Page Contents

- A. FAQs on Filing Application for Rectification or Taking Action in the Subsequent Proceedings under section 161 Conducted by Tax Officer

- B. Manual > Filing Application for Rectification or Taking Action in the Subsequent Proceedings u/s 161 Conducted by Tax Officer

- How can I file an application for rectification of order and participate in the subsequent proceedings u/s 161?

- A. (1) File an Application for Rectification of Order

- A. (2) View Issued Order/Notice and Open the related Case Details Screen

- B. Search for your Applications for Rectification of Order and open its Case Details Screen

- C. Take action using APPLICATIONS tab of Case Details screen: View your Filed Application

- D. Take action using NOTICES tab of Case Details screen: View issued Notice of that Application

- E. Take action using REPLIES tab of Case Details screen: View/Add your replies to the issued Notice of that Application

- F. Take action using ORDERS tab of Case Details screen: View issued Orders of that Application

A. FAQs on Filing Application for Rectification or Taking Action in the Subsequent Proceedings under section 161 Conducted by Tax Officer

Q.1 How can Rectification of errors in decision, Orders, notice or certificate or any other document be done?

Ans: Rectification of errors, which is apparent on the face of record in such decision, order, notice or certificate, can be done by the authority, who has passed such decision/order/notice, etc. either on his/her own motion or whether such error is brought to its notice by tax official or by the affected person.

Q.2 What is the time limit within which a taxpayer can file for rectification?

Ans: Taxpayer must file the rectification application within a period of three months, from the date of issue of such order.

Q.3 Can I file an application of rectification of Order if appeal is filed against that order?

Ans: If appeal is filed against assessment order, then application of rectification of Order, against that order, cannot be filed.

Q.4 What happens if a suo moto rectification done by an Adjudication Authority (A/A) adversely affects any person?

Ans: If rectification of an Order is going to adversely affect any person, then Adjudication Authority (A/A) must provide him/her an opportunity of being heard. For this, the A/A must issue “Additional Information” notice to the concerned taxpayer, hear him/her in Personal Hearing and then issue the Rectification Order.

Q.5 In the case of suo moto rectification order done by an A/A in any of my cases, how will I come to know about it and where can I view the issued orders/notice on the GST portal?

Ans: In the case of suo moto rectification done by the A/A on any order (Ref. No.), you will receive an intimation via email and SMS. You can view the issued order/notice from the following navigation: Services > User Services > View Additional Notices/Orders

Q.6 What is the procedure of rectification of order?

Ans: Following is the procedure of rectification of order:

1. Taxpayer files an application for rectification of order or an A/A initiates a suo moto rectification.

2. In case of suo moto rectification:

(a) If rectification does not adversely affect the person, then A/A can rectify and issue the rectified Order on his/her motion.

(b) If rectification of the order adversely affects the person, then A/A performs following steps 3 to 6.

3. A/A issues a notice to the taxpayer seeking additional clarifications. If personal hearing is required, personal hearing date/time/venue is also scheduled while issuing the notice.

4a. Taxpayer can reply to the issued notice and also request for a personal hearing (in case A/A has not called for a personal hearing in the issued notice) in his/her reply.

Or

4b. Taxpayer can file for application of extension offline. Tax Official can approve the application and allow Adjournment maximum 3 times.

- If A/A approves the application of extension, A/A will issue an adjournment with the new date/time and venue of personal hearing.

- If A/A does not approve the application of extension, the taxpayer will have to reply by the “Due Date for Reply” mentioned in the notice.

5a. In case of no reply from taxpayer, A/A can issue a Reminder. Maximum three such reminders can be issued. If taxpayer does not reply, even after the issue of three reminders, A/A can rectify and issue the rectified Order on his/her motion.

5b. In case the taxpayer replies on time, A/A examines the taxpayer’s reply and if a personal hearing is scheduled, hears the parties involved in the case.

6. Based on the taxpayer’s reply and personal hearing proceedings (if conducted), A/A rectifies and issues the rectified Order.

Q.7 What is the time limit for the completion of Rectification of Order related proceedings?

Ans: The Rectification Order must be passed by A/A within 6 months from date of original order, except in cases of Orders that require rectification of clerical/arithmetical mistake in them (arising from any accidental slip or omission). In such cases of clerical/arithmetical mistake in Orders, rectification order may be issued even after six months.

Q.8 What happens on the GST Portal once I file an application for rectification of order?

