I. Introduction: –

In general, Dividend refers to the share of the profits of a company that is distributed amongst its members. Dividend is a return on the investment made in the share capital of a company, as distinct from the return on borrowed capital, which is in the form of interest.

Chapter VIII of Companies Act, 2013, i.e., Declaration and Payment of Dividend, a recommendatory Secretarial Standard 3, i.e., Secretarial Standard on Dividend covers the provisions of dividend. Listed companies need to comply with regulations of SEBI (Listing Obligations and Disclosure Requirements), 2015 and Securities Contracts (Regulation) Act, 1956. Any specific provision relating to Dividend in the Income tax Act, 1961 or under any other statue shall also be applicable.

Section 2(35) of the Companies Act, 2013 defines dividend as “dividend includes any interim dividend.”

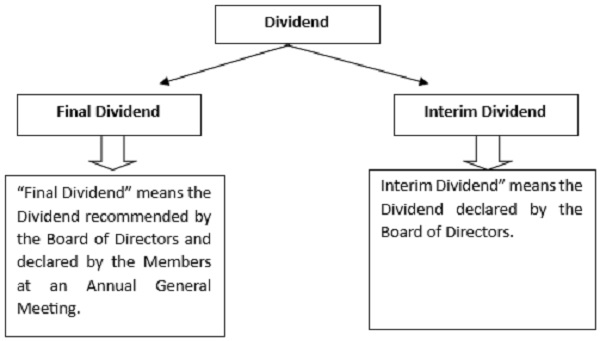

Secretarial Standard 3 Defines Final and interim dividend as follows: –

Companies licensed under Section 8 of the Companies Act, 2013 or corresponding provisions of any previous enactment thereof are prohibited by their constitution from paying any Dividend to its Members.

II. Section 123 of Companies Act, 2013- Declaration of Dividend and Rule 3 of Companies (Declaration and Payment of Dividend), Rules 2014.

| Sections | Content | Explanations/Proviso |

| Section 123(1)(a) | A company can declare and pay dividend for any financial year only out of –

|

Proviso:- In computing profits any amount representing unrealised gains, notional gains or revaluation of assets and any change in carrying amount of an asset or of a liability on measurement of the asset or the liability at fair value shall be excluded. |

| Section 123(1)(b) | No dividend shall be declared or paid by a company for any financial year except—

out of money provided by the Central Government or a State Government for the payment of dividend by the company in pursuance of a guarantee given by that Government. |

Proviso- I– A company may, before the declaration of any dividend in any financial year, transfer such percentage of its profits for that financial year as it may consider appropriate to the reserves of the company.

Proviso II:– In case of inadequacy or absence of profits in any financial year, any company proposes to declare dividend out of the accumulated profits earned by it in previous years and 7[transferred by the company to the free reserves], such declaration of dividend shall not be made except in accordance with such rules as may be prescribed in this behalf. Proviso III:- No dividend shall be declared or paid by a company from its reserves other than free reserves. Proviso IV:– No company shall declare dividend unless carried over previous losses and depreciation not provided in previous year or years are set off against profit of the company for the current year. |

| Rule 3:- Declaration of Dividend Out of Reserves | In the event of inadequacy or absence of profits in any year, a company may declare dividend out of free reserves subject to the fulfilment of the following conditions, namely: –

(1) The rate of dividend declared shall not exceed the average of the rates at which dividend was declared by it in the three years immediately preceding that year. (2) The total amount to be drawn from such accumulated profits shall not exceed one-tenth of the sum of its paid-up share capital and free reserves as appearing in the latest audited financial statement. (3) The amount so drawn shall first be utilised to set off the losses incurred in the financial year in which dividend is declared before any dividend in respect of equity shares is declared. (4) The balance of reserves after such withdrawal shall not fall below fifteen per cent of its paid up share capital as appearing in the latest audited financial statement. |

Proviso to Rule 3(1): – This sub-rule shall not apply to a company, which has not declared any dividend in each of the three preceding financial year. |

| Section 123(2) | For the purposes of clause (a) of sub-section (1), depreciation shall be provided in accordance with the provisions of Schedule II. | – |

| Section 123(3) | The Board of Directors of a company may declare interim dividend during any financial year or at any time during the period from closure of financial year till holding of the annual general meeting out of the surplus in the profit and loss account or out of profits of the financial year for which such interim dividend is sought to be declared or out of profits generated in the financial year till the quarter preceding the date of declