Understand the nuances of Input Service Distribution (ISD) vs Cross Charge in GST. Learn about the tax implications, controversies, and recent developments. Stay informed for effective compliance.

The concept of Input Service Distributor (ISD) under GST has been carried forward from the erstwhile Service tax regime. ISD has been defined under Section 2(61) of the CGST Act, 2017. It is an office of supplier which has received input services, and the said input services are attributable to various branches of a company, consequent to which the ITC on such input services are to be distributed amongst all such branches deriving benefit out of the said services. The intent of the ISD mechanism is to pass on the credit to the respective states to which the expense or the input service is attributable. The role of an ISD is limited to availing and distributing credit to its various other establishments or units for utilisation. The entire ISD mechanism is only for distribution of credit on input services and not on inputs or capital goods.

Cross charge is not defined under the GST Laws. It is a colloquially derived term in usage. It is a mere supply from one registered person to another where such entities have a common PAN. Inter-branch supply of goods (stock transfers) & supply of services by one branch of a company to another would qualify for cross charge vide Entry 2 of Schedule I read with Section 25(4) of the CGST Act, 2017. For example, a company has procured a contract for provision of consultancy services, and Tamil Nadu office has entered into a contract for the same. During the course of provision of service, if Karnataka office provides some portion of the services to the end customer, this will tantamount to cross billing amongst different GSTINs of the same company. Tamil Nadu office will invoice the end customer for the full contract value and Karnataka office will invoice Tamil Nadu office for the part of the services provided by it. The same can be regarded as a deemed outward supply.

There is a huge controversy which revolves around the question that whenever a particular expense is incurred by the Head office and the benefit of the same is attributable to other units also, then would the same have to be cross charged or the ITC on the same be distributed through ISD. Often the matter is raised by the department in audit & scrutiny proceedings of persons having pan India operations with registrations in multiple states.

This article is an attempt to throw some light on the same.

For externally procured services like Auditing services, the company can avail ITC on the same and distribute it to all branches since such services are availed for the company as a whole and thus the benefit of the same is derived by all the branches.

The Head office may provide internal services to its branches like, HR, admin support, payroll processing, legal support, IT systems, accounting etc the benefit of which is obtained by all branches. Whether the same constitutes a supply or not is a primary question. If it is construed to be a supply, the next challenge is the valuation of such services to be apportioned to the branches.

ISD does not create charge, there is no outward supply, it is only distribution of ITC to the relevant units / branches. Cross charge is an outward supply and GST is applicable on the same.

Cross charge can be done from any existing registration and there is no requirement for any separate registration unlike ISD.

In the case of Cummins India Ltd, the Authority for Advance Ruling held that availment of ITC on common input supplies on behalf of other units registered as distinct persons and further allocation of the cost incurred for the same to such other units qualifies as a supply and is exigible to GST. Further, the authority held that where GST is levied on such internal apportionments and ITC thereof is availed by the recipient unit, the HO is still required to obtain mandatory registration as an ISD in terms of Section 24.

The ruling has created more confusions in the industry. Compulsory registration as an ISD is required only if a person wants to distribute ITC by way of ISD mechanism.

Further, once the common allocation of expenses is treated as supply and leviable to GST, there legally seems to be no requirement for registration of ISD. If the applicant takes registration under ISD and distributes credit there under, there would be no requirement of cross charge. Both are mutually exclusive. Cross charging a particular expense, and registering as ISD does not categorically seem to be the proposition.

In the case of Columbia Asia Hospitals Pvt Ltd, the Appellate Authority for Advance Ruling observed that the question that emerges in this appeal is whether the Head office is providing a service to its other distinct units by way of carrying out activities such as accounting, administrative work, etc., with the use of the services of the personnel working in the Head office, the outcome of which, benefits all the other units and whether such activity is to be treated as a taxable supply in terms of the Entry 2 of Schedule I read with Section 7 of the CGST Act. The AAAR clearly answered the question in the affirmative. The cost of the employees working in the Head Office is an integral part of the cost of the services rendered by the HO to its other distinct units. The services of the employees at the HO in so far as they are benefiting the other registered units of the appellant, will not be termed as ’employee-employer relationship’ and will therefore not fall within the purview of Entry 1 of Schedule III.

This ruling has by and large far-reaching consequences.