Ans: Once you file an application for rectification of order, following actions take place on the GST Portal:

- Acknowledgement screen is displayed, containing the generated ARN.

- You will receive an intimation of successful filing, along with the generated ARN, on your registered email and mobile.

- You will be able to view and track the ARN from the following navigation: Dashboard > Services > User Services > My Applications > Case Details > APPLICATIONS

Q.9 What documents will I receive once Notice is issued?

Ans: You will receive documents i.e. system-generated Notice for seeking clarification for rectification of order and annexure uploaded by officer.

Q.10 What happens on the GST Portal once I file a reply?

Ans: Once you file your reply, following actions take place on the GST Portal:

- Notices and Orders page is displayed with the generated Reference number (RFN).

- You will receive an intimation of successful filing, along with the generated RFN, on your registered email and mobile.

- The REPLIES tab gets updated with the record of the filed reply in a table and with the Status updated to “Reply furnished, Pending for rectification order”.

Q.11 What happens on the GST Portal if rectification order is issued?

Ans: If rectification order is issued, following actions take place on the GST Portal:

- Rectification order will be generated and intimation of issue of order shall be sent to the taxpayer via his/her registered email ID and mobile.

- Order will also be available at the dashboard of taxpayer for view, print and download.

- Electronic liability register and DCR will be updated accordingly.

- In case of application received from taxpayer, Status of ARN/RFN will get changed to ‘Order rectified’.

Q.12 What happens on the GST Portal if rectification application is rejected?

Ans: If application for rectification is rejected, following actions take place on the GST Portal:

- ‘Rejection of application for rectification’ shall be issued and intimation of issue of order shall be sent to the taxpayer via his/her registered email and mobile.

- Order will also be available at the dashboard of taxpayer for view, print and download.

- Status of ARN shall get updated to ‘Application rejected’.

B. Manual > Filing Application for Rectification or Taking Action in the Subsequent Proceedings u/s 161 Conducted by Tax Officer

How can I file an application for rectification of order and participate in the subsequent proceedings u/s 161?

To file an application for Rectification and participate in the subsequent proceedings u/s 161, perform following steps:

A. File an Application for Rectification of Order or View Issued Order/Notice and Open the related Case Details Screen

B. Search for your Applications for Rectification of Order and open its Case Details Screen

C. Take action using APPLICATIONS tab of Case Details screen: View your Filed Application

D. Take action using NOTICES tab of Case Details screen: View issued Notice of that Application

E. Take action using REPLIES tab of Case Details screen: View/Add your replies to the issued Notice of that Application

F. Take action using ORDERS tab of Case Details screen: View issued Orders of that Application

A. (1) File an Application for Rectification of Order

To file an Application for Rectification of Order, perform following steps:

1. Access the www.gst.gov.in URL. The GST Home page is displayed.

2. Login to the portal with valid credentials.

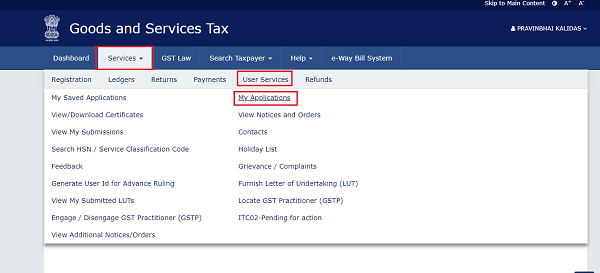

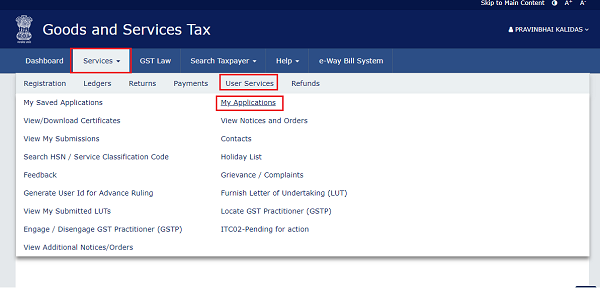

3. Dashboard page is displayed. Click Dashboard > Services > User Services > My Applications

4. My Applications page is displayed. Select “Application for rectification of order” in the Application Type field. Then, click the NEW APPLICATION button.

