Learn how the issuance of show cause notices for GST short payments operates under the CGST Act and Rules. Sections 73, 74, and Rule 142 are key provisions defining the process and requirements for demanding GST amounts that are short paid, not paid, erroneously refunded, or involve wrongly availed or utilized Input Tax Credit (ITC). The process is further elaborated with a comprehensive flowchart.

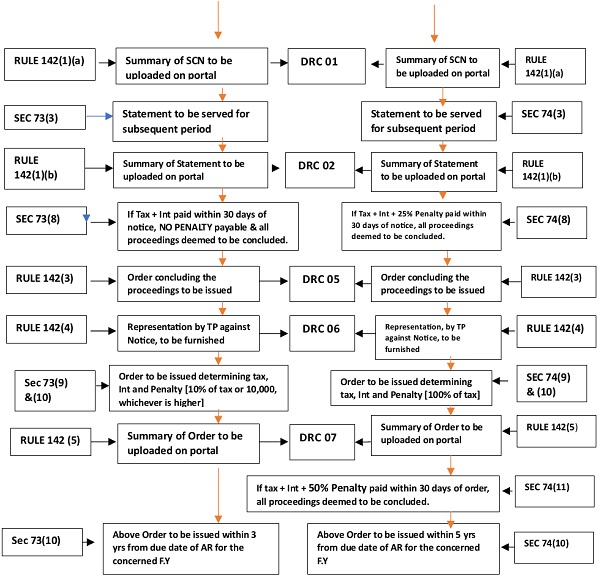

Under the CGST Act and Rules, Section 73, 74 and Rule 142 are the main relevant provisions, for the purpose of issuance of show cause notices, whereby, GST short paid or not paid or erroneously refunded or ITC wrongly availed or utilised, can be demanded. There are certain requirements and process to be followed thereon. The same is depicted in the flow chart given below-.

TO NOTE: In the flowchart, ‘SUPPRESSION’ cases refer to situations, wherein, GST is being demanded in terms of Sec 74(1) of CGST Act, by reason of fraud or any wilful mis statement or suppression of facts, to evade tax. ‘NON-SUPPRESSION’ cases refer to situations, wherein, GST is being demanded in terms of Sec 73(1) of CGST Act, for any other reasons.

The requirements/processes to be followed as depicted in the above flowchart is further elaborated hereunder-

1) COMMUNICATION -The discrepancy noticed i.r.o taxes and other dues needs to be first brought to the notice of the Tax payer (TP) in Part A of DRC -01A.

2) RESPONSE OF THE TP– If the TP accepts the objection and wishes to pay the entire/part of the tax amount, the same can be paid along with Interest and penalty by DRC-03 on the portal and the same can be intimated along with his submissions, if any, in part B of DRC-01A.

3) ACKNOWLEDGEMENT – The proper officer needs to acknowledge the payment in DRC 04.

4) NON-ISSUANCE OF SCN- In non-suppression cases, in terms of Sec 73(6), if the TP pays the pointed-out tax amount along with Interest, then no SCN shall be issued. However, in suppression cases, in terms of Sec 74(6) the TP also requires to pay penalty @15% of the tax amount for getting the benefit of waiver of SCN.

SELF ASSESSED TAX: However, in terms of Sec 73(11) i.e in non-suppression cases, if the tax payable is in respect of self assessed tax or is in respect of tax that has been collected but not paid to the Govt, to get the benefit of Sec 73(6) i.e non-issuance of SCN, Penalty @10% of the tax or Rs.10,000/-, whichever is higher, also needs to be paid.

i) Delay in filing GSTR 3B : When there is a delay in filing GSTR 3B, the tax payable and paid as declared in the said return becomes self assessed tax and consequently, Sec 73(11) gets attracted. However, Circular no. 76/50/2018-GST- Central Tax, dated 31.12.2018 has clarified vide sr. no.2 of the table in the said Circular that – ‘the provisions of Section 73(11) of the CGST Act can be invoked only when the provisions of section 73 are invoked (emphasis supplied- ie. when SCN is issued under the provisions of Sec 73(1)). The provisions of Section 73 of the CGST Act are generally not invoked in case of delayed filing of the return in FORM GSTR-3Bbecause tax along with applicable interest has already been paid but after the due date for payment of such tax. It is accordingly clarified that penalty under the provisions of Section 73(11) of the CGST Act is not payable in such cases. It is further clarified that since the tax has been paid late in contravention of the provisions of the CGST Act, a general penalty under Section 125 of the CGST Act may be imposed after following the due process of law’. In other words, an exception has been created vide the said Circular, whereby, no penalty is payable in terms of Section 73, in such self assessed tax cases, which arises due to late filing of GSTR 3B with the logic that no SCN is generally invoked in such cases as the tax and interest is already paid.