The same matter was highlighted before the GST Council for discussion as agenda item 6(iv) in its 35th GST Council meeting dated 21st June 2019. A draft circular was discussed which was never issued. The relevant extracts of the same is attached herewith for reference.

As per the minutes & draft circular the intent of the government is clear to tax such support activities internally generated and the cross charge of the same needs to be done.

The aforesaid draft circular was never published or issued for clarification and it remained as draft, hence the clarification given therein has no validity as such, but it shows the intent of the Government towards such support activities internally generated.

It is possible to take a stand that such internal activities carried out by employees of HO for its BOs or vice-versa may not be considered as supply as per the GST provisions as the employees be it under HO or BO are considered as employees of the company as a whole and Schedule III specifically provides that the services by an employee to the employer in the course of or in relation to his employment as Activities or transactions which shall neither be treated as a supply of goods nor a supply of services.

In general parlance it means an organisation or a person which employs people and an individual employed by an employer, as such, shall be considered as an employee of an entity as a whole. The branch office shall also be considered as an employer and any activity carried out by an employee posted at head office on the directions of the branch office will also be considered as carried out in the course of or on relation to his employment and hence the support activities carried out by the employees posted at HO may not be considered as supply of services by HO to BOs or vice-versa.

Nevertheless, there are advance rulings as discussed above that such internal employee driven activities shall be considered as service provision by one unit to another and also the intention of the law makers basis the draft circular is clear that they want to tax such activities. The correct view is yet to be validated by the judiciary in the times to come.

If for whatever reasons cross charge is not done for internally generated activities but cross charge for deemed outward supply activities (like in the example discussed in the introductory part) is done, there is a greater controversy which could be raised by the department that both are employee driven and, in both situations, cross charge should be applicable.

The draft circular also clarified that the ISD mechanism is mandatory and once common expenses are incurred by one unit or GSTIN for the company as a whole, then the ITC on such common expenses needs to be mandatorily distributed through ISD mechanism only.

The primary intention of the ISD & Cross charging mechanisms is that Common credit shall be used in the same State in which the unit is registered, to which the expense is attributable. The retention of such common credit should not happen only in one State in which the expense is incurred and consequently only such State should not use the full common credit, it should be used by all the States in which such units are registered to whom the expense was attributable.

It is also pertinent to note that if ISD mechanism is not followed for distribution of credit, but such common expenses attributable to various units of same PAN are cross charged then can this be considered as compliance of Law in spirit.

Section 20(2) uses the term “may distribute” the credit subject to conditions. Thus, if a person wants to distribute ITC then he has to take registration as an ISD and fulfil all the conditions prescribed under Section 20(2). Rule 39 of CGST Rules, 2017 prescribed for manner of distribution uses the term “shall distribute”.

Thus, it can prima facie be inferred that ISD mechanism is an option and is discretionary.

In the case of Commr. of C.T, Pune Commissionerate Vs. Oerlikon Balzers Coating India P. Ltd [2019 (366) E.LT 624 (Bom.)], it was held that:-

From the use of the word “may distribute the Cenvat Credit” found in Rule 7, the option was available to the assessee whether to distribute the Cenvat Credit or not.

In the case of Commssioner of Customs and Central Excise Vs Sri Ram Pistons and Rings [2019 (369) E.LT 631 (All)] the Hon’ble High Court has duly observed that ISD mechanism as provided for in Rule 7 of Cenvat Credit Rules, 2004 are machinery procedural provisions and cannot be construed to be mandatory.

The Hon’ble Supreme Court in the case of Sambhaji vs Gangabai [2009 (240) E.L,T 161 (SC)] has clearly stated that the procedural law should not ordinarily be construed to be mandatory, the procedural law is subservient to and is an aid to justice.

Similarly, in the case of PT.Rajan vs. T.P.M. Sahir, (2003) 8 SCC 498, the Supreme Court considered the purpose and object of the relevant provision and whether the provision itself was part of a procedural/machinery provision or substantive provision to interpret whether the word ‘shall’ appearing therein was imperative/mandatory or directory. Further, it was found that procedural provision would not be mandatory despite word ‘shall’ being employed, unless prejudice was caused.

