or do so rather confirmed the action of the ld. AO.

8. Comparable sale deed ignored: During the course of search proceedings, purchase deeds of other 2 shops purchased in same B-Block of Kardhani Scheme were also found(Page nos. 35 -58 of Exhibit No. 2 of Seized Documents). These shops were bearing no. 19 and no. 15were purchased in FY 2012-13 for Rs. 25 lakh and Rs. 24 Lakh respectively. Both shops are of same size as Shop No. 16 which is subject matter of this onmoney and are also in the same B-Block in which Shop No. 16 is located. These are in-fact comparable transactions and established the true value of the property in the said area. It may be seen that while value of 1 shop in 2012-13 was Rs. 24 lakh it has increased to Rs. 32.80 lakh in year 2015-16 which is increase of approx.36% during 3 years’ time frame which is practical. And both the lower authorities were keep mum on these vital facts. There was also no case of purchase of shop in lower rate of DLC.

Thus the price at which this shop no. 16 had been purchased was reasonable and at or above the DLC rates declared by State. The presumption of valuing the shop at Rs. 1.50 crore is baseless.

Although the purchase deeds were on record but the assessee again explained regarding purchase of all these shops in letter dated 05/11/2018.

9. As per Section 142(3) of Income Tax Act states as under:

‘The assessee shall, except where the assessment is made under section 144, be given an opportunity of being heard in respect of any material gathered on the basis of any inquiry under sub-section (2) or any audit under subsection (2A) and proposed to be utilised for the purposes of the assessment.’

It clearly shows that it was legal duty of learned AO that she should have provided the copy of document on the basis of which Mr. Harpal gave his statement and copy of statements of any other person who has stated of receiving on money from assessee. The assessee should have also been provided the opportunity of cross examination of HarpalYadav and others, but neither the document was provided nor the opportunity to cross examine was given.

The Honble Supreme Court in case of Surajmal Mohta & Co. vs. A V VisvanathSastry (1954)26 ITR 2(SC) has observed that the proceedings before the Income Tax Officer are judicial proceedings and all the incidents of such judicial proceedings have to be observed before the result is arrived at. In other words, the assessee would have a right to obtain copies of records and all relevant documents before he is called upon to lead evidence in rebuttal. This right has not been taken away by any express provision of Income Tax Act.

10. No additions made on the same ground in case of assessee’s brother Gopal Lal Yadav: It is also to be noted that under the similar question regarding on-money on purchase of shop and alleged surrender of undisclosed income in that respect was also done in the statements recorded u/s 132(4) in case of the assessee’s brother Sh. Gopal Lal Yadav. Sh. Gopal Lal Yadav also retracted from the said surrender statement and submitted his reply in response to show cause notice during assessment proceedings (Copy of relevant portions of his statements and retraction affidavit are enclosed at PB Page No.29-35).

It may be noted from the assessment order of Shri Gopal Lal Yadav for AY 2016-17 that the ld. AO has accepted the reply of assessee and has not made any addition on this ground (Copy of assessment order is at PB Page No.36-39D). Thus while AO has accepted the submission in one case but has rejected the submission on same issue in the case of assessee which is not tenable. And her own contradictory and against the principal of law. The ld. AO has also not stated that why the addition is being made in the hands of the assessee and not being made in the hands of Sh. Gopal Lal Yadav. In absence of the same addition could not be made.

11. No addition could be made on the basis of a dumb document:

The seized material and transaction noted on the loose paper found in the possession of third party did not reflects any transaction that only rough estimated paper, on this paper neither any date, nor any signature nor any correlated entry by the assessee found.

Thus no addition can be made on basis of dumb document On this preposition the assessee referred following decisions.

CIT v/s SM Aaggrawal 293 ITR 43(Del).

CIT v/s Grish Choudhary 296 ITR 619(Del)

CIT v/s Jai Pal Agrawal 91 DTR 327 (Del)

ACIT v/s Rakesh Goyal 87 TTJ 151 (Del)

Pankaj Dahyabhai Patel (HUF)* vs. ACIT 63 TTJ 79(Ahd)

In the case of Jayanti Lal Patel vs. ACIT & ORS. High Court Of Rajasthan : Jaipur Bench (1998) 233 ITR 588 (Raj).

In the case Mahaan Foods Ltd. vs. DCITV ITAT, DELHI ‘C’ BENCH (2010) 123 lTD 590

v) ACIT vs. Satyapal Wassan ITAT, JABALPUR BENCH (2008) 5 DTR (Jab)(Trib) 202

ACIT Central Circle- Jaipur v/s M/s Kedia Real Estate LLP in ITA No. 127 & 289/Jp/2019 dt.03.06.219 copy is enclosed.