ii) Difference in GSTR 1 vis a vis GSTR 3B – Further, in terms of Sec 75(12), if any such self assessed tax remains unpaid, either wholly or partly, then recovery proceedings can be initiated under Sec 79. Explanation inserted to the said sub-section- 75(12), wef 1.1.2022, has widened the scope of ‘self assessed tax’ by including within its ambit ‘the tax payable in respect of details of outward supplies furnished under Section 37, but not included in the return furnished under Section 39’. In other words, the tax payable as declared in GSTR 1 also falls under the category of ‘self assessed tax’, which implies that recovery proceedings can be initiated under Sec 79 for recovery of the tax that has been declared in GSTR1 but not declared in GSTR 3B. However, vide Instruction no. 1/2022 dated 7.1.2022 issued by CBEC it has been directed that, before initiating any recovery proceedings in such cases, clarification first needs to be sought from the TP for the difference noticed in GSTR 1 and GSTR 3B and only if the TP fails to reply to the proper officer, or fails to explain the reasons for the difference/short payment, or fails to make the payment of such amount short paid or not paid, within the time prescribed in the communication or such further period as may be permitted by the proper officer, then the proceedings for recovery of the said amount as per provisions of section 79 may be initiated by the proper officer.

These aspects have been incorporated in Rule 88C which was inserted vide notification no. 26/2022-CT dated 26.12.2022, which entails intimation of such discrepancy noticed to the TP in Part A of Form GST DRC-01B. If the TP accepts the liability, whether partly or fully, the said tax liability is to be paid along with interest, through Form GST DRC 03. The details thereof alongwith reply is to be uploaded by the TP on the common portal in Part B of Form GST DRC -01B. In terms of sub-rule(3), if the explanation or reason furnished by such person is not found to be acceptable, the said amount shall be recoverable in accordance with the provision of Section 79. As per the recommendations of the 50th GST Council Meeting held in July 23, a new Rule 142B has been inserted vide notification no.38/2023 dated 4.8.23, which lays down further mechanism for recovery of the amount remaining unpaid. In respect of the amount that remains unpaid, an intimation needs to be given to the TP on the common portal in Form GST DRC -01D directing the person in default to pay the said amount, along with applicable interest, or, as the case may the amount of interest, within seven days of the date of the said intimation. On expiry of the 7 days’ time period, if the amount of tax or interest still remains unpaid, the officer shall proceed to recover in terms of Rules 143, 144, 145, 146, 147, 155, 156, 157 or rule 160 as applicable.

The wordings used in sub-rule (3) of Rule 88C raises a question as to whether it is simply the discretion of the officer to accept or not to accept the explanation, as, if not found acceptable, direct recovery action can be initiated. Let’s take an example- Hypothetically, let’s assume that the taxable value declared for the month of August 2023 in Table 4A of GSTR 1 is Rs.1 cr.. and the tax payable thereof @18% is shown as Rs.18 lacs. No other supply is shown for the said month. The factual position for the TP is that the actual taxable value of supply of services for the said month is of Rs.90 lacs and Rs.10 lacs pertains to ‘Pure services provided to a Municipal corporation’, which according to the TP is exempted vide sr. no. 3 of the Exemption notification no. 12/2017-CT (R) dated 28.6.2017, as amended. Thus, the actual tax payable, as per the TP, for the said month, works out to Rs.16.2 lacs. These facts are correctly depicted by the TP in table 3.1(a) and 3.1(c) of GSTR3B for the said month. Thus, the tax payable for the month of Aug 2023 as per GSTR 1 exceeds the tax payable as per GSTR3B by Rs.1.8 lacs. Now, if these facts are conveyed by the TP in Part B of GST DRC-01B and is not found acceptable to the proper officer as he feels that the TP is not entitled to exemption, the question is, can he directly initiate recovery proceedings in this case.

