A Start Up in common parlance means a project undertaken by entrepreneur seeking to develop a scalable business model. The Government of India in order to streamline and promote all such brain child ideas launched an initiative called Start Up India on 16th January 2016. It intended to build a strong network nurturing all the innovative ideas leading to massive wealth and employment creation. A Start Up can also be a newly established business but some of the parameters differs it from the traditional business.

The Start Up India has initiated several programs under the leadership of the Prime Minister, Shri Narendra Modi. In order to maintain uniformity among all the enterprises, the Department for Promotion of Industry and Internal Trade (DPIIT), Ministry of Commerce and Industry (MCI) and Government of India has defined following prerequisites to be categorised as a Start up:

Age of the Company: Incorporated less than 10 years ago

Type of Company: Should have been registered as Private Limited Company/ Partnership Firm/ Limited Liability Partnership

Annual turnover: Turnover of entity for any of the financial year since incorporation should not exceed INR 100 Crores.

Original Entity: The Company should not have been formed by splitting up or restructuring of existing business. It should be originally formed by the promoters.

Innovative and Scalable: The entity should work towards innovation, development and improvement of product and services. Also, the business model should have potential to scale up to generate wealth and employment.

Registration Procedure with Start up India

- Incorporate Business: Obtain Certificate of Incorporation/ partnership Registration, PAN and other compliances.

- Register with Start Up India: Log on to Start Up India website and after filling the details online, create Start Up India profile

- Get DPIIT Recognition: This helps the start up to avail various benefits, relaxations and exemptions. Recognition is applied online by filling the details.

- Documents required for Registration: Incorporation Certificate, details of Directors, Proof of concept like website link or video, PAN and Patent/ Trademark details (Optional)

- Recognition Number: Immediately on application for Recognition, a recognition number gets generated. Certificate of recognition is issued within the period of 2 days after validating all the documents. On erraneous uploading of documents, the start up shall be liable to the fine upto 50% paid up capital with minimum fine of INR 25,000.

Benefits from DPIIT

Companies registered under DPIIT are eligible for various benefits.

1. Simple and easy process of registration for start up

2. Tax Holiday for a period of 3 years (Sec 80 IAC)

3. Various benefits with respect to Intellectual Property Rights (IPR)

4. Government to ensure fund of funds to be infused into Start up ecosystem

5. Relaxation in Public Procurement norms for start ups

6. Self Certification is permitted for compliance with labour and Environment laws

7. Faster Exit and simple winding up process is designed in case of start up failure

8. Several Research parks are in pipeline to provide Research & Development facilities to the start ups

Sweat Equity Shares in Start Ups

Sweat Equity shares are the equity shares allotted by the company to its employees or the directors in exchange for their expertise and time they put in for the setting up the business. It gives a sense of ownership and they can derive benefits once the valuation of company rises.

As per Sec 2(88) of the Companies Act 2013, Sweat Equity shares mean shares issued by a company to its directors or employees for non cash consideration or at a discount for making rights available in the nature of intellectual property rights or providing know-how or any value additions in any form.

Start ups in their initial phase of setting up the business usually face cash crunch, so they resort to sweat equity shares to reward their employees.

Quantum for Issue of Sweat Equity Shares – The Company shall not issue Sweat Equity Shares for more than:

> 15% of the existing Paid up Equity Share Capital in a year or

> Shares of the issue value of INR 5 Crores whichever is higher

Cumulatively a Start up may issue Sweat Equity shares up to 50% of the Paid up Capital for the period of 10 years from the date of incorporation.

Amid the pandemic COVID 19, Government of India has come up with the amendment, bringing a great sigh of relief for the start ups. It has allowed start ups to issue sweat equity shares for the period of 10 years from their registration/ incorporation. Ministry of Corporate Affairs (MCA) has amended Companies Rules 2014, and allowed issue of sweat equity upto 50% of their paid up capital as opposed to 25% earlier. Outbreak of COVID 19 has slowed down the business creating immense liquidity pressure, declining revenues and funding issues. Extending the limit from 5 years to 10 years will help start ups to retain their core employees by incentivising them well.

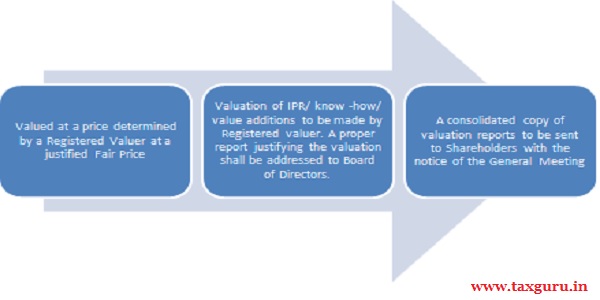

Valuation of Sweat Equity Shares

Sweat Equity Shares issued to Directors and the key employees shall have a lock-in period or made non transferable for a period of 3 years from the date of allotment. The lock in period shall be mentioned in bold prominent manner on the share certificate. Also, the issue of Sweat equity shares shall be disclosed by the Board of Directors in the Director’s Report for that year.

Procedure of Issuance of sweat Equity Shares

- Board Meeting is called serving the notice atleast 7 days before to discuss the proposal of issue of Sweat Equity shares and fix up the date for EGM

- Issue notice of General Meeting atleast 21 days prior to the date of meeting with the Explanatory statement annexed along

- Pass resolution for the issue of Sweat Equity Shares in the General Meeting called. File the form MGT-14 with Registrar within 30 days of passing the reolution.

- Call the next Board Meeting for passing the resolution for allotment of shares. Once the resolution is passed, file form PAS – 3 with Registrar within 30 days. Shares must be issued within 12 months from the date of passing the special resolution.

- After the allotment of shares, Company shall maintain a register of sweat equity shares in form SH-3 with all the details and particulars of the shares alloted .

Taxability of Sweat Equity Shares

Sweat Equity Shares are taxable in the hands of Employee in two instances:

1. At the time of Allotment – Will be taxable under the head Salary in the year in which shares are allotted or transferred to the employees

2. At the time of sale of such sweat Equity Shares – Will be taxable under the head Capital Gains in the year in which such shares are transferred by the Employee

Issue of Sweat Equity Shares to Persons Resident outside India

Indian company may issue Sweat Equity shares to its Employees/ Directors or Employees/ Directors of its holding company or joint venture or wholly owned overseas subsidiary/subsidiaries who are resident outside India, provided that:

> It is in line with the regulations issued by SEBI Act 1992 or the Companies Rules 2014 notified by the Central Government under the Companies Act 2013

> It is in compliance with the Sectoral cap applicable to the said company

> Where foreign investment is under approval route, it shall require prior approval of Foreign Investment Promotion Board (FIPB) of Government of India

> Citizen of Pakistan/Bangladesh shall require prior approval of Foreign Investment Promotion Board (FIPB) of Government of India

About the Author

Author is Ruchika Bhagat, FCA helping foreign companies in setting up and closure of business in India and complying with various tax laws applicable to foreign companies while establishing a business in India. Neeraj Bhagat & Co. Chartered Accountants, is a well-established Chartered Accountancy firm founded in the year 1997 with its head office at New Delhi.

Author is Ruchika Bhagat, FCA helping foreign companies in setting up and closure of business in India and complying with various tax laws applicable to foreign companies while establishing a business in India. Neeraj Bhagat & Co. Chartered Accountants, is a well-established Chartered Accountancy firm founded in the year 1997 with its head office at New Delhi.