12. The AO proceeded on suspicion and it is settled principlesthat suspicion may be strong but cannot take the place of reality, kindly refer Dhakeshwari cotton Mills 26 ITR 775 (SC), Uma Charan Shaw v/s CIT 37 ITR 271 (SC).

13. Addition if any was to be made u/s 153C not 143(3): Further it is submitted that the addition of Rs. 1,17,20,000/- has been made on the basis of statements of Harpal Yadav who gave his search statement in relation to the loose paper found in his premises. And the addition of Rs.2,44,93,451/-was made on the basis of statements of Nirmal Kedia recorded u/s 132(4) in whose case search was carried out u/s 132. Thus it is established that the material, if any, on the basis of which addition has been made was not found in the premises of assessee admittedly and thus neither action could be taken under section 153A nor any addition. The addition if any could have been made only after issuing notice under section 153C after recording the satisfaction by the AO of other search persons and making assessment there upon. The learned AO has not acquired any jurisdiction under section 153C and thus the addition of Rs. 1,17,20,000/- as well as the addition of Rs.2,44,93,451/- (in both assessee are is illegal and should be deleted. This is without prejudice to assessee’s claim that the alleged addition was otherwise also illegal and liable to be deleted.

On this Preposition the assessee has relied upon on the decision of Delhi High Court in case of Pr. CIT(Central) & Ors. V/s Anand Kumar Jain (HUF) & Ors. 432 ITR 384(Del).

14. Addition of Rs. 1,17,20,000/- made under section 68 is illegal: The learned AO has made addition of Rs. 1,17,20,000/- under the provisions of Section 68 of Income Tax Act.

Section 68 states as follows:

“Where any sum is found credited in the books of an assessee maintained for any previous year, and the assessee offers no explanation about the nature and source thereof or the explanation offered by him is not, in the opinion of the Assessing Officer, satisfactory, the sum so credited may be charged to income-tax as the income of the assessee of that previous year”

In the present case neither the assessee maintained any books of account nor any amount has been found credited in even any document, thus Section 68 is squarely not applicable in case of assessee and the addition made there under is illegal and void ab initio. Thus addition of Rs. 1,17,20,000/- made under section 68 should be deleted in full.

11.1. Further during the assessment proceedings, the assessee had requested for cross examination of Mr. Harpal Yadav, Mr. Nirmal Kumar Kedia and any other person who had owned the payment of on-money to assessee, by way of written request as well as orally. The assessee also requested for copy of document i.e paper slip on the basis of which Mr. Harpal Yadav gave his statements. But the ld. AO has neither given opportunity to cross examine nor she provided copy of paper slip in relation to which Mr. Harpal Yadav gave his statement. And on this aspect we have already submitted hereinabove.

11.2 The copy of statement of assessee recorded under section 132(4) were not given to assessee inspite of repeated oral reminders to ADIT(Inv) together with letters dated 11/01/2017 & 21/03/2017 . It was on 11/05/2017, that the assessee received copy of his statements from Central Circle-3. The assessee then found that there is alleged surrender of income being recorded in his statement taken on 19.11.2016.

Till the receipt of the copy of statement the assessee genuinely believed that he had not surrendered any income for taxation and that no incriminating material have been discovered in search, therefore he did not file any retraction statement. But on receipt of copy of his statements on 17/11/2017, he was astonished to note the surrender of income and after complete understanding of the contents of his statements dated 19.11.2016, he sworn in a Retraction Affidavit on 19/06/2017 wherein he retracted from the surrender of any undisclosed income for taxation. After the affidavit was filed before the assessing authority, the AO remained silent on the face of it and carried no enquiry thereon to verify the correctness thereof.

The assessee also referred in his retraction affidavit (para no. 7) that some of the questions asked from him and replies said to be made by him were completely identical to the questions and answers recorded in case of statements of his brother Gopal Lal Yadav, while the time of statements recorded was different and the persons recording statements were different in both cases. This fact concludes that the statements were not recorded properly. The assessee has also referred to various question numbering 34, 35, 36, 43 & 47 which have either not been asked at all or have been asked in different manner but the reply has been recorded as per the wish of the person recording the statement. ‘’

2.6 During the course of hearing, the ld. DR supported the orders of the authorizes below and stated that the addition was made on the basis of material seized from Sh. Harpaal Yadav alongwith his statement was recorded during search and also confronted to the assessee.