Thus, based on the above Supreme Court rulings it is apparent that the words used in the Act “may distribute” provides with the option and it is not compulsion and once if the ISD route is taken then one has to mandatorily distribute the ITC in the prescribed manner as provided in the Rules as the words used therein are “shall distribute“. Hence, the words “shall distribute” used in the Rules are only directory in nature.

Thus, from the aforesaid various judgements it is apparent that the distribution of ITC by an ISD mechanism is just procedural Law and based on the Apex Court ruling it is clear that the procedural Law can only be directory and not mandatory.

The Act uses the words “may distribute” and Rules uses the words “shall distribute”, even then it cannot be construed that the ISD mechanism is mandatory as the word “shall” is to be construed as directory and not mandatory.

Based on overall scheme of GST Law, one must follow ISD route to distribute credit of common expenses, but on the basis of aforementioned judgements it can be determined that the ISD mechanism is not mandatory as it is just a machinery procedural provision and cannot be enforced upon a taxpayer when there is an option of cross charge available. But it does not mean that one can retain the credits at one unit and utilise it in one State. The credit should be passed on to the end State to which the expense is attributable looking into the scheme of GST Law and if the same is done through cross charge then it is possible to argue that the Law has been complied with, in spirit, even if credit is not distributed through ISD mechanism.

If a view is to be taken that such internal services are to be cross charged, the valuation mechanism to be followed, as per Rule 28, is that the open market value for such external services should be determined i.e., the value as charged by an independent third-party supplier can be considered as the open market value and the cross charge should be done at such value. However, practically it is difficult to obtain open market value for internal activities, but the 2nd proviso to Rule 28 categorically provides that if the recipient is eligible for full ITC then any value charged on the invoice shall be deemed to be the open market value.

But however, while taking shelter under the 2nd proviso to Rule 28, abundant caution must be exercised.

Intention of the Rule is to be interpreted in line with the parent section. [Section 15(5)]. Delegated legislation or subordinate legislation (Rules) cannot dilute the scope or application of the parent legislation (Act). Rules cannot undo what was set out to be achieved by the section. Procedural law cannot override substantive law. Rules cannot override the Act. If there is any conflict between a statute and a subordinate legislation, it does not require elaborate reasoning to firmly state that the statute prevails over the subordinate legislation and the bye-law if not in conformity with the statute in order to give effect to the statutory provision the Rule or bye-law has to be ignored. The statutory provision has precedence and must be complied with.

From a harmonious construction of the 2nd proviso to Rule 28 with the definition of “supply” and the principles enshrined in Section 15, it appears to be appropriate to construe “the value declared in the invoice” under the said proviso can in no way be short of the Open Market Value inter se. Section 15 clearly provides the boundaries within which every exercise of valuation must operate. Thus, 2nd proviso to Rule 28 cannot be construed or interpreted to be an escape option to tax payers to declare any value in the invoice as the open market value for discharging output tax liabilities. Doing so, would result in a complete disharmony between the rule and the section which would have never been the intention of the legislature. It is accordingly advisable to adopt a reasonably justifiable method of valuation in accordance with the hierarchy provided in Rule 28 to avoid any potential litigations.

If the recipient establishment is not eligible for full ITC, then valuation should be in following sequence:-

Open market value of such supply

Value of supply of like kind & quality

At the option of the supplier, 90% of value of supply of goods of like kind and quality as supplied by the recipient, if further supplied to unrelated party.

110% of cost of acquisition of such goods or cost of provision of such services or

Any other reasonable means.

In case of internally generated activities, if the view is taken to cross charge then it has to be valued as per valuation rules first and further charged to other units. Basis or proportion of allocation of such value of internally generated supply should be as follows:-

For the apportionment i.e., the amount so determined as per the Valuation provisions needs to be correlated with the various recipient units for the purposes of cross charge one must identify as to whether the recipient unit is a service centre or cost centre. If the recipient unit is the service centre i.e., fully independent in terms of incurring its own cost and provides services and raises relevant outward supply invoices then the common expenses may be apportioned on the basis of turnover of respective recipient units. However, if the recipient units are cost centre i.e. dependent on the head office for all its costs and outward supply invoicing then the apportionment may be done depending on the nature of common expenses.

