SOP for extension of time limit to apply for revocation of cancellation of registration:

CBIC has issued Notification No. 15 /2021 – Central Tax dated 18th May 2021 and Circular No. 148/04/2021-GST dated 18th May, 2021 specifying Standard Operating Procedure (SOP) for implementation of the provision of extension of time limit to apply for revocation of cancellation of registration u/s 30 of the CGST Act, 2017 and rule 23 of the CGST Rules, 2017.

The said change along detailed procedure and flowchart has been discussed herein below –

A. Revocation of Cancellation of Registration – Amendment in Rule 23 of CGST Rules, 2017 –

As per Rule 23 of the CGST Rules, 2017 – A registered person, whose registration is cancelled by the proper officer on his own motion, may submit an application for revocation of cancellation of registration, within a period of thirty days from the date of the service of the order of cancellation of registration at the common portal, or within such time period as extended by the Additional Commissioner or the Joint Commissioner or the Commissioner, as the case may be, in exercise of the powers provided under the proviso to sub-section (1) of section 30. (italics portion Inserted by CGST (4th Amendment) Rules, 2021)

B. Standard Operating Procedure for implementation of the provision of extension of time limit to apply for revocation of cancellation of registration–

i. In the Finance Act, 2020, section 30 of the CGST Act, 2017 was amended (notified wef 1stJan, 2021 vide notification No. 92/2020- Central Tax, dated 22nd December 2020). The amended provision provides for extension of time limit for applying for revocation of cancellation of registration.

ii. Application may be made to the Additional or Joint Commissioner, as the case may be, for a period not exceeding thirty days.

iii. The Commissioner, for a further period not exceeding thirty days, beyond the period specified above

c. Procedure for revocation of cancellation –

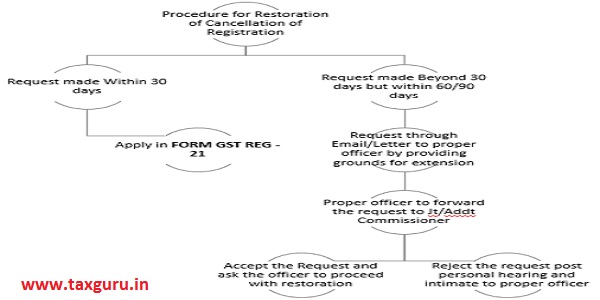

i. If revocation is applied within 30 days –It has been provided in section 30 of the CGST Act, any registered person, whose registration is cancelled, may apply in FORM GST REG-21, for revocation of cancellation of registration within 30 days from the date of service of the cancellation order.

ii. If revocation is applied beyond 30 days but within 60 days – In case the registered person applies for revocation of cancellation beyond 30 days, but within 60 days from the date of service of the cancellation order, the following procedure is specified for handling such cases:

Flowchart of procedure for restoration of cancellation of Registration –

a. The person may request, through letter or e-mail, for extension of time limit to apply for revocation of cancellation of registration to the proper officer by providing the grounds on which such extension is sought.

b. The proper officer shall forward the request to the jurisdictional Joint/Additional Commissioner for decision on the request for extension of time limit.

c. The Joint/Additional Commissioner may extend the time limit to apply for revocation of cancellation of registration. In case the request is accepted, the extension of the time limit shall be communicated to the proper officer.

d. In case the concerned Joint/Additional Commissioner, is not satisfied with the grounds on which such extension is sought, an opportunity of personal hearing may be granted to the person before taking decision in the matter.

e. In case of rejection of the request for the extension of time limit, the grounds for such rejection may be communicated to the person concerned, through the proper officer.

f. On receipt of the decision of the Joint/Additional Commissioner, the proper officer shall process the application for revocation of cancellation of registration according to the law and procedure laid down in this regard

g. Procedure similar to that explained above, shall be followed mutatis-mutandis in case a person applies for revocation of cancellation of registration beyond a period of 60 daysfrom the date of service of the order of cancellation of registration but within 90 days of such date.

The circular shall cease to have effect once the independent functionality for extension of time limit for applying in FORM GST REG-21 is developed on the GSTN portal

*****

You can contact us at: Email: Rohit@taxmarvel.com

Disclaimer: The content of this document is for general information purpose only. TaxMarvel shall not accept any liability for any decision taken based on the advice. You should carefully study the situation before taking any decision.

Author Bio

i like your suggession