2.7 We have heard the rival submissions perused the materials available on record and also noted that as the AO has made addition of Rs.1,17,00,0000/- on account of On-Money paid to Sh. Kailash Bhutiya only on the basis of document seized in the premises of Harpal Yadav during search and the statement of Sh. Harpal Yadav recorded u/s 132(4), although the statement of Harpal Yadav was confronted to the assessee who confirmed the statement of Sh. Harpal Yadva. However, after meticulously inspecting the record and material placed before us, it is an admitted facts that the assessee has asked for the statements recorded u/s 132(4), After receiving the copy of statement he has retracted from the statement regarding the any On-Money given by him to Sh. Kailash Bhutiya through the Affidavit dt. 19.06.2017 placed at PB1-6 and after filling the retraction cum affidavit. The AO has also recorded the statement of the assessee u/s 131 on dt. 03.05.2018 wherein assessee has clearly denied of giving any On-Money of Rs.1,17,00,000/- to Sh. Kailash Bhutiya for purchase of the said Shop by his sons from sons of Sh. Kailash Bhutia, thus the retraction has been again confronted by the AO and assessee has affirmed the same again, the copy of the same is placed at PB 43-47. However the AO has not spoken any things and adverse on the statements recorded u/s 131 by herself during the course of assessment proceedings. Further when the assessee sought cross examination of Sh. Harpal Yadav the AO has straight away denied the same. When it is now a settled principal of law that no addition can be made only on the basis of statements of the third party without providing opportunity of cross examination of the person when specifically asked by the assessee in whose hand the addition has been made. This issue is supported by the decision of The Hon’ble Supreme Court in case of Andaman Timber Industries Vs. CCE 127 DTR 0241 dated 02.09.2015 wherein it has been held that denial of opportunity to the assessee to cross-examine the witnesses whose statements were made the sole basis of the assessment is a serious flaw rendering the order a nullity in as much as it amount to violation of principles of natural justice. The Honble Supreme Court has held while dealing with the issue whose relevant para 5 to 8 are as under:

“5. We have heard Mr. Kavin Gulati, learned senior counsel appearing for the assessee, and Mr. K. Radhakrishnan, learned senior counsel who appeared for the Revenue.

6. According to us, not allowing the assessee to cross-examine the witnesses by the Adjudicating Authority though the statements of those witnesses were made the basis of the impugned order is a serious flaw which makes the order nullity inasmuch as it amounted to violation of principles of natural justice because of which the assessee was adversely affected. It is to be borne in mind that the order of the Commissioner was based upon the statements given by the aforesaid two witnesses.

Even when the assessee disputed the correctness of the statements and wanted to cross-examine, the Adjudicating Authority did not grant this opportunity to the assessee. It would be pertinent to note that in the impugned order passed by the Adjudicating Authority he has specifically mentioned that such an opportunity was sought by the assessee. However, no such opportunity was granted and the aforesaid plea is not even dealt with by the Adjudicating Authority. As far as the Tribunal is concerned, we find that rejection of this plea is totally untenable. The Tribunal has simply stated that cross-examination of the said dealers could not have brought out any material which would not be in possession of the appellant themselves to explain as to why their ex-factory prices remain static. It was not for the Tribunal to have guess work as to for what purposes the appellant wanted to cross-examine those dealers and what extraction the appellant wanted from them.

7. As mentioned above, the appellant had contested the truthfulness of the statements of these two witnesses and wanted to discredit their testimony for which purpose it wanted to avail the opportunity of cross-examination. That apart, the Adjudicating Authority simply relied upon the price list as maintained at the depot to determine the price for the purpose of levy of excise duty. Whether the goods were, in fact, sold to the said dealers/witnesses at the price which is mentioned in the price list itself could be the subject matter of cross-examination. Therefore, it was not for the Adjudicating Authority to presuppose as to what could be the subject matter of the cross-examination and make the remarks as mentioned above. We may also point out that on an earlier occasion when the matter came before this Court in Civil Appeal No. 2216 of 2000, order dated 17.03.2005 was passed remitting the case back to the Tribunal with the directions to decide the appeal on merits giving its reasons for accepting or rejecting the submissions.

8. In view the above, we are of the opinion that if the testimony of these two witnesses is discredited, there was no material with the Department on the basis of which it could justify its action, as the statement of the aforesaid two witnesses was the only basis of issuing the Show Cause Notice.”

Further Recently the Honble Raj. High Court in the case of Pr. CIT, Jaipur-2 v/s Sh. Sanjay Chhabra in DBIT No. 22/2021 dated 06.04.2022, the Honble HC held that :-

“ The Tribunal by impugned order has categorically held that the material information received by the Assessing Officer from the investigation wing alongwith certain statements recorded byDBIT Investigation, Calcutta could not be taken into considerationas that material was not disclosed nor an opportunity was accorded for cross-examination of the Assessee. This finding recorded by the Tribunal cannot be said to be perverse or suffering from any patent illegality. Learned counsel for the Revenue could not satisfy us with reference to any judgment on this aspect that even without disclosing any material to the Assessee and without allowing him proper cross-examination, such undisclosed and unverified material could be taken into consideration for the purposes of addition.