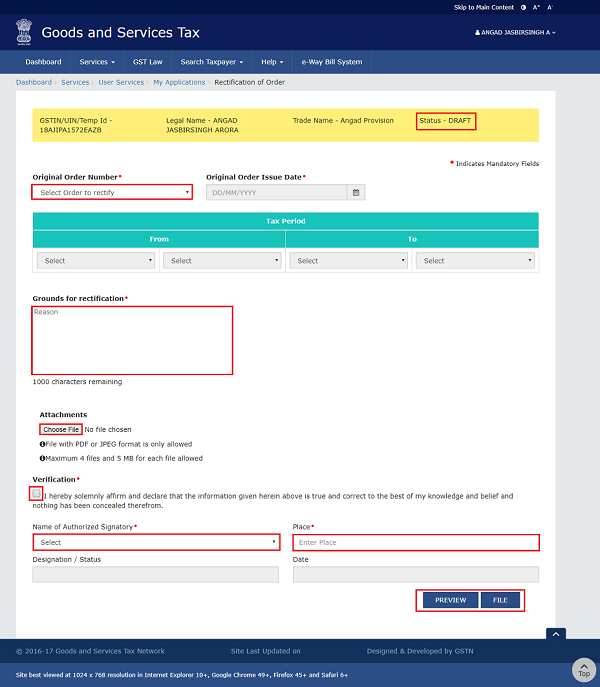

5. New Application page is displayed. Enter details in the displayed fields as mentioned in the following steps.

Note: Currently, Status of the application is “Draft”. It will remain so until you file the application.

5a. In Original Order Number field, select the order number of the order that you wish to rectify. Based on your selection, Original Order Issue Date and Tax Period fields get auto-populated.

5b. In Grounds for rectification field, enter reason for filing this application.

5c. Click Choose File to upload the document(s) related to this application, if any. This is not a mandatory field.

5d. Enter Verification details. Select the declaration check-box and select the name of the authorized signatory. Based on your selection, the fields Designation/Status and Date (current date) displayed below gets auto-populated. Enter the name of the place where you are filing this application.

5e. Click PREVIEW to download and review your application. Once you are satisfied, click FILE.

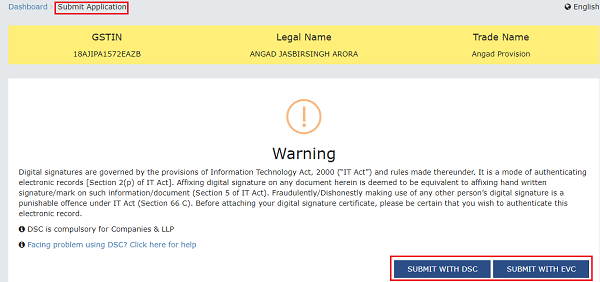

6. Submit Application page is displayed. Click ISSUE WITH DSC or ISSUE WITH EVC.

7. Acknowledgement page is displayed with the generated ARN. You will also receive an SMS and email intimating you of the generated ARN and successful filing of the application. To download the filed application, click the Click here hyperlink or click CREATE NEW APPLICATION to go back to My Applications page.

Note: Once the application is filed, Status of the application gets updated to “Pending for action by tax officer”.

To view issued order/notice related to rectification of orders and open the Case Details screen, perform following steps:

1. Access the www.gst.gov.in URL. The GST Home page is displayed.

2. Login to the portal with valid credentials.

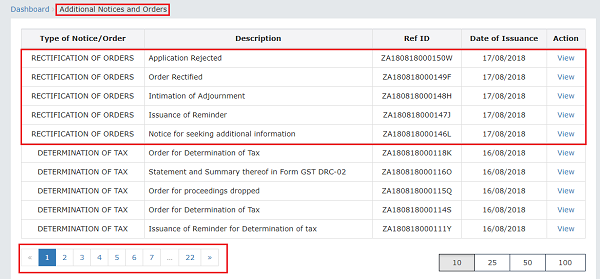

3. Dashboard page is displayed. Click Dashboard > Services > User Services > View Additional Notices/Orders

4. Additional Notices and Orders page is displayed. Using the Navigation buttons provided below, search for the Orders related to Rectification of Orders. Click View hyperlink to go to the Case Details screen of that particular Order/Notice.

