Limited Liability Partnerships (LLP) are emerging ever since the introduction of the Companies Act, 2013 as it is a form of business entity, which allows individual partners to be free from the concept of joint liability of partners in a partnership firm. LLPs are preferred form of business as it is an alternative corporate business vehicle that provides the benefits of limited liability of a company and allows its members the flexibility of organizing their internal management on the basis of a mutually arrived agreement, as is the case in a partnership firm.

A registered limited company in India (Private or Public) has a lot of complex formalities and incurs additional overheads for managing affairs including mandatory board meeting, maintenance of statutory records, filling of e-forms with MCA etc. Absence of such mandates for LLP combined with advantages such as non-applicability of dividend distribution tax on profit repatriation, transfer of profit rules and deemed dividend profit issues, MAT provisions and many more.

Hence, LLPs involve the best practices of private companies and also protect the freedom of partners, giving them the ability to decide the norms of the company. In a nutshell, it combines the best features of various kinds of businesses.

Accordingly, in this article, we shall discuss about the procedure and provisions w.r.t. conversion of a Private Ltd. or unlisted Public Company into LLP:

Requirements for conversion of company into LLP

- Every member of the company must agree with the decision of conversion.

- All the members become the partners of an LLP and no one else.

- The latest copy of Income tax return is to be filed with ROC.

- Not just the members, all the creditors of the company must also agree with the conversion.

- Under Companies Act, no prosecution should have been initiated procedure to be followed

- No open (unsatisfied) charges should be pending against the company.

- At least one balance sheet and annual return should have been filed by the company after its incorporation.

- The company should be having share capital.

- The company should not be a ‘Section 25 company’/ ’Section 8 Company under Companies Act, 1956/2013.

Taxation Aspect of Conversion

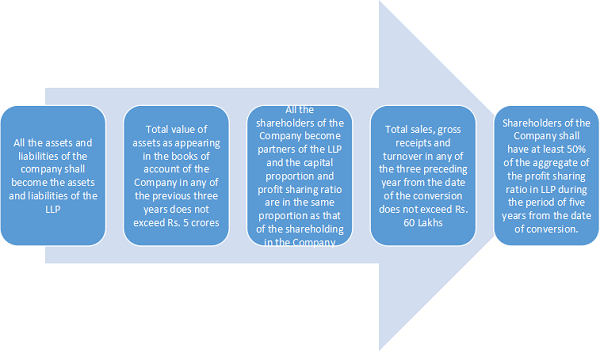

As per Sec 47 of the Income Tax Act, 1961, conversion of Company into LLP will not attract capital gain tax if all the following conditions are satisfied:

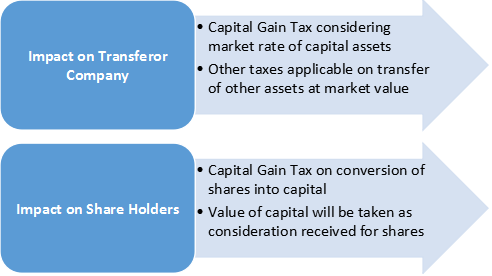

Consequences of violation of above conditions are as below:

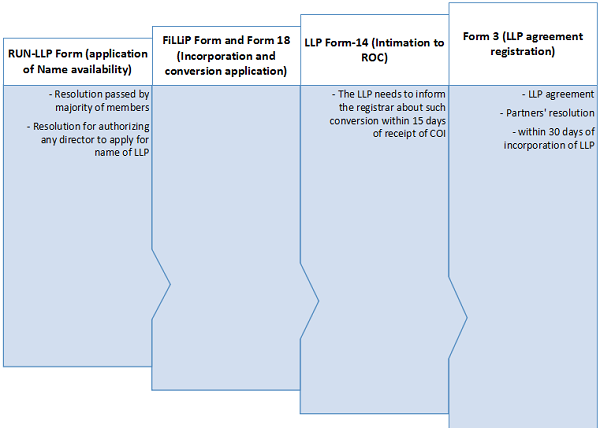

Procedure for Conversion

Documents required to be filed for Conversion

Conclusion

Owing to flexibility in its structure, compliances, tax and operation, LLP would be useful for small and medium enterprises, in general, and for the enterprises in services sector and professional firms, in particular. Internationally, LLPs are the preferred vehicle of business, particularly for service industry or for activities involving professionals. The conversion from the existing corporate structure can be made to a LLP while retaining the advantages of Limited Liability and less compliances.

About the Author

Author is Divya Goel, ACS working as Assistant Manager- Company Secretary with Neeraj Bhagat & Co. Chartered Accountants, a Chartered Accountancy firm helping foreign companies in setting up business in India and complying with various tax laws applicable to foreign companies while establishing their business in India. Author can be reached at info@neerajbhagat.com.