The Tribunal’s findings are based on material placed on record. The aspect of human probability, in the present case, only goes against the Revenue because in the present case, a raid was conducted and in that process, statement is said to have beenrecorded under Section 132(4) of the I.T. Act, which was, later on,retracted by the Assessee. In a situation like this, where the officepremises are sealed for many days and during that period, astatement is said to have been recorded under Section 132 (4) ofthe I.T. Act, the Tribunal’s view that only the basis of suchretracted statement, addition could not be justified without anyother material admissible in evidence, warrants no interference asit is not a substantial question of law.

In the case of Commissioner of Income Tax Versus Harjeev Aggarwal reported in (2016) 290 CTR (Del) 263 and Kailashben Manharlal Chokshi Versus Commissioner of Income Tax reported in (2010) 328 ITR 411 (Guj) variousHigh Courts have held that addition based solely on statement later on retracted, without anything more, could not be justified in law. Thus, the view taken by the Tribunal cannot be faulted.

In view of the above consideration, we are of the view thatthis appeal does not involve any substantial question of law and is,therefore, dismissed.”

In the case of Smt. Sunita Dhadda vs DCIT [2013] 33 Taxmann.com 639 (Jaipur – Trib.),Ttribunal ruled that Where Assessing Officer, while making addition on account of ‘on money’ received by assessee on sale of land to a builder group, relied upon statement of director of that group and did not allow assessee to cross-examine said person, there was violation of principle of natural justice and, therefore, addition could not be sustained. The same has been upheld by Hon’bleRajsthan High Court on 31/07/2017 and SLP by Revenue in Supreme Court has been dismissed. It is noted there is the same position in the case of the assessee because no cross examination has been provided and it was against the Principal of natural justice, thus Respectively following the Judgement of the Honble Apex Court and Jurisdictional High Court , No addition is liable to made in the case of assessee also. Further when the assessee has retracted the statement through the affidavit and there was no material found in his possession as In Pullangode Rubber Produce Co. Ltd. vs State of Kerela [1973]19 ITR 18 (SC) the Supreme Court has held that ‘An admission is an extremely important piece of evidence but it cannot be said that it is conclusive. It is open to the person who made the admission to show that it is incorrect. The ld. A/R of the assesse has also furnished the copy of this Co-Ordinate Bench the case of ACIT Central Circle- Jaipur v/s M/s Kedia Real Estate LLP in ITA No. 127 & 289/Jp/2019 dt.03.06.219 of same search case where in under the same facts and circumstances this Co-Ordinate Bench has deleted the addition on account of On Money vide order. Thus also no addition is liable to made. Further it also noted that the AO has not provided the copy of seized document found at the premises of third party i.e Mr. Harpal who gave his statement and the addition was made despite the request by the assessee vide page 73PB of the assessee and no addition can be made without confronting or providing the documents to the assesse. It is also an admitted fact that no incriminating documents were found in the premises/ possession of the assessee during the course of search operation. Hence, no addition can be made in the hands of the assessee without any corroborative and incriminating documents found during the course of search. To this effect, the ld. AR of the assessee relied on following case laws.

CIT V/S KABUL CHAWALA(2016) 380 ITR 573

Rathi Rathi Steel Ltd. &ANR. vs. ACIT&ANR. 31st May, 2019 (2019) 56 CCH 0102 DelTribIt

PCIT v/s Meeta Gutgutia Prop. Ferns Patel &Ors 395 ITR 526(Del) held

Further the ld. AR has drawn our attention on the statement of Sh. Gopal Lal Yadav brother of the assessee where under the similar question regarding On-Money on purchase of shop and alleged surrender of undisclosed income in that respect was also done or obtained in the statements recorded u/s 132(4) in case of the assessee’s brother Sh. Gopal Lal Yadav vide PB 29-30. Shri Gopal Lal Yadav had also retracted said surrender statement and submitted his reply in response to show cause notice during assessment proceedings and relevant portions of his statements and retraction affidavit are placed at PB Page No.29-35. However the same AO while passing the assessment order in the case of Shri Gopal Lal Yadav has not made any addition on this ground and copy of which is placed at Paper Book Pages 36-39D, otherwise she should have made 50-50% addition if any. It shows that there is contradictory approach of the AO in making wrong addition on this account. It is also noteworthy to mention that AO made the addition of Rs. 1,17,20,000/- on the basis of statements of Harpal Yadav who gave his search statement u/s 132(4) in relation to the loose paper found in his premises but no material on this account was found in the possession of the assessee. As per the provisions of Sec. 153C, the material, if any, on the basis of which addition is to be made was not found in the premises of assessee then neither action could be taken under section 153A nor any addition u/s 153A can be made. The addition if any could have been made only after issuing notice under section 153C after recording the satisfaction by the AO of other search persons. In the present case the AO has not assumed any jurisdiction under section 153C rather than made the addition u/s 153A. The Honble Delhi High Court in case of Pr. CIT(Central) & Ors. V/s Anand Kumar Jain (HUF) & Ors. 432 ITR 384(Del) held as under:

