Introduction

E-commerce does not need any introduction to start with. However, the unique features of e-commerce transactions have always made it a bit complex to levy tax. In e-commerce transactions, the supplier of goods and services may or may not have a permanent establishment or an office in a taxable territory in which he supplies goods and services. Finance Act 2020 also brought some changes in the taxability of e-commerce transactions from income tax perspective. However, in this article, we have discussed the impact of GST these e-commerce transactions.

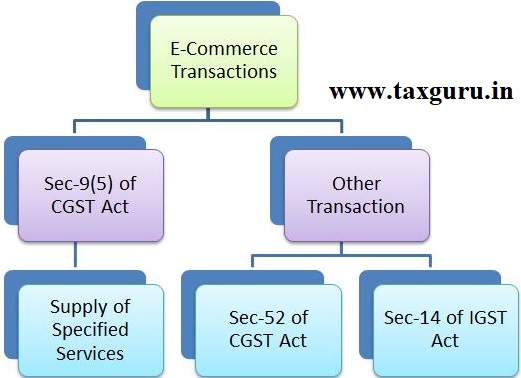

All the e-commerce transactions can be divided into three categories under GST regime. A transaction may fall into sec-9(5) of the CGST Act or Sec-52 of CGST Act or Sec-14 of IGST Act 2017. All the three categories are mutually exclusive that means a transaction may fall in only one of the above category only.

Transactions Falling u/s 9(5) of CGST Act 2017

Section 9(5) of the CGST Act is a charging section along with other sub sections of section 9. Sec-9(5) has been reiterated here as follows:

The Government may, on the recommendations of the Council, by notification, specify categories of services the tax on intra-State supplies of which shall be paid by the electronic commerce operator if such services are supplied through it, and all the provisions of this Act shall apply to such electronic commerce operator as if he is the supplier liable for paying the tax in relation to the supply of such services:

Provided that where an electronic commerce operator does not have a physical presence in the taxable territory, any person representing such electronic commerce operator for any purpose in the taxable territory shall be liable to pay tax:

Provided further that where an electronic commerce operator does not have a physical presence in the taxable territory and also he does not have a representative in the said territory, such electronic commerce operator shall appoint a person in the taxable territory for the purpose of paying tax and such person shall be liable to pay tax.

As per the above provisions, the Central Govt is empowered to notify services, tax on which shall be payable by the e-commerce operator (ECO) if such services are supplied through it. Unlike the reverse charge mechanism where recipient is liable only for payment of tax, an ECO is treated as actual supplier of services falling u/s 9(5). The ECO shall be liable to pay tax, report supplies, file return and comply with all the laws which are, otherwise, to be complied by the supplier of services.

In exercise of the powers conferred u/s 9(5) of the CGST Act, the Central Government has notified, vide NN 17/2017 (Rate) and 23/2017 (Rate), the following categories of services, the tax on intra-State supplies shall be paid by the electronic commerce operator –

- Services by way of transportation of passengers by a radio-taxi, motorcab, maxicab and motor cycle;

- Services by way of providing accommodation in hotels, inns, guest houses, clubs, campsites or other commercial places meant for residential or lodging purposes, except where supplier is liable for registration u/s 22 of the CGST Act;

- Services by way of house-keeping, such as plumbing, carpentering etc., except where supplier is liable for registration u/s 22 of the CGST Act.

Transactions Falling u/s 52 of CGST Act 2017

Section 52 of the CGST Act is not a charging section but is a method of collecting taxes. Section 52 lays down that the ECO shall collect and deposit a tax @1% (i.e. 0.5%+0.5%) from the value of taxable supplies made through it by other suppliers and the consideration is also collected by the ECO from the customer. Here it is worth noting that where an ECO supplies its own goods or services through its website/portal then the provisions of sec-52 are not at all applicable.