The most preferred basis may be the turnover of the respective establishment in proportion to the total turnover of the entity. In some cases, a specific base may be used. Like in case of apportionment for internal services like Payroll processing service, HR & admin services, Number of employees may be a valid basis. For Housekeeping services and security charges, square feet area of the establishment may be a valid basis. For Maintenance services relating to equipments & plants & AMCs of various machines, the production capacity of each establishment may be a valid basis.

Agenda Item 6(iv): Clarification re2ardin2 taxability of services provided by an office of an or2anisation in one State to the office of that or2anisation in another State, both bein2 distinct persons

Various representations have been received seeking clarification on the taxability of activities performed by an office of an organization in one State to the office of that organization in another State, which are regarded as distinct persons under section 25 of the Central Goods and Services Tax Act, 2017 (hereinafter referred to as ‘the CGST Act’) and of the supply of services between such distinct persons.

2. The Law Committee has proposed to clarify the issues regarding distribution of input tax credit in respect of input services procured by the Head Office but attributable to the Head Office and /or various Branch Offices, treatment of expenses incurred by the Head Office on the procurement, distribution and management of common input services, treatment of services provided by the Head Office such as common administration or common IT maintenance to its Branch Offices and its valuation thereof, etc.

3. A draft Circular is annexed to this Agenda Note (Annexure-A) clarifying the doubts on the above subject. Similar Circular would be issued by all the States also.

4. Accordingly, the approval of the GST Council is sought for the issuance of the proposed Circular.

Annexure-A

F.No.

Government of India

Ministry of Finance

Department of Revenue

Central Board of Indirect Taxes and Customs

GST Policy Win2

*****

North Block, New Delhi

Dated : June, 2019

To,

The Principal Chief Commissioners / Chief Commissioners / Principal Commissioners / Commissioners of Central Tax (All) / The Principal Directors General / Directors General (All)

Madam/Sir,

Subject: Clarification re2ardin2 taxability of services provided by an office of an or2anisation in one State to the office of that or2anisation in another State, both bein2 distinct persons– re2.

Various representation have been received seeking clarification on the taxability of activities performed by an office of an organisation in one State to the office of that organisation in another State, which are regarded as distinct persons under section 25 of Central Goods and Services Tax Act, 2017 (hereinafter referred to as ‘the CGST Act’) and of the supply of services between such distinct persons. The issues raised in the said representations have been examined and to ensure uniformity in the implementation of the law across the field formations, the Board, in exercise of its powers conferred under section 168(1) of the CGST Act hereby clarifies the issue in succeeding paras.

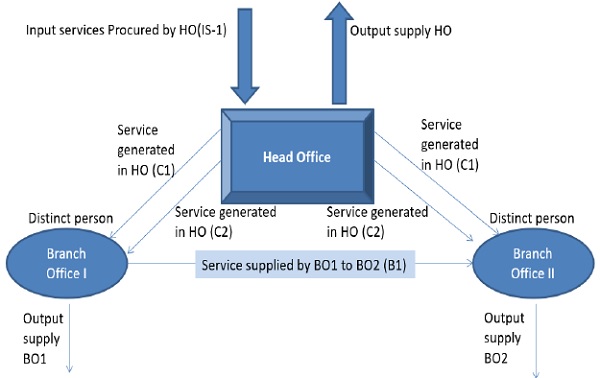

2. For better understanding the issues involved, let us take the following example: –

2.1. Let us assume that there is a business entity which has Head Office (HO) at Mumbai (HO) and two branch offices at Kolkata (BO-1) and Chennai (BO-2), as shown in the matrix above. The HO procures security service (IS – 1) for the entire organisation from a security agency located in Delhi, which deploys 10 security guards at HO and 5 each at BO-1 and BO-2.

2.2. The HO has a Personnel Department which looks after the personnel administration such as maintenance of leave record, performance evaluation, and promotion of all the employees posted at HO, BO-1 and BO-2. The activity performed by the personnel department of HO is marked as C-1. The Technical Maintenance Department of the HO does the maintenance of all the machines installed at HO, BO-1 and BO-2. The activity performed by the Technical Maintenance Department of the HO is marked as C-2.

2.3. Head Office as well as branch offices undertake software development projects for their clients. In a software development project undertaken for a client by BO-2, two engineers posted at BO-1 assisted BO-2. The activity performed by the two engineers of BO-1 for the software development project undertaken by BO-2 is marked as B-1 in the matrix above, depicting the flow of the above services within the three distinct persons of the same organisation.