“3. A search was conducted u/s. 132 on 18th November, 2015 at the premises of the Assessee {being Anand Kumar Jain (HUF), its coparceners and relatives} as well as at the premises of one Pradeep Kumar Jindal. During the search, statement of Pradeep Kumar Jindal was recorded on oath u/s. 132(4) on the same date, wherein he admitted to providing ITA 23/2021 and connected matters Page 4 of 11 accommodation entries to Anand Kumar Jain (HUF) and his family members through their Chartered Accountant. The assessing officer framed the assessment order detailing the modus operandi as to how the cash is provided to accommodation entry operator in lieu of allotment of shares of a private company. Thereafter when the matter was carried up in appeal before the CIT(A), the findings of AO were affirmed. However, in further appeal before the ITAT, the said findings were set aside vide the impugned order.

4. The Revenue is aggrieved with the aforesaid impugned order and has filed the present appeal under Section 260A of the Act, proposing the following questions of law…..

10. Now, coming to the aspect viz the invocation of section 153A on the basis of the statement recorded in search action against a third person. We may note that the AO has used this statement on oath recorded in the course of search conducted in the case of a third party (i.e., search of Pradeep Kumar Jindal) for making the additions in the hands of the assessee. As per the mandate of Section 153C, if this statement was to be construed as an incriminating material belonging to or pertaining to a person other than person searched (as referred to in Section 153A), then the only legal recourse available to the department was to proceed in terms of Section 153C of the Act by handing over the same to the AO who has jurisdiction over such person. Here, the assessment has been framed under section 153A on the basis of alleged incriminating material (being the statement recorded under 132(4) of the Act). As noted above, the Assessee had no opportunity to cross-examine the said witness, but that apart, the mandatory procedure under section 153C has not been followed. On this count alone, we find no perversity in the view taken by the ITAT. Therefore, we do not find any substantial question of law that requires our consideration.

11. Accordingly, the present appeals, along with all pending applications, are dismissed.”

Thus the assessment as well as addition u/s 153A are wrongly made and liable to be deleted. Further the AO has also made the addition u/s 68 which is also incorrect or wrong in view of above deliberations. Thus in view of the above facts, circumstances and legal position of the case, the addition of Rs.1,17,00,000/- sustained by the ld. CIT(A) is deleted and grounds of appeal No.1,3 & 4 of the assessee are allowed.

3.1 During the course of hearing, the AR of the assessee has not pressed the Ground No.2 which is dismissed being not pressed.

4.1 The Ground No. 5 of the assessee is regarding charging of interest 234B which is consequential in nature and does not require any adjudication.

5.1 Now we take up Departmental Appeal in ITA NO. 168/JP/2022 wherein the solitary ground of the Department is deletion of addition of Rs. 2,44,93,451/- on account of Long Term Capital Gain.

5.2 Brief facts of the issue in question are that the AO has observed that it is was noticed from the statement of Sh. Nirmal Kumar Kedia in his statement recorded u/s 132(1) during the survey proceedings on 20.11.2016 at his business premises in reply to Que. No. 8,9 &18 wherein he has admitted that he had purchased 3 bhiga 18 biswa land from Sh. Jai Singh Yadav at a consideration of Rs.8.10 crores ( Rs.3.10 crores by cheque and Rs.5.00 crore in cash as “On Money” to Sh. Jai Singh Yadav. The AO reproduced the relevant part of statement at page 7 of the assessment order. The AO stated that subsequently statements of Sh. Jai Singh Yadav were recorded during search vide page 7 of the assessment order wherein the assessee has not accepted of receiving any on money from Sh. Nirmal Kedia. He has stated that assessee had not paid any capital gain tax on sale of 3 bhiga 18 biswa land for which he had received total consideration of Rs.8.10 crore (including on money of Rs.5 crores). The AO has issued the Show cause notice to the assessee for the Long Term Capital Gain addition on the sale of land for Rs.8.10 crores. In response thereto, the assessee filed the following reply placed at PB 73 also vide page No. 8 of the assessment order.

