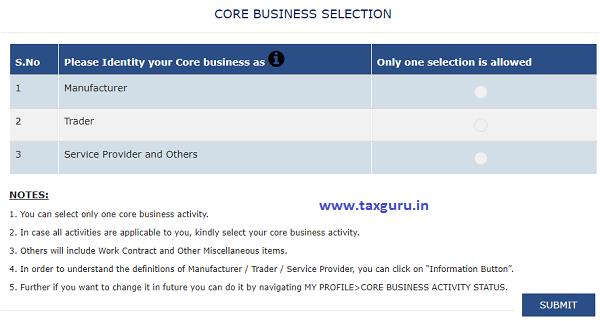

GSTN New Functionality of SELECTION OF CORE BUSINESS

The following notification is popping up these days every time the dealer logs in to the GST portal to go to the Profile page and select the nature of your Business.

All the Registered dealers are getting this notification, and you have an option to select between options, including:

- Manufacturer

- Trader whether Wholesaler / Distributor or Retailer in case of a Trading Business

- Service Provider.

There is also an option of “Others” for Businesses like Work Contractors / Job Worker and other professionals who also supply goods along with the execution of projects. Etc.

Important Points to be Noted while selecting this option:

1. Businesses are supposed to mention the category, which involves the majority of their business practices.

2. Businesses have to mention the category which is predominantly carried at that particular location.

3. For different GSTN numbers, you have to fill out different categories as per the nature of the Business of that GSTN number of your Business.

For example, Let’s assume that your company is involved in manufacturing, Trading and Services, and you generate a total of 10 crores of revenue. Out of the total 10 crores, 3 crores is from manufacturing, 5 crores are from Trading, and 2 crores is from services; your core Business activity will be Trading.

4. Every Corporate entity being a limited or private limited company files ROC returns. In the Annual returns form AOC-4, there is an option called Highest Turnover contributing product or service code (ITC/NPCS 8- digit code). One can also get to know about businesses core business activity from this field.

5. The Government thought can be aligning the core business activity with Gst and ROC returns for future data analysis.

6. This option can also be changed in case of Errors! But in that scenario, the specific Reason for Change has to be stated within the 1000 characters limit.

7. The Exact Difference between a manufacturer, Trader and Service Provider:

A Manufacturer is a registered person who produces new products from raw materials using tools, equipment, machines and then further sells them to consumers, retailers, wholesalers, and others.

A Trader is a registered person who does not manufacture but just buys and sells the same Goods. The trader can be further classified into:

- Wholesaler

- Retailer

A Service Provider is a registered person who renders services to the customer and does not manufacture or Trade in Goods.

8. Six Probable Reasons for developing this functionality and asking such kind of classification of business activities:

A. Specialisation in GST Categories

This is the Age of Specialisations. The Govt. is making all efforts to implement ADVAIT effectively in all divisions of GST.

Even in the GST Audit Manual given by the Govt., we can see different provisions for Manufacturers, Traders and Service providers in the form of:

- Separate checklists for all these categories

- Separate kinds of ratio analysis for all

- Separate document verification

B. With this categorisation in GST, it could be a possibility that the Govt. will appoint Officers dedicated to a particular category and Industry. GST Officers can be allocated for specific divisions based on their past experience and can be categorised as a specialist for a specific domain.

C. The process of finding lapses and matching data will also become automated.

D. Specific Requirements in GST

There are specific requirements earmarked for Traders, Wholesalers, Retailers, Manufacturers, Work Contractors, Warehouse Keepers, etc.

Maintaining books and records for all these is different and can be found in Rule 56 and Rule 58 of Chapter VII of CGST Rules 2017.

The Govt. can use the current categorisation to enhance compliance with all these requirements for Businesses.

E. Use of the Text Mining Technique

Firms having a turnover of more than 1 crores have to submit the business details in Form 3CD. And Bigger Businesses have to maintain the submit the Cost Audit Report. While firms constituted as the company has to submit AOC 4. Revenue details are also available at IT – TDS – 26AS and GST TDS.

With this categorisation, the Govt. will have to power to utilise the Text Mining Technique to cross- verify the data with the Revenue Details!

F. Controls on menace of fake invoicing

There can be some transaction planning, when a company in the manufacturing industry with high accumulated input credits would issue fake bills to another entity for, say, technical or consultancy services or other business auxiliary services. It can then adjust the accumulated ITC against the GST payable on the fake bills issued.

Once an entity mentions its core business activity, Gst authorities can confront it if it raises high-value invoices for one time abnormal or unusual or unrelated services.

This new feature can be to check the practice of circulation of ITC within a company. For example, a manufacturer sells to its sister company which claims to be into trading business and take services from another sister concern which claims to be into providing a service.

9. Certain businesses have been kept out of the scope of these rules which include GST Practitioners, Online information and database access or retrieval services (OIDAR), TDS deductors, embassies, etc

10. Non access of the Gst portal on non-selection of the options, the portal does not allow to move further and can restrict access of the Gst portal in future.

11. Also, there is a possibility that you can be fined Rs. 50,000 as per Section 125. (if you fail to comply even after getting a notice)

*****

Disclaimer: The contents of this article are for information purposes only and do not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.