3. The issues that may arise with regard to taxability of supply of services between distinct persons in terms of sub-section (4) of section 25 of the CGST Act as shown in the above matrix are being clarified in the form of questions and answers as detailed below: –

3.1. Question– Is it mandatory to distribute input tax credit (hereinafter referred to as ‘ITC’) in respect of input services (IS-1), procured by HO but attributable to both HO and BOs, following the Input Service Distributor (ISD) procedure?

Answer –Yes, it is mandatory to follow ISD procedure laid down in Section 20 of CGST Act read with rule 39 of the Central Goods and Services Tax Rules, 2017 (hereinafter referred to as ‘the CGST Rules’) for distribution of ITC in respect of input services procured by HO from a third party but attributable to both HO and BO or exclusively to one or more BOs.

3.2. Question–Will the input service (IS-1) procured by HO from a third party for use by the BOs, the ITC of which is distributed in accordance with the ISD procedure, be treated as a supply by HO to the BOs and will it be taxable in the hands of HO.

Answer – No, the services procured by HO from a third party for use at HO and BOs, or exclusively for use by BOs, the ITC of which is distributed in accordance with the ISD procedure laid down in Section 20 of the CGST Act read with rule 39 of the CGST Rules, would not be separately treated as supply by the HO to the BOs.

3.3. Question– If HO considers that procurement, distribution and management of common input services for use by HO and BOs as per ISD provisions leads to an expense, how can it apportion these expenses to the BOs?

Answer–HO may incur certain expenses on procurement, distribution and management of common input services. The HO may or may not apportion and recover such expenses from BOs. Nevertheless, such procurement, distribution and management of services by the HO for the BOs is a separate service provided by the HO to the BOs. It should be invoiced by the HO to the BOs to the extent of expense incurred by the HO. It is a service distinct from those services the ITC in respect of which has been distributed through the ISD procedure. It is for the HO to value the service as per the principles laid down in para 3.6 below.

3.4. Question– If the HO generates some services internally such as common administration by maintaining common administration team for BOs and HO (C1 in the matrix above), or common IT maintenance through a maintenance team at HO (C2 in the matrix above), where the team members are the employee of the HO, are these employees providing any service to the BOs?

Answer –

3.4.1. The offices or establishments of an organisation in different States are establishments of distinct persons under sub-section (4) of section 25 of the CGST Act and Explanation 1 of section 8 of the Integrated Goods and Services Tax Act, 2017 (hereinafter referred to as ‘the IGST Act’). GST law envisages these distinct registered persons to be independent entities, though part of one legal entity, and they can be providing services to each other.

3.4.2. Whether employees posted in HO, who look after administration of HO and BOs or maintenance of machines installed in the HO and BOs or perform similar other functions for the organization as a whole or for a particular BO which is a distinct person, are providing service to BOs is not the correct perspective to be determined here. The correct perspective for examining the issue at hand would be to determine whether the HO and BOs are providing services to each other and not whether the employee of HO is providing services to the BOs. In this case, it is the HO which is providing services to BOs.

3.5. Question– What is the legal basis for concluding that HO is providing services to the BOs in the above example?

Answer –HO and BOs are distinct persons in terms of sub-section (4) of section 25 of the CGST Act. They are also related persons as defined in Explanation (a) to section 15 of the CGST Act. It may be noted that the supply of goods or services or both between related persons or between distinct persons, when made in the course or furtherance of business is a supply even if it is made without consideration in terms of para 2 of Schedule I to the CGST Act. Thus, services produced or generated in HO by its employees and used by or supplied to BOs, with or without consideration, are supplies liable to GST. The HO should invoice such supplies to the BOs, whether HO charges any consideration for such supplies from BOs or not is immaterial. The same principle would apply for supply of services by a BO to another BO (B 1in the above matrix) or by a BO to the HO.

3.6. Question– How would these services provided by one entity to another of a body corporate, registered as distinct entities (C1 and C2 in the above matrix) be valued?