“The assessee has sold agriculture land at Village Badarama, Jaipur (Khasra No.15) to KediaRealestate LLP. Total area of agriculture land sold was 3 Bigha 18 Biswa and total consideration was Rs. 3,10,00,000/-. The assessee had 1/2 share in the above property. The transaction had been duly disclosed in the ITR filed by the assessee. The copy of Sale deed has already been seized by department during search proceedings (Exhibit -2-Page Nos. 59-79).

The above land sold was being used for agriculture purposes in the immediately preceding 2 years (evident from the copy of Girdawari OF Khasra No. 15 attached) and hence the assessee was eligible for exemption u/s 54B subject to purchase of agriculture land and other terms of Section 54B. The assessee complied with provisions of Section 54B and invested amount of Rs. 22,98,700/-in purchase of agriculture land and deposited balance amount of Rs. 1,33,00,000/- in capital gain scheme FDR (2 FDRs of 80 lakh & 53 lakh) (for buying agriculture land in future) and thus gain from sale of agriculture land was totally exempted from tax and no capital gain tax was payable on sale of agriculture land.

Further, the assessee stated that he had not received any ‘on money’ on the said sale of agriculture land. No addition can be made merely on the basis of statements of some person without documents substantiating the said transaction/income. Further assessee also seeks copy of relied upon documents in respect of said transaction. Assessee should also be given an opportunity to cross examine Mr. NirmalKedia and any other person who claims to have paid amount exceeding the transaction amount as per purchase deed. Assessee has not surrendered any undisclosed income on this account. Thus no addition can be made in income of assessee on this ground.”

However, the AO has not accepted the request of the assessee stating therein that request of assessee for cross examination is not acceptable as the right of cross examination is not an absolute right. The AO further stated that the agriculture land is not exempt from the capital gain because the land is situated within the municipal limit and purchaser Sh. Nirmal Kedia is authorized person of M/s Kedia Real Estate LLP, has confirmed in his statement that Rs.5,00,00,000/- was paid to Sh. Jai Singh Yadav against the above land. The AO stated that the total value of the property sold is Rs.8.10 Crores where assessee’s share was 1/2 i.e 4,05,00,000/-. Thus the AO has calculated the LTCG of Rs.2,44,93,451/- and made the addition vide page 11 of the assessment order.

5.3 In first appeal, the assessee submitted the detailed WS(PB57-6) praying therein that When the addition has been deleted in the hands of M/s Kedia Real Estate LLP no addition is required to be made here. It has also been submitted that Sh. Nirmnal Kedia has retracted from his statements and the ld. CIT(A) as well as the Honble ITAT has deleted the additions vide order in ACIT Central Circle-Jaipur v/s M/s Kedia Real Estate LLP in ITA No. 127 & 289/Jp/2019 dt.03.06.219, the copy of which is also placed on record. Considering the above facts and circumstances of the case, the ld. CIT(A) deleted the additions at pages 20 to 21 of his order.

5.4 Against the order of the ld. CIT(A) as to deletion of addition, the revenue is in appeal before us.

5.5 During the course of hearing, the ld. DR supported the order of the AO. and stated that the addition was made on the basis of statement of Sh. Nirmal Kedia who purchased the land from assessee and paid the On-Money to the assessee and statement has been given u/s 132(4).

5.6 On the other hand, the AR of the assessee has submitted following written submissions:

1. At the very outset we strongly rely upon on the order of the ld. CIT(A) on this addition. The ld. CIT(A) has deleted the addition by observing as under:

“ the ld. AO has made the addition merely on the basis of statement of Sh. NirmalKedia which ahs been subsequently retracted. It is observed that during the course of search/survey proceedings, no document found to prove the payment of on money by Sh. NirmalKedia to the appellant or his brother Shri Gopal lal Yadav for purchase of alleged agriculture land. In fact no corroborative or incriminating documents were found or seized with reference to the purchases/sale of aforesaid land to justify the addition. It is settled principal of law that statement alone cannot be treated as incriminating material for justifying the addition made in the assessment framed u/s 153A/143(3) of the act without any corroborative evidence brought on record. Further I have perused the order of Honble ITAT Jaipur Bench in ITA No. 289/Jp/2019 in case of ACIT Central Circle-3 Jaipur v/s M/s Kedia Real Estate LLP wherein the addition of Rs.5.00 Crores has been deleted in the hands M/s Kedia Real Estate LLP by stating as under.

