Default in Declaration in respect of beneficial interest in any share under Section 89 of Companies Act, 2013: MCA imposes Penalty of Rs. 16.80 Lakh

On July 30, 2024, the Ministry of Corporate Affairs (MCA), through the Registrar of Companies, NCT of Delhi & Haryana, imposed a significant penalty on Hygosap Pharma Private Limited (formerly Burroughs Welcome Pharmacia Private Limited). This penalty, amounting to Rs. 16.80 lakh, arises from non-compliance with Section 89 of the Companies Act, 2013.

1. Appointment of Adjudicating Officer

The Registrar of Companies, NCT of Delhi & Haryana was appointed as the Adjudicating Officer as per Gazette Notification No. A-42011/112/2014-Ad.II, dated March 24, 2015. This appointment was made under the powers conferred by Section 454(1) of the Companies Act, 2013 and the Companies (Adjudication of Penalties) Rules, 2014. The role of the Adjudicating Officer is to oversee and adjudge penalties for non-compliance with various sections of the Companies Act.

2. Company Overview

Hygosap Pharma Private Limited, incorporated on January 22, 2021, has its registered office in Pitampura, Delhi. For the financial year 2023-24, the company reported a paid-up capital of INR 0.10 lakh, a revenue from operations of INR 658.81 lakh, and a profit of INR 395.95 lakh. Despite being a wholly-owned subsidiary of Akums Drugs & Pharmaceuticals Limited, Hygosap Pharma faced scrutiny for non-compliance with mandatory declarations under Section 89 of the Companies Act.

3. Case Facts and Proceedings

The case originated from observations that the company had failed to comply with Section 89 of the Companies Act, which requires declarations regarding beneficial ownership of shares. Specifically, the company did not file Form MGT-6 as required under Rule 9(3) of the Companies (Management and Administration) Rules, 2014.

- Show Cause Notice: On September 29, 2023, a show cause notice was issued for non-compliance. The company’s response claimed that the provisions of Section 89 were not applicable as Akums was both the beneficial and registered owner.

- Subsequent Findings: During hearings held on October 23, 2023, and February 26, 2024, discrepancies were noted in the submission of Form MGT-4 and MGT-5. The forms were found to be backdated, and there was insufficient proof of receipt. This raised concerns about the authenticity of the documents submitted by the company.

4. Observations and Penalty Imposition

The Registrar of Companies identified several issues:

- Backdating and Document Discrepancies: The forms were digitally created and backdated, raising concerns about their validity. The company failed to provide credible proof of receipt for the forms.

- Non-Compliance with Filing Requirements: The delay in filing Form MGT-6 and discrepancies in the forms led to the conclusion that the company had not met its obligations under Section 89.

The penalty was adjudged as follows:

- For Violation under Section 89(1): The penalty for non-filing of declarations by registered owners was calculated at Rs. 1,90,000 per individual.

- For Violation under Section 89(6): The penalty for the company and its officers for the delayed filing of Form MGT-6 amounted to Rs. 5,00,000 for the company and Rs. 2,00,000 each for directors, with a reduced penalty for directors who served for shorter periods.

GOVERNMENT OF INDIA

MINISTRY OF CORPORATE AFFAIRS,

OFFICE OF REGISTRAR OF COMPANIES,

NCT OF DELHI & HARYANA

4TH FLOOR, IFCI TOWER, 61, NEHRU PLACE,

NEW DELHI -110019

ORDER OF PENALTY PURSUANT TO SECTION 89 OF THE COMPANIES ACT, 2013 IN THE MATTER OF HYGOSAP PHARMA PRIVATE LIMITED (Formerly knowns as BURROUGHS WELCOME PHARMACIA PRIVATE LIMITED) (U24290DL2021PTC376044)

1. Appointment of Adjudicating Officer: –

Ministry of Corporate Affairs vide its Gazette Notification No. A-42011/112/2014-Ad.II, dated 24.03.2015 appointed Registrar of Companies, NCT of Delhi & Haryana as Adjudicating Officer in exercise of the powers conferred by section 454(1) of the Companies Act, 2013 (hereinafter known as Act) r/w Companies (Adjudication of Penalties) Rules, 2014 for adjudging penalties under the provisions of this Act.