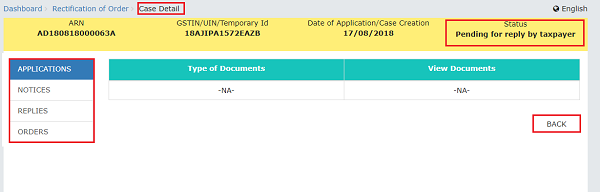

5. Case Details page is displayed. From this page, you can initiate acting on proceedings related to rectification of order u/s 161 by operating on the tabs provided at the left-hand side of the page: APPLICATIONS, NOTICES, REPLIES, ORDERS.

Note 1: On this page, the APPLICATIONS tab is selected by default.

Note 2: Currently, Status of the ARN/Case is “Pending for reply by taxpayer”. It will change as you act on the proceeding.

B. Search for your Applications for Rectification of Order and open its Case Details Screen

To search for your Applications for Rectification of Order and open its Case Details Screen, perform following steps:

1. Access the www.gst.gov.in URL. The GST Home page is displayed.

2. Login to the portal with valid credentials.

3. Dashboard page is displayed. Click Dashboard > Services > User Services > My Applications

4. My Applications page is displayed. Select “Application for rectification of order” in the Application Type field, select submission period in the From Date field and To Date fields and then click SEARCH.

5. Based on your Search criteria, applications are displayed. Click the ARN hyperlink you want to open.

6. Case Details page is displayed. From this page, you can initiate acting on proceedings related to rectification of order u/s 161 by operating on the tabs provided at the left-hand side of the page: APPLICATIONS, NOTICES, REPLIES, ORDERS. Click BACK to go back to My Applications page.

Note 1: On this page, the APPLICATIONS tab is selected by default.

Note 2: Currently, Status of the ARN/Case is “Pending for action by tax officer”. It will change as you act on the proceeding.

C. Take action using APPLICATIONS tab of Case Details screen: View your Filed Application

To view Application Details based on which this Case was created, perform following steps:

1. On the Case Details page of that particular application, select the APPLICATIONS tab, if it is not selected by default. This tab provides you an option to view the filed application in PDF mode. Click BACK to go back to My Applications page.

2. Click the View hyperlink to download and view the application in PDF mode.

D. Take action using NOTICES tab of Case Details screen: View issued Notice of that Application

To view issued Notices and File your Reply, perform following steps:

1. On the Case Details page of that particular application, select the NOTICES tab. This tab displays all the notices (Additional Information/Reminder/Adjournment) issued by Adjudication Authority (A/A).

2. Scroll to the right to view the document name(s) in the Attachments section of the table and click them to download into your machine.

E. Take action using REPLIES tab of Case Details screen: View/Add your replies to the issued Notice of that Application

To view or add your replies to the issued Notice of that Application, perform following steps:

1. On the Case Details page of that particular application, select the REPLIES tab. This tab will display the replies you will file against the Notice issued by Adjudication Authority (A/A). To add a reply, click ADD REPLY and select Additional Information.

2. Additional Information page is displayed. Enter details in the displayed fields as mentioned in the following steps. To go to the previous page, click BACK.

2a. In the Personal Hearing Required? field, select Yes or No.

Note: This button is visible in only those applications where the A/A has not called for a personal hearing in the issued notice.

2b. In Reply field, enter details of your reply to the issued notice.

2c. Click Choose File to upload the document(s) related to your reply, if any. This is not a mandatory field.

2d. Enter Verification details. Select the declaration check-box and select the name of the authorized signatory. Based on your selection, the fields Designation/Status and Date (current date) displayed below gets auto-populated. Enter the name of the place where you are filing this application.

2e. Click PREVIEW to download and review your application. Once you are satisfied, click FILE.

3. Submit Application page is displayed. Click ISSUE WITH DSC or ISSUE WITH EVC.

4. Notices and Orders page is displayed with the generated Reference number. To download the filed reply, click the Click here hyperlink. Then, click OK.

5. The updated REPLIES tab is displayed, with the record of the filed reply in a table and with the Status updated to “Reply furnished, Pending for rectification order“. You can also click the documents in the Attachments section of the table to download them.

F. Take action using ORDERS tab of Case Details screen: View issued Orders of that Application

To download order for summary assessment, perform following steps:

1. On the Case Details page of that particular taxpayer, click the ORDERS tab. This tab provides you an option to view the issued order, with all its attached documents, in PDF mode.

2. Click the document(s) in the Attachments section of the table to download them.

(Republished with amendments)

****

Disclaimer: The contents of this article are for information purposes only and does not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

Nicely explained