……But in the case of the assessee, the surrender is not relatable to any material. In the case of assessee no any agreement, receipt, material was found to corroborate the surrender made in survey. Neither such material was found from the possession of assessee group nor from the possession of Shri Jai Singh Yadav group where the search was taken place on the same day.

Further, the surrender was obtained under duress, coercion, and in the atmosphere of fear. Further, in view of several discrepancies pointed out by the assessee in recording of the statement, the recording of statement is against the principle of natural justice vitiated in law and no cognizance of these statements should be taken.

54. Furthermore, the detailed finding recorded by the ld. CIT(A) in this regard, has not been controverted by the ld. DR by brining any positive material on record. Considering the judicial pronouncements relied on by the ldCIT(A) vis a vis quoted by the ld AR and ld DR during the course of hearing before us in the context of factual matrix of the case, we do not find any reason to interfere in the finding so recorded by the ld CIT(A) resulting into deletion of addition of Rs. 5.00 crores. Hence, this ground of the revenue’s appeal is dismissed.

In view of the categorical finding of the Honble ITAT Jaipur deleting the aforesaid addition of Rs.5.00 crore in the name of M/s Kedia Real Estate LLP, ther remain no grounds of treating the alleged on money of Rs.5.00 crore to have been received by the appellant. Further, the appellant has contended that the said transaction of sale of land, excluding the alleged on-money component duly disclosed by him in his ITR and exemption was claimed u/s 54B. On perusal of the assessment order it is observed that the AO has allowed the claim of exemption u/s 54B of the Act. And has thereafter worked out the capital gain at Rs.2,44,93,451/-. In view of the above findings, the AO is directed to verify the claim of the appellant and work out the long term capital gain in respect of the alleged property by reducing the on-money component of Rs.5.00 crores. “

2. Directly Covered matter: It is also submitted that now the issue is directly covered by the decision of this Honble ITAT. Because under the same facts and circumstances and under in the same search and the same addition has been deleted on account of On Money given by the NirmalKedia to the assessee vide order in In the case of ACIT Central Circle-3 Jaipur v/s M/s Kedia Real Estate LLP in ITA No. 127 & 289/Jp/2019 dt.03.06.219 copy is enclosed.

3. Further during the course of assessment proceedings we have submitted as under:

“The assessee has sold agriculture land at Village Badarama, Jaipur (Khasra No. 15) to KediaRealestate LLP. Total area of agriculture land sold was 3 Bigha 18 Biswa and total consideration was Rs. 3,10,00,000/-. The assessee had 1/2 share in the above property. The transaction had been duly disclosed in the ITR filed by the assessee. The copy of Sale deed has already been seized by department during search proceedings (Exhibit -2-Page Nos. 59-79).

The above land sold was being used for agriculture purposes in the immediately preceding 2 years (evident from the copy of Girdawari OF Khasra No. 15 attached) and hence the assessee was eligible for exemption u/s 54B subject to purchase of agriculture land and other terms of Section 54B. The assessee complied with provisions of Section 54B and invested amount of Rs. 2298700/-in purchase of agriculture land and deposited balance amount of Rs. 1,33,00,000/- in capital gain scheme FDR (2 FDRs of 80 lakh & 53 lakh)(for buying agriculture land in future)and thus gain from sale of agriculture land was totally exempted from tax and no capital gain tax was payable on sale of agriculture land.

Further, the assessee states that he had not received any ‘on money’ on the said sale of agriculture land. No addition can be made merely on the basis of statements of some person without documents substantiating the said transaction/income. Furtherassessee also seeks copy of relied upon documents in respect of said transaction.

Assessee should also be given an opportunity to cross examine Mr. Nirmal Kedia and any other person who claims to have paid amount exceeding the transaction amount as per purchase deed. Assessee has not surrendered any undisclosed income on this account.

Thus no addition can be made in income of assessee on this ground.

Further submission vide letter dated 05/11/2018:

Receipt of ‘On money’ of Rs. 5 Crore from Mr. Nirmal Kumar Kedia on sale of agriculture land.

The assessee reiterates his submission that he had not received any on-money from Nirmal Kumar Kedia in transaction of sale of agriculture land to M/s kedia Real Estate LLP. As per the statement of Nirmal Kumar Kedia he had given 1 post datedcheque as security for payment of Rs. 5 crore. No normal person will leave Rs. 5 crore on security of a post datedcheque. The statement of Nirmal Kumar Kedia is misleading and seems to have been made with some other motive. No other document except his statement has been made available to substantiate the alleged ‘On money’ receipt..