On a cohesive reading of the provisions of Sections-73, 74, 75; Rules 88C and 142B, it could be inferred that, where the tax payer has accepted the tax liability and has remained unpaid even after expiry of the notice period, then action can be initiated for recovery proceedings. However, my personal view is that, when the TP disputes the tax liability, the issue is no more of self assessed tax. At the most, it can be said to be wrongly termed as ‘self assessed tax’ in GSTR1 and rectified in GSTR 3B. The person is not in default. Moreover, in such case, the theory of ‘audi alteram partem’ [Meaning -let the other side be heard as well] will come into play and it needs to be heard by the appropriate authority, for which issuance of a proper show cause notice under the provisions of Section 73 becomes essential.

In a case before Kar HC [Writ Appeal no. 188 of 2020 (T-Res)- LC INFRA PROJECTS P LTD- ORDER DT. 3.3.2020], department had initiated proceedings under Sec 79 for recovery of interest under Sec 50 without issuance of SCN. It was contended by the dept. that as the tax was payable as per the self-assessment made by the assessee, it was not necessary to issue a show cause notice to the respondent-assessee as the demand was only as regards to payment of interest under Sub Section (1) of Section 50 of the GST Act. In the said case it was held that non-issuance of SCN for recovery of interest will be in breach of principles of natural justice and that before recovery of interest payable in accordance with Section 50 of the GST Act, a show Cause Notice is required to be issued to the assessee.

To conclude, it appears that in such cases of self-assessed tax and interest liability, if the same is disputed, then the same comes out of the colour of ‘self assessed tax’ and recourse needs to be taken to issuance of SCN under Section 73 of the GST Act to decide the issue. For lack of clarity, there are bound to be litigations in the matter, till the matter is clarified by way of issuance of a Circular or suitable amendments to the relevant provisions.

5) ISSUANCE OF SCN – SCN has to be issued and served to the TP for the amount short paid along with Interest and demanding penalty leviable under the provisions of Sec 73 for non-suppression cases and in suppression cases, SCN is to be issued under Section 74, demanding tax/ITC amount short paid with Interest and Penalty equivalent to the tax/ITC amount specified in the notice. A summary of the notice needs to be uploaded by the proper officer in DRC 01 on the portal.

The SCN can be served by any one of the methods prescribed under Sec 169 of the GST Act, which includes by way of making it available on the common portal, by way of e-mail to the regd. e-mail ID, by regd. post or by tendering it directly to the TP.

6) NOTICE FOR SUBSEQUENT PERIOD – For the subsequent periods, on the same issue, a statement containing details of the tax payable or ITC wrongly availed or utilised will suffice, in lieu of issuance of SCN, which may be served on the TP. A Summary thereof shall be uploaded on the portal in FORM GST DRC -02.

7) CONCLUSION OF PROCEEDINGS – In non-suppression cases, if within 30 days of issuance of notice, the TP pays the tax amount along with interest payable, No Penalty shall be payable and all proceedings iro the SCN shall be deemed to be concluded. In suppression cases, 25% Penalty also needs to be paid for conclusion of the proceedings. An Order concluding the proceedings need to be issued and uploaded by the proper officer on the portal in DRC 05.

8) SUBMISSIONS AGAINST THE NOTICE – Representation, if any, against the SCN is to be filed by the TP and needs to be uploaded on the portal in Form – DRC 06.

9) ISSUANCE OF ORDER (OIO) – After considering the representation of the TP, the proper officer shall issue an OIO determining the tax, interest and penalty. In non-suppression cases, penalty payable shall be equivalent to 10% of the tax or Rs.10,000/-, whichever is higher. In suppression cases, Penalty payable shall be equivalent to 100% of the tax payable. A summary of the order shall be uploaded on the portal in DRC 07.

It is to be pointed out that, though, Sec 74(11) specifies serving of the Order, incidentally, Sec 73 is silent on the aspect of serving of the Order. The same will have to be read with Section 169, inferring, thereby, that the Order needs to be served by one of the methods prescribed therein.