2. Company: –

Whereas the company viz. HYGOSAP PHARMA PRIVATE LIMITED (formerly known as BURROUGHS WELCOME PHARMACIA PRIVATE LIMITED) (herein after known as ‘company’ or ‘subject company’) was incorporated on 22.01.2021 and has its registered office as per MCA21 Register address at Unit No. 201, 2nd Floor, LSC, Mohan, Place, BLK-C, Saraswati Vihar, Pitampura, DELHI, North West,Delhi,110034,India. The financial & other details of the subject company for the immediately preceding F.Y 2023-24 as available on MCA-21 portal is stated as under:

| S. No. | Particulars | Details |

| 1. | Paid up capital (INR in lakhs) | 0.10 |

| 2. | a. Revenue from operation (INR in lakhs) | 658.81 |

| b. Other Income (INR in lakhs) | 19.37 | |

| c. Profit for the Period (INR in lakhs) | 395.95 | |

| 3. | Holding Company | YES |

| 4. | Subsidiary Company | NO |

| 5. | Whether company registered under Section 8 of the Act? | NO |

| 6.

|

Whether company registered under any other special Act? | NO

|

3. Facts about the Case: –

(i) It was observed from the records that company has filed its Annual Return for F.Y. 2022-23 vide eform MGT-7 (SRN F61755088) wherein it is mentioned that AKUMS DRUGS AND PHARMACEUTICALS LIMITED is holding 100% shares in the subject company. However, it was seen that company had in total 3 (three) shareholders. Therefore, the beneficial holder and the registered holder ought to have declared the status of their interest in the shares in terms of Section 89(1) and Section 89(2) of the Act respectively. Further, it was also seen that the company did not file MGT-6 in term of Rule 9 (3) of Companies (Management and Administration) Rule, 2014.

(iii) In view of above, a show cause notice u/s 89 of the Act was issued on 29.09.2023 to the company and its then current directors with a direction u/s 20 of the Act that the company shall serve this notice to all the officers in default.

(iii) In response to the said SCN, a reply has been received from the company on 10.10.2023 which inter alia states as under:

a) It is hereby submitted that the company is wholly owned subsidiary of Akums Drugs & Pharmaceuticals Limited (Akums) and to ensure the minimum number of members in the company as per statutory limit under Section 3 and 3A of the Act, allowing two of its directors to hold one share each in the company as Nominee Shareholders (on behalf of Akums).

b) Further, section 89 of the act shall be applicable on those cases where beneficial owner is not shown as registered owner and the company is unknown with the details of actual beneficial owner. Whereas in the given case, Akums it is not only beneficial owner but also registered owner of the company whose name is recorded in the register of members of the company.

Resulting section 89 of the Act shall not at all be applicable on the company its officers or its members.

c) Since the company is wholly owned subsidiary of Akums and the other shareholders holding one share each as nominee shareholder only (on behalf of Akums). Therefore, there is no requirement to submit any declaration under section 89(1) and 89(2) of the Act in form MGT 4 and MGT 5 respectively by the members and consequently question of filing of for MGT- 6 under section 89(6) by the company does not arise

(iv) In view of submissions made in reply, a hearing in the matter was scheduled for oral submissions on 20.10.2023 which was rescheduled on 23.10.2023 wherein Shri. Vishant Kumar Jain, PCS, an Authorised representative (AR) of the Company appeared for hearing and submitted as under:

a) AR of Company submitted that upon re-verification, it has come to the notice of the company that it is already in receipt of form MGT-4 and form MGT-5 from the registered owners and from the beneficial owners of two shares. Therefore, earlier written submission made by the company whereby it was stated that provisions of 89(1) and 89(2) of the Act are not applicable were withdrawn.

b) In view of the submissions, company was asked to provide the copies of form MGT-4 and form MGT-5 received by itself along with proof receipt/dispatch.