The assessee also submits that had he received such a huge amount, then it must have been reflected either as unexplained deposits in banks or some other unexplained investments, but no such instances are there. It is to be noted that not a single document seized from his premises indicates that any on-money was received from Nirmal Kumar Kedia. At the time of search also cash amounting to Rs. 1003350/- only had been found at the premises and for which suitable explanation has already been given.

It is also a well settled legal position that in absence of any corroborative incriminating documents, no addition can be made on the basis of statements of a third person. The assessee again seeks cross examination of Mr. Nirmal Kumar Kedia and request for copy of relied upon documents in addition to the statement of Mr. Kedia.”

However the ld. AO neither provide any opportunity of cross examination not any material. And made the addition blindly.

4. No incriminating documents and material found in search: Further during the course of search at the premises of assessee no documents or incriminating material was found which could establish the receipt of alleged on-money from sale of agriculture land to Kedia Realestate LLP. Further as per information available to assessee, no incriminating document is said to have been found at the premises of Mr. Nirmal Kumar Kedia(partner of Kedia Real Estate LLP) to evidence the payment of on-money for purchase of agriculture land from the assessee and his brother. Thus no addition can be made kindly refer our submission para no 4 page 17-22 in GOA -1 of the assessee’s appeal as also here .

5. Statement has been retracted by the Nirmal Kedia: The addition in income of assessee has been made solely on the basis of search statement of Mr. Nirmal Kumar Kedia (partner Kedia Real Estate LLP) in his case not in the case of assessee, who has himself retracted from his search statements and has denied paying any on-money to assessee and his brother. As now the additions has also been deleted by the Honble ITAT as stated above.

6.The assessee had out rightly denied receiving any on-money on sale of agriculture land to Kedia Realestate LLP and also contended that had he received the on-money then it must have been reflected in some manner like deposit in bank or unexplained investment in some asset, but no such instances are there. Further logically speaking nobody will leave a huge amount of Rs. 5 crore on security of a post dated cheque. The alleged cheque of Rs. 5 crore has also not been found from any of the searched premises. The assessee had submitted letter dated 05/11/2018 in this regard, but it has not been referred in the assessment order.

The assessee had also requested twice for cross examination of Mr. Nirmal Kumar Kedia to bring out correct facts, but the learned AO did not give this opportunity to the assessee. Thus on addition can be made on the basis of third party statement without any evidence and cross examination.

On this plea kindly refer our ws in assessee;s appeal submission in Para No.1 page 5-11 as also here our submissions.

7.There is no case of non- payment of tax on sale of agriculture land to M/s Kedia Real Estate LLP. In fact the assessee had declared the sale transaction of Rs. 3.10 crorein his ITR and claimed exemption under section 54B and there is no evasion of tax.

8. Assessee is illiterate and does not understand the nitty gritty of taxation:

We would like to draw your attention towards the fact that assessee, in his statement recorded on 19/11/2016, stated that he is illiterate and that he cannot read the contents of statement (Answer to Q.No. 1). He has also stated that work of filing of ITR is done by his nephew ManojYadav(Answer to Q. No. 9). In answer to Q.No.31 & 32 he has stated that he has not shown transaction of sale of land to KediaRealestate and has not paid tax, while in fact the same was disclosed in his ITR but because he had claimed exemption under section 54B hence no tax was paid by him.

9. Addition if any was to be made u/s 153C not 143(3): Further it is submitted that the addition of Rs.2,44,93,451/- was made on the basis of statements of Nirmal Kedia recorded u/s 132(4) in whose case search was carried out u/s 132. Thus it is established that the material, if any, on the basis of which addition has been made was not found in the premises of assessee admittedly and thus neither action could be taken under section 153A nor any addition. The addition if any could have been made only after issuing notice under section 153C after recording the satisfaction by the AO of other search persons and making assessment there upon. The learned AO has not acquired any jurisdiction under section 153C and thus the addition of Rs.2,44,93,451/- (in both assessee are is illegal and should be deleted. This is without prejudice to assessee’s claim that the alleged addition was otherwise also illegal and liable to be deleted.

11.1. Further during the assessment proceedings, the assessee had requested for cross examination of Mr. Nirmal Kumar Kedia and any other person who had owned the payment of on-money to assessee, by way of written request as well as orally. But the ld. AO has neither given opportunity to cross examine nor she provided copy of paper slip. And on this aspect we have already submitted hereinabove.

11.2 The copy of statement of assessee recorded under section 132(4) were not given to assessee inspite of repeated oral reminders to ADIT(Inv) together with letters dated 11/01/2017 & 21/03/2017 . It was on 11/05/2017, that the assessee received copy of his statements from Central Circle-3. The assessee then found that there is alleged surrender of income being recorded in his statement taken on 19.11.2016.