SCHEME OF PRESENTATION

> Present System of Filing – GSTR 1 & GSTR 3B

> Simplified New Return System

√ Key Features of Monthly Return

√ Key Features of Quarterly Return

√ Brief Overview

Transition to New Return System

Download PPT on Latest Update in GST including New Return System

PRESENT SYSTEM OF FILING

GSTR – 1 & GSTR 3B

SIMPLIFIED NEW RETURN SYSTEM

BRIEF OVERVIEW

![]()

SIMPLIFIED NEW RETURN SYSTEM – AN OVERVIEW

SIMPLIFIED NEW RETURN SYSTEM

SIMPLIFIED NEW RETURN SYSTEM – AN OVERVIEW

A look at the options available for the taxpayers

| Aggregate Turnover | New Return Type / Options available | FORM Name & Filing Frequency | Determination of Turnover |

| More than₹ 5.0 Crore | FORM GST RET – 1 | NORMAL – Monthly | Newly Registered Dealer: For newly registered taxpayer turnover will be decided on the basis of Self Declaration made by them on estimated turnover.

Other than above : For already registered Taxpayer it will be decided on the basis of Last year’s Turnover |

| Less than ₹ 5.0 Crore | (1). FORM GST RET – 1 | NORMAL – Monthly | |

| (2). FORM GST RET – 1 | NORMAL – Quarterly | ||

| (3). FORM GST RET – 2 | SAHAJ – Quarterly | ||

| (4). FORM GST RET – 3 | SUGAM – Quarterly |

BRIEF OVERVIEW OF NEW RETURNS SOME OTHER KEY ASPECTS

SIMPLIFIED NEW RETURN SYSTEM

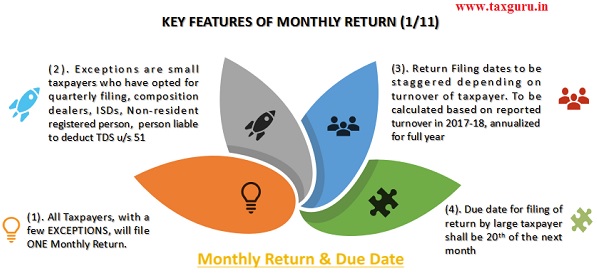

KEY FEATURES OF MONTHLY RETURN

JULY 2017- JUNE 2019

I. Total GST Registrations has doubled up to 1.22 Cr.

II. Total number of GST Returns filed – 28 Cr.

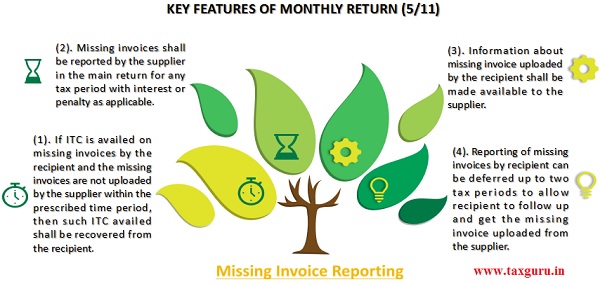

KEY FEATURES OF MONTHLY RETURN (4/11)

Invoice Uploaded but Return not Filed

↓

If the return is not filed by the supplier after uploading the invoices, it shall be treated as self-admitted liability by the supplier and recovery proceedings shall be initiated against the said supplier after allowing a reasonable time to file the return and pay tax.

KEY FEATURES OF MONTHLY RETURN (11/11)

Other Miscellaneous Features

> Tax amount shall be computed by system based on taxable value and tax rate. The tax amount so computed will not be editable except in case of credit/ debit notes issued.

> Reverse charge supplies will be reported only by recipient and not by supplier. Such supplies shall be reported GSTIN wise (wherever applicable) and net of credit and debit notes.

> All supplies specified in Schedule III of CGST Act shall be reported under ‘No supply’ in the main return. It will include high sea sale and bonded warehouse sale also.

> Place of supply shall have to be reported mandatorily for all supplies.

> Supplies made through e-commerce portal maintained by other operators shall be reported at consolidated level.

TRANSITION

![]()

CBIC Mitra Helpdesk

Toll Free No. 1800-1200-232

Cbecmitra.helpdesk@icegate.gov.in

Cbec-gst.gov.in>HELP>SELF SERVICE

E – Invoicing :

> The Council also decided to introduce electronic invoicing system in a phase-wise manner for B2B transactions.

> E-invoicing is a rapidly expanding technology which would help taxpayers in backward integration and automation of tax relevant processes.

> It would also help tax authorities in combating the menace of tax evasion.

> The Phase 1 is proposed to be voluntary and it shall be rolled out from Jan 2020

TRADE FACILITATION MEASURES

GRIEVANCE REDRESSAL PORTAL FOR GST

Grievance Redressal portal for lodging complaints by taxpayers and other stakeholders. Complaints with respect to portal can be lodged here. Facility to uploads screenshots of pages – Self Help Grievance Portal.

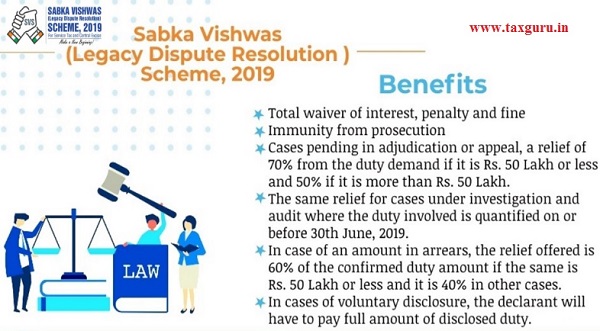

SABKA VISHWAS (LEGACY DISPUTE RESOLUTION) SCHEME, 2019

Scheme Open from 01.09.2019 to 31.12.2019

Scheme Open from 01.09.2019 to 31.12.2019

Compiled by-

S.K. Rahman

COMMISSIONER (IT & COMPLIANCE VERIFICATION)

Directorate General of Systems,

Central Board of Indirect Taxes and Customs

011-26113619, 9490957533

rahman.shaik@icegate.gov.in

Download PPT on Latest Update in GST including New Return System