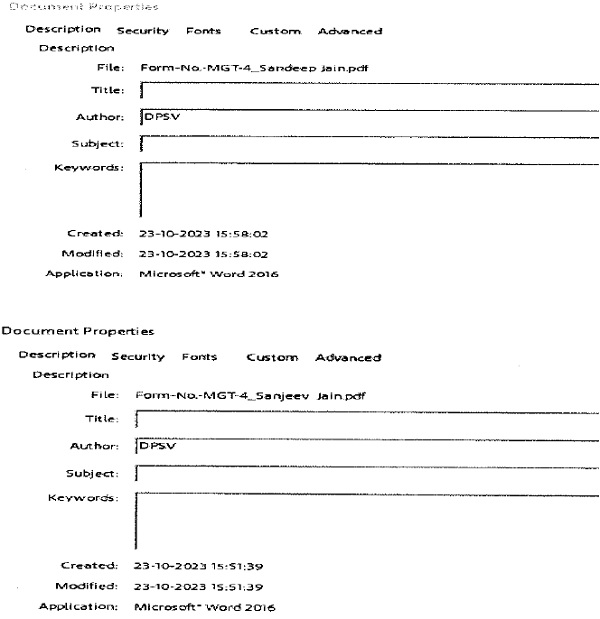

(v) Subsequently, a reply from the company was received vide email dated 26.10.2023, wherein the copy of form MGT-4 and MGT-5 were attached to the said email. The copy of form MGT-4 submitted to this office through email showed that it was created digitally only on 23.10.2023 using Microsoft Word 2016 and later it was converted into a pdf file. At the same time, the signatures of Shri Sandeep Jain and Shri Sanjeev Jain were pasted on the said document. The document was dated 25.10.2021. But the electronic properties of the document showed a different picture. Additionally, no proof was submitted by the company to show the receipt of forms MGT-4 and MGT-5 by it. It is also observed that the company has filed form MGT-6 on MCA portal vide SRN F75812339 dated 30.10.2023.

(vi) In view of the submission made by the company, an email was sent on 17.11.2023 seeking clarification on the observations made by this office. In response to which, a reply was received on 28.11.2023 (letter dated 23.11.2023) along with which physical copies of MGT-4 and MGT-5 was submitted. However, the reply did not seem to be satisfactory.

(vii) In view of the above, an additional hearing was scheduled on 26.02.2024. Shri. Dharamvir Malik, Company Secretary of the Holding Company (duly authorized by the directors) appeared for hearing wherein he was asked to provide a clarification with regard to the discrepancy noted in form MGT-4 and also to provide a clarification with respect to the proof of receipt of the declarations in form MGT-4 and MGT-5. Thus, company was required to show cause as to why the form MGT-6 filed vide SRN F75812339 dated 30.10.2023 should not be disregarded for the purpose of adjudication of this matter.

(viii) Subsequent to hearing dated 26.02.2024, a reply from the company was received on 04.03.2024 wherein inter alia stated as follows:

“With the submission of original/ hard copies of MGT-4 and MGT-5 the question creation of documents should not arise as any scan document will show its date of creation when that document was converted into scan from original hardcopy.”

Thus, the company has affirmed that the hard copies of the declarations have been received from the beneficial owner and the registered owner in the past and that they were hand delivered.

4. Observations

i) When the notice of adjudication was issued for non-filing of MGT-6 as required under Section 89 of the Act and rules made thereunder, the company submitted that since the section 89(1) and 89 (2) is not applicable, therefore it has not received any declaration in MGT-4 and MGT-5 and accordingly it was not required to file MGT-6 and accordingly there is no non-compliance.

ii) But when the hearing was held on 23.10.2023, the AR of the company submitted that subsequent to the notice, a re-verification was done, and it was found that company is in receipt of MGT-4 and MGT-5. Accordingly, the company was asked to provide the copies of MGT-4 and MGT-5 received by it along with proof of receipt/dispatch. Subsequently, vide email dated 26.10.2023, the company submitted the following documents:

a. Scanned copy of form MGT-5 dated 25.10.2021 submitted by the beneficial owner wherein date of acquisition of beneficial interest is 29.09.2021.

b. A pdf copy of form MGT-4, which was created digitally only on 23.10.2023 using Microsoft Word 2016. The screenshot showing the document properties is as under:

iii) The copy of MGT-4 submitted through email is clearly back-dated and was produced as an afterthought by the company when the notice was received.

iv) When the issue was raised, the company submitted physical copies of forms MGT-4 and MGT-5 which carried the below-mentioned receiving by the subject company:

THIS FROM MGT-H HAS BEEN RECEIRED BY BURROUGHS WELCOME PHARMACIA. PVT. LTD. (THE COMPANY) ON 26th OCT, 2001

Burroughs Welcome Pharmacia Pvt. Ltd.