Answer-

3.6.1. As regards valuation of such supplies, since HO and BOs located in different States are related persons, value of such supplies cannot be determined under sub- section (1) of section 15 of CGST Act. The same has to be determined under sub- section (4) of Section 15 of CGST Act read with the rules made thereunder. According to rule 28 of the CGST Rules, the value of supply of goods or services between distinct persons or related persons shall,

a) be the open market value of such supply;

b) if the open market value is not available, be the value of supply of goods or service of like kind and quality;

c) if the value is not determinable under clause (a) or (b), be the value as determined by the

application of rule 30 or rule 31 of the CGST Rules, in that order.

3.6.2.The rule further provides that where the recipient is eligible for full ITC, the value declared in the invoice shall be deemed to be the open market value of the goods or services.

3.6.3. Illustration -HO has sent an annual expense budget of Rs 10 lakh for the administrative division looking after the personnel administration of the employees in HO as well as two BOs located in two different States. The value of services supplied by the HO to BO-I may be determined under rule 31 of the CGST Rules using any reasonable means consistent with the principles of valuation contained in the CGST ACT. For example, value “V” of service provided by HO to BO-1 for managing administration of staff can be determined as follows:

Value “V” = (Y/N) x Rs.10,00,000/-

Where, Y is the number of employees in BO-1;

And N is the total number of employees posted in the HO and two BOs.

3.7. Question– If there is an input service, clearly attributable to a BO, can it be contracted by the HO and paid for by the HO. How would this credit be transferred to the BO?

Answer – HO can distribute ITC in respect of input services procured on behalf of BO following the ISD procedure laid down in section 20 of CGST Act read with rule 39 of the CGST Rules. There is no restriction on HO acting as common procurement centre for all the services required by a business. If a service is specifically attributable to a BO, it shall be distributed to that BO only in terms of clause (c) of sub-section (2) of section 20 of the CGST Act.

3.8. Question– There are some services internally generated which are clearly identifiable as those pertaining to another distinct person, how would these be taxed? For example, if two persons in BO 1 do work related to IT development for a project contracted by BO-2 (service B 1 in the above matrix), how would it be taxed?

Answer-

3.8.1. In this case, BO-1 is providing service to BO-2 by way of assistance in the IT development work undertaken by BO-2. BO-1 should invoice this service to BO-2 and pay GST on it. Value of the service may be determined by using any reasonable means as illustrated below:

3.8.2. Illustration – Assuming that each of the two engineers of BO-1, who assisted in the software development project undertaken by BO-2 as shown in the above matrix, draws salary and emoluments on cost to the company (CTC) basis of Rs. 1.00 lakh per month and puts in, on an average, 200 hours of work per month, and devoted 50 hours each for the project undertaken by BO-2, the value of service (B1) supplied by BO-1 to BO-2, by way of assistance in a project belonging to BO-2, may be determined using reasonable means under rule 31 of the CGST Rules as under:

Value of service B 1= Employee cost + Establishment cost of supplying 100 man-hours.

Employee cost of 100 man-hours supplied by BO-1 to BO-2 may be calculated in this example as under:

= (100000/200)*50*2

To this may be added the establishment cost of supplying 100 man-hours following any reasonable method consistent with the generally accepted accounting principles as illustrated in para 3.6.3 above.

3.8.3. It may be noted that the question pertains to clearly identifiable service for which BO maintains record. This does not warrant that activities and services of individual employees are required to be monitored in terms of its usage by various BOs and HO. Where such accounting is not done in the normal course of business, answer as given for question 3.6 shall apply.

4. Accordingly, it is reiterated that where a taxpayer, registrant in different States, is a distinct person, then –

(i) An employee of a HO (registered as a separate entity) does not provide any services to a BO, rather it is the HO which provides service to the BO.

(ii) There is a need to apportion expenses incurred by one office for provision of output services to another office by any reasonable means consistent with the principles of valuation in the GST law and the generally accepted accounting principles.

(iii) Such apportionment/valuation of supply shall be done on the basis of information maintained by a company in its normal course of working. There is no need to maintain additional records of activities undertaken by individual employees.

(iv) The only exception to this principle would be distribution of ITC in respect of input services procured by one office and distributed to the others for which ISD provisions apply as the taxpayer is expected to mandatorily obtain ISD registration if he has to distribute ITC on input services.

5. It is requested that suitable trade notices may be issued to publicize the contents of this circular.

6. Difficulty if any, in the implementation of this circular may be brought to the notice of the Hindi version would follow.

Principal Commissioner (GST)

Author Bio