Section 52(1) states:

Notwithstanding anything to the contrary contained in this Act, every electronic commerce operator (hereafter in this section referred to as the “operator”), not being an agent, shall collect an amount calculated at such rate not exceeding one per cent., as may be notified by the Government on the recommendations of the Council, of the net value of taxable supplies made through it by other suppliers where the consideration with respect to such supplies is to be collected by the operator.

Explanation.––For the purposes of this sub-section, the expression “net value of taxable supplies” shall mean the aggregate value of taxable supplies of goods or services or both, other than services notified under sub-section (5) of section 9, made during any month by all registered persons through the operator reduced by the aggregate value of taxable supplies returned to the suppliers during the said month.

Explanation to the sub-section (1) excludes the value of supplies notified u/s 9(5) from the net value of taxable supplies on which tax is to be collected.

If a comparison is to be made of sec-52 vis-a-vis sec-9(5) of the CGST Act 2017: –

- Both the sections are mutually exclusive of each other.

- Sec-9(5) is a charging section whereas sec-52 is a method of collecting tax charged by other section.

- Sec-9(5) treats the ECO as actual supplier of services whereas sec-52 does not makes any such assumptions

An ECO is liable to deposit the tax collected u/s 52 to the Govt latest by 10th day of next month and file GSTR-8 by that that failing which shall attract interest u/s 50. The amount thus collected and deposited shall be reflected in the supplier’s cash ledger on the common portal.

Transactions Falling u/s 14 of IGST Act 2017

Since GST is a consumption based tax therefore any supplies which are consumed in India i.e. the taxable territory should be liable to tax. However, consider an e-commerce transaction where the ECO is not situated in India or does not have any physical presence in India and still supplies services to non-business persons in India. We know where service provider is outside India and service recipient is in India, tax is discharged by the recipient under RCM. Since a non-business person is not liable for registration, would he be required to take registration for life long to discharge the RCM liability on such services? The answer is NO. In such cases, the ECO has been made liable for registration and payment of tax via section-14 of IGST Act.

Section-14(1) of IGST Act lays down: On supply of online information and database access or retrieval services by any person located in a non-taxable territory and received by a non-taxable online recipient, the supplier of services located in a non-taxable territory shall be the person liable for paying integrated tax on such supply of service.

Where Online information and database access or retrieval (OIDAR) services means services whose delivery is mediated by information technology over the internet or an electronic network and the nature of which renders their supply essentially automated and involving minimal human intervention and impossible to ensure in the absence of information technology and includes electronic services such as,––

- Advertising on the internet;

- Providing cloud services;

- Provision of e-books, movie, music, software and other intangibles through telecommunication networks or internet;

- Providing data or information, retrievable or otherwise, to any person in electronic form through a computer network;

- Online supplies of digital content (movies, television shows, music and the like);

- Digital data storage; and

- Online gaming;

And non-taxable online recipient means any Government, local authority, governmental authority, an individual or any other person not registered and receiving online information and database access or retrieval services in relation to any purpose other than commerce, industry or any other business or profession, located in taxable territory.

Also, if such services are provided to a person who is located outside India then such services are exempt vide exemption notification.

Remark by Author

From the above discussion we have tried to ease down the complexity of the e-commerce transactions by providing a gross view of the taxability of these transactions. All the above analysis provided above is solely based on the understanding and analysis of the author, another person may have a different point of view which is always welcome.

Hi Mr Pawan Kumar

We have a company from Malaysia and they want to setup wholly owned subsidiary company in India.

They will sale general goods through online portal (which is managed by Holding company) and Subsidiary company will act as intermediary to collect revenue from clients in India, they will deliver the goods in India through bluedart or DHFL etc.

Can you guide what will be GST obligations on subsidiary and holding company

Thanks,

Hi Mr Vivek,

We have a company from Malaysia and they want to setup wholly owned subsidiary company in India.

They will sale general goods through online portal (which is managed by Holding company) and Subsidiary company will act as intermediary to collect revenue from clients in India, they will deliver the goods in India through bluedart or DHFL etc.

Can you guide what will be GST obligations on subsidiary and holding company

Thanks,