It is also to be pointed out that what amounts to communication of order, for the purpose of filing appeal under Section 107 has been given different interpretation by Courts. Whether, the date of uploading of Order on the portal or the date of serving of the order by any one of the methods prescribed for serving of order under Sec 169 is to be taken as the date of communication of Order for the purpose of Section 107, is under litigation and has been given different interpretation by Courts.

10) TIME LIMIT FOR OIO – In terms of Sec 73(10), in non-suppression case, the OIO shall be issued within 3 years from the due date for furnishing of Annual Return (AR) for the concerned tax period or within 3 years from date of erroneous refund. In suppression cases, in terms of Sec 74(10), the time limit will be 5 years.

In terms of Sec 73(2), SCN is to be issued atleast 3 months prior to the above said time limit of issuance of OIO. Whereas, in suppression cases, SCN is to be issued atleast 6 months prior to the issuance of OIO.

For cases, other than that to be issued for recovery of erroneous refund, the due dates for issuance of OIO for the F.Y starting from July 2017 and consequently the due dates for issuance of SCN has been tabulated as under-

| Financial Year | AR Due Date | OIO Due Date U/Sec 73 | OIO Due Date- U/Sec 74 | Notfn. extending due dt. U/Sec 168A | REVI SED OIO DUE DATE U/ SEC 73(10) | SCN DUE DATE U/ SEC 73 |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 |

| 2017-18 | 7.2.2020 (Maharashtra & few States.)

Notf. 6/20. Other States- 5.2.2020 |

6.2.2023

4.2.2023 |

6.2.2025

4.2.2025 |

9/2023 dt. 31.3.23 |

31.12.23 |

30.09.23 |

| 2018-19 | 31.12.20 (Notf. 80/20) | 30.12.2023 | 30.12.2025 | 9/2023 dt. 31.3.23 |

31.03.24 |

30.12.23 |

| 2019-20 | 31.3.21 (Notf 4/21) | 30.3.2024 | 30.3.2026 | 9/2023 dt. 31.3.23 |

30.06.24 |

29.03.24 |

| 2020-21 | 28.2.22 [Rule 80(1A)] | 27.2.2025 | 27.2.2027 | 26.11.24 | ||

| 2021-22 | 31.12.22 [Rule 80(1)] | 30.12.2025 | 30.12.2027 | 29.09.25 | ||

| 2022-23 | 31.12.23 [Rule 80(1)] | 30.12.2026 | 30.12.2028 | 29.09.26 |

The revised due dates for issuance of SCN, as per sr. no. 7 of the table may be noted, which is due to the revised due dates for issuance of OIO as per sr. no.6 of the table. In a case before the Kerala HC in the case of Pappachan Chakkiath vs. AC, North Paravur [WP(C) no. 816 of 2023, decided on 11.1.2023], the revised due date for issuance of SCN for F.Y. 2017-18 was challenged, when the due date for issuance of Order for 2017-18 was extended upto 30.9.23, according to which the due date for issuance of SCN became 29.6.2023. It was then held as under-

“When the time limit for issuance order under sub- section (10) of section 73 for the financial year 2017-18 has been extended upto 30-9-2023, the only interpretation that can be placed on the provisions of sub-section (2) of section 73 is that, the show cause notice can also be issued with reference to the date 30-9-2023 and not with reference to any other date.”

Thus, the due date for issuance of SCN under Section 73, for the Financial Years as shown in column no.1 will be as per the due dates specified in column no.7 of the above table, which will be in sync with the extended due date for issuance of order under Section 73(9).

11) NON ISSUANCE OF ORDER WITHIN TIME PRESCRIBED– Further, in terms of Sec 75(10) of the CGST Act, if the Order is not issued within three years as provided for in sub-section (10) of section 73 or within five years as provided for in sub-section (10) of section 74, then the adjudication proceedings shall be deemed to be concluded.

12) REDUCTION OF PENALTY– In suppression cases, if tax +Int+ penalty @50% of tax is paid within 30 days of the OIO, all proceedings i.r.o the said notice shall be deemed to be concluded.