Director/Authorised Sinuated

“THIS FORM MGT-5 HAS BEEN RECEIVED BY BURROUGHS WELCOME PHARMACIA PVT. LTD. (THE COMPANY) ON 26th OCTOBER, 2021.

Burroughs Welcome Pharmacia Pvt. Ltd.

Director/Authorised Sinuated

v) However no response was submitted on the observation that copies were digitally created on 23.10.2023 while the document is dated 25.10.2021.

vi) The company has filed MGT-6 e-form vide SRN F75812339 dated 30.10.2023 wherein the copies of MGT-4 and MGT-5 are attached. However, the MGT-4 and MGT-5 do not have the receiving statement as is mentioned in the physical copies.

vii) In this regard, reference is also required to be made to rule 8(6) of the Companies (The Registration Offices and Fees) Rules, 2014 which states as under:

“Scanned image of documents shall be of original signed documents relevant to the e-forms or forms and the scanned document image shall not be left blank without bearing the actual signature of authorised person.”

viii) Thus, it is quite clear the company has multiple sets of form MGT 4 and MGT-5, one set is attached with eform MGT-6 and there is another set on which receiving is mentioned.

ix) On the basis of the records available in our record and the records produced during the proceedings the non-compliance of Section 89 of the Act could be seen as follows:

a. The date mentioned on the form MGT-4 is not reliable due to the aforesaid reasons. There is evidently an attempt to back-date the compliance so that the liability of the registered owner can be avoided. In such a circumstance the filing made by the company cannot be considered. Moreover, it is clear that the copy of the form MGT-4 attached to the eform MGT-6 filed by the company is at variance with the copy submitted to this office [which contains a receiving given by the company]. Accordingly, as per Section 89(1) of the Act and rules made thereunder, the liability of the two registered owners under section 89(5) for not submitting the form MGT-4 within a period of 30 days of entry of their name in the register of member would subsist which is 29.09.2021 (as has been disclosed by the beneficial owner in MGT-5). This liability is being calculated from 29.10.2021 to date of issue of SCN i.e 29.09.2023.

b. Form MGT-5 is a scanned version of the physical copy, so the contention of the company that it was received on 26.10.2021 cannot be ruled out. Now as per Section 89(2) of the Act, the beneficial owner has submitted its declaration on 26.10.2021 and accordingly the company was required to file MGT-6 within 30 days i.e. 25.11.2021. However, MGT-6 has not been filed till the date of issue of notice dated 29.09.2023. Accordingly, the subject company and its officers are liable for penal action under Section 89(7) of the Act. In addition, the issue of having different copies of form MGT-5 is also seen in this. The copy attached to form MGT-6 is not a true copy.

5. The relevant provision of the Act and Rules therewith:

Section 89. Declaration in respect of beneficial interest in any share:

(1) Where the name of a person is entered in the register of members of a company as the holder of shares in that company but who does not hold the beneficial interest in such shares, such person shall make a declaration within such time and in such form as may be prescribed to the company specifying the name and other particulars of the person who holds the beneficial interest in such shares.

(2) Every person who holds or acquires a beneficial interest in share of a company shall make a declaration to the company specifying the nature of his interest, particulars of the person in whose name the shares stand registered in the books of the company and such other particulars as may be prescribed.

(5) If any person fails to make a declaration as required under sub-section (1) or sub-section (2) or sub-section (3), he shall be liable to a penalty of fifty thousand rupees and in case of continuing failure, with a further penalty of two hundred rupees for each day after the first during which such failure continues, subject to a maximum of five lakh rupees.

(6) Where any declaration under this section is made to a company, the company shall make a note of such declaration in the register concerned and shall file, within thirty days from the date of receipt of declaration by it, a return in the prescribed form with the Registrar in respect of such declaration with such fees or additional fees as may be prescribed.

(7) If a company, required to file a return under sub-section (6), fails to do so before the expiry of the time specified therein, the company and every officer of the company who is in default shall be liable to a penalty of one thousand rupees for each day during which such failure continues, subject to a maximum of five lakh rupees in the case of a company and two lakh rupees in case of an officer who is in default.

