In the fight against black money and in attempting to promote governance culture, the Indian government is constantly finding new weapons viz. demonetisation, roll out of Goods and Services Tax, introduction of new laws such as RERA, Insolvency and Bankruptcy Code, etc. The government is also plugging loopholes in existing laws and regulations through amendments. In exercising the powers conferred under proviso to clause (87) of section 2 to restrict the number of layers of subsidiaries a holding company can have, the Ministry of Corporate Affairs on 20 September, 2017 notified Companies (Restriction on number of layers) Rules, 2017 (Rule). As per the rule, a Company cannot have more than two layers of subsidiaries.

In the past, it has been observed that multiple layers of shell companies have been floated for diversion of funds, tax evasion or money laundering. The restriction on number of layers of subsidiaries has been introduced to clampdown on illicit fund flows.

However, this rule is not applicable to a banking company, non-banking financial company, insurance company and a government company.

The Rule exempts one layer of wholly owned subsidiary for calculating the limit of two layers. The Rule here should not be read as any layer represented by a wholly owned subsidiary. For instance:

Whether Company “Co. X” can avail the exemption for the layer represented by “Co. A,” which is not a wholly owned subsidiary of “Co. X.”

From a reading of the Rule, it seems that the layer of wholly owned subsidiary has to be seen with regard to the first holding company and not thereafter in order to avail the exemption. Say in the above example 2, Co. Y is a wholly owned subsidiary, then that layer would not be counted, and hence, Co A may be set up as a WOS/ subsidiary. However, in example 1, as Co. Y is not a WOS of Co. X it would be considered as violation of rule.

Additionally, an exemption is provided for subsidiaries incorporated outside India. According to the provisions, an Indian company can acquire a company incorporated outside India which may have several layers of subsidiaries beyond two but not beyond the limit permitted as per the law of the host country. Technically, this limit shall count with reference to the top layer of the foreign subsidiary in the host country. The language suggests that the exemption is only at the time of acquisition of the company and not otherwise. Therefore, if the Indian company freshly incorporates any subsidiary outside India or tries to acquire any further subsidiary/ies, it would have to adhere to this rule.

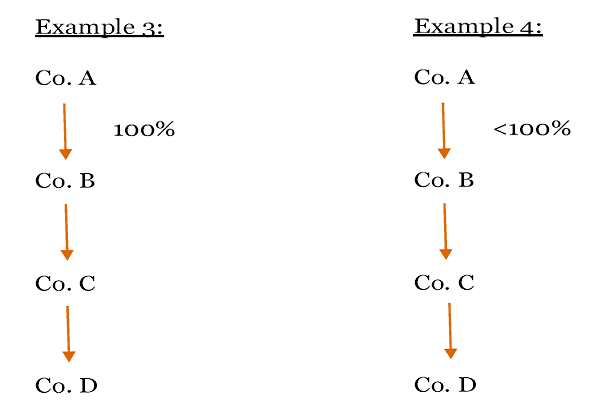

Further, one may want to draw analogy to section 186(1), wherein similar restriction on number of layers of investment companies has already been in force. It is pertinent to note that while section 186(1) puts a restriction on the layers of investment companies, it did not restrict the number of operating companies. However, this Rule is ubiquitous and would apply to all classes of companies, including investment companies covered under section 186. Therefore, post applicability of the Rule, a company cannot form more than three layers (one layer of WOS included) of companies for both operating and investment companies. As discussed earlier, if the first layer is not a WOS the parent company cannot have more than two layers of subsidiaries. Therefore, the rule is more restrictive in nature. We have tried explaining the same with an example:

In example 3, if investment Co. A has a WOS B, which is an investment co and has a subsidiary C. C, now wants to takeover operating Co. D. Is this possible?

Yes, Co A could continue with all of them as its subsidiaries since B would be exempted from counting two layers of subsidiaries, as it is a WOS.

However, in example 4, if Co. A owns less than 100% in Co B then Co C cannot acquire Co D, as that would violate the restriction as per the rule.

Companies having more than two layers of subsidiaries on or before the date of commencement of this rule need not reduce layers. Instead, such companies should disclose the details of such subsidiaries to the Registrar of Companies in form CRL-1 within 150 days (i.e. 17 February, 2018). They shall not make additional layers of subsidiaries over what existed on 20 September, 2017 and shall not have number of layers beyond the number of layers it has after such reduction or maximum layers allowed, whichever is more, in case one or more layers are reduced by it subsequent to the commencement of these rules.

Contravention of any provision of these rules shall be punishable with fine, which may extend to INR 10,000, and in case of continuing contravention, with a further fine, which may extend to INR 1000 for each day.

While the rule provides exemptions to NBFC and other regulated financial entities and disregards one layer of WOS, providing some relief; however, given the above restrictions, groups with various shell companies may consider mergers or winding up such companies in order to float one or more new operating companies.

There is also additional relief in the form of proposed amendment to section 2(87), defining subsidiary. The amendment proposes that a company will be treated as a subsidiary in case the holding company exercises or controls more than 50 percent of the total voting power instead of the total share capital. Therefore, if a company invests in other companies such that it does not hold any voting power, it would be beyond the purview of this rule. This may provide structuring ability to groups. However, this being just a proposal, its fate remains unknown.

This rule by simplifying corporate structure, aids in keeping a check on rotation and siphoning of funds, and therefore is a welcome step in the direction of improved corporate governance.

Views are personal to author. The article includes inputs from Siddhi Udani – Manager, M&A Tax, PwC India and Dhwani Sanghavi – Associate, M&A Tax, PwC India

Author Bio

How different is this amendment from section 186(1)?