13) RECTIFICATION OF OIO – In terms of Sec 161 of the CGST Act, if any error apparent on the face of record in the said OIO comes to the notice of the department or is brought to its notice within a period of 3 months of such OIO, the authority who has issued the OIO may rectify the OIO within a period of 6 months. The said time limit shall not apply in case of clerical or arithmetical error, arising from any accidental slip or omission.

The above also applies to SCN’s issued.

SOME RELATED ISSUES :

A) TAX AND OTHER DUES ARISING OUT OF SCRUTINY OF RETURNS – If the discrepancy iro taxes and other dues is noticed during Scrutiny of returns, then in terms of Sec 61 read with Rule 99 of CGST Rules, the issuance of DRC-01 shall be preceded by issuance of notice to the TP in Form GST ASMT-10, informing him of such discrepancy. Explanation may be furnished by the TP in Form GST ASMT-11. IF the explanation is found acceptable, then the TP may be informed accordingly in Form GST ASMT-12.

If the explanation is not found acceptable, then the procedure as above, by way of initiating the process of issuance of SCN and DRC 01 may be followed. In this context, reference may be had to Madras HC decision dated 27.9.2022 [WP(MD) NO. 22642 OF 2022 & WMP(MD)NOS. 16803 AND 16804 OF 2022] in the case of Vadivel Pyrotech P Ltd. which has inferred as such and wherein ASMT-10 having not been issued, for the subject matter, before issuance of DRC 01 was held to vitiate the entire proceedings and thereby the Order issued in DRC 07 was set aside and an opportunity was granted to the Department to issue Form ASMT-10 in the matter.

B) NON ISSUANCE OF INTIMATION UNDER DRC 01A – From the process flow chart for issuance of show cause notice, it could be seen that it is essential that the TP need to be first communicated the discrepancy noticed, in part A of DRC 01A, failing which there is a possibility that the SCN may be declared invalid and be set aside. However, in an interesting case [ELESH AGRAWAL VS. UOI- ALLAHABAD HC – WRIT TAX NO.753 OF 2023], wherein, the disputed tax amount was about Rs.10.5 cr and though DRC 01 was issued, DRC 01 A was not issued in the said case. It was contended by the revenue that the TP has not admitted any fact allegations levelled against him and therefore the requirement of preliminary notice has largely been reduced to a formality. Allahabad HC in the said case accepted the line of argument and did not set aside the notice and the TP was directed to reply to the notice within 1 month on the ground that the objection appears to be hyper technical and not real.

It may be noted that non-issuance of DRC 01A would result in depriving the TP the opportunity to avail the benefit of Sec 74(5) and 74(6), whereby, by payment of tax +Int + 15% penalty, they could have got the benefit of waiver of issuance of SCN and DRC 01. In the said case, athe Hon’ble High Court could have atleast given the opportunity to the TP to avail the benefit of Sec 74(5) and 74(6) by giving them one month’s time to pay the dues accordingly. Probably, similar matter may be dealt with differently, if it’s raked up again in a different court/bench.

C) NON-SERVING OF SCN – On the other hand, just issuance of summary of SCN in form GST DRC 01 without serving of proper SCN on the TP has been held to be legally unsustainable. In the case of NKAS SERVICES P LTD, Jharkhand HC has held that- ‘A summary of show-cause notice as issued in Form GST DRC-01 in terms of Rule 142(1) of the JGST Rules, 2017 cannot substitute the requirement of a proper show-cause notice’. Similar decision has been given by the same Court in the case of Shree Ram Agrotech [WP(T) no. 163 of 2023], wherein the DRC 07 issued in the said case was set aside and liberty granted to the department to issue fresh SCN.

To conclude, it is of importance for the departmental officers to follow the process flow prescribed and as detailed hereinabove, under the provisions of Sec 73, 74 of CGST Act read with Rule 142 of CGST Rules, in its letter and spirit and also adhere to the time limit for issuance of SCN and Order, lest it may be held to vitiate the entire proceedings initiated under Sec 73/74. The tax payers, on the other hand, need to ensure that the departmental officers have followed the process flow as laid down in the flow chart and as detailed hereinabove and if any deviation is noticed, the same can be used to claim that the deviation has vitiated the proceedings prescribed under Section 73 or 74, as the case may be.

The due dates mentioned for issue of order under sec 73/74 are wrong

Latest Updates are not complied.

Excellent