Rule 9 of Companies (Management and Administration) Rule, 2014

(1) A person whose name is entered in the register of members of a company as the holder of shares in that company but who does not hold the beneficial interest in such shares (hereinafter referred to as 9 “the registered owner”), shall file with the company, a declaration to that effect in Form No.MGT.4 in duplicate, within a period of thirty days from the date on which his name is entered in the register of members of such company:

(2) Every person holding and exempted from furnishing declaration or acquiring a beneficial interest in shares of a company not registered in his name (hereinafter referred to as “the beneficial owner”) shall file with the company, a declaration disclosing such interest in Form No. MGT.5 in duplicate, within thirty days after acquiring such beneficial interest in the shares of the company:

(3) Where any declaration under section 89 is received by the company, the company shall make a note of such declaration in the register of members and shall file, within a period of thirty days from the date of receipt of declaration by it, a return in Form No.MGT.6 with the Registrar in respect of such declaration with fee.

6. Adjudication of penalty

The subject company does not get covered under the purview of small company as defined u/s 2(85) of the Act. Hence, the benefit of section 446B would not be applicable on the company. Now in exercise of the powers conferred vide Notification dated 24th March, 2015 and having considered the reply submitted by the noticee (s) in response to the notice issued and hearing held, I do hereby impose the penalty on the company and its officers in default as under:

A. For default u/s 89(1) of the Act in respect of the registered owner:

Table-I

| Violation section period & | Penalty imposed on company/ director(s) | Calculation of penalty amount u/s 89(5) (in Rs.) | Penalty imposed (in Rs.) |

| A | B | C | D |

| 89 (delay 700 (1) of | Sh. Sandeep Jain, Registered Owner | 50000+ 200×700= 190000 | 190000 |

| Sh. Sanjeev Jain, Registered Owner | 50000+ 200×700= 190000 | 190000 |

B. For default u/s 89(6) of the Act n respect of company and its officers:

Table-II

| Violation section & period | Penalty imposed on company/ director(s) | Calculation of penalty amount u/s 89(7) (in Rs.) | Penalty imposed (in Rs.) |

| A | B | C | D |

| 89 (6) (delay of 673 days in filing of from MGT- 6) |

Burroughs Welcome Pharmacia Private Limited (company) | 673 x 1000 = 6,73,000 Subject to maximum 5,00,000 | 5,00,000 |

| Arushi Jain (Director) | 673 x 1000 = 6,73,000 Subject to maximum 2,00,000 | 2,00,000 | |

| Umang Jain (Director) | 673 x 1000 = 6,73,000 Subject to maximum 2,00,000 | 2,00,000 | |

| Shivangi Jain (Director since 24.03.2022) | 554 x 1000 = 5,54,000 Subject to maximum 2,00,000 | 2,00,000 | |

| Pranav Trikha (director 26.09.2022 to 03.8.2023) | 311 x 1000 = 3,11,000 Subject to maximum 2,00,000 | 2,00,000 |

7. Order:

a. Names of parties as mentioned in the table I and table II above are hereby directed to pay the penalty amount as per column no. ‘D’ therein. In case of parties other than company, such amount is required to be paid out of their own funds.

b. The said amount of penalty shall be paid through online by using the website mca.gov.in (Misc. head) in favor of “Pay & Accounts Officer, Ministry of Corporate Affairs, New Delhi, within 90 days of receipt of this order, and intimate this office with proof of penalty paid.

c. Company to file MGT-6 with true copies of form MGT-4 and MGT-5.

d. Appeal against this order may be filed with the Regional Director (NR), Ministry of Corporate Affairs, B-2 Wing, 2nd Floor, Paryavaran Bhawan, CGO Complex, Lodhi Road, New Delhi-110003 within a period of sixty days from the date of receipt of this order, in Form ADJ [available on Ministry website mca.gov.in] setting forth the grounds of appeal and shall be accompanied by a certified copy of the order. [Section 454(5) & 454(6) of the Act read with Companies (Adjudicating of Penalties) Rules, 2014].

e. Your attention is also invited to section 454(8) of the Act in the event of non-compliance of this order.

(Pranay Chaturvedi, ICLS)

Registrar of Companies

NCT of Delhi & Haryana

No. ROC/D/Adj/Order/89/BURROUGHS/3005-3012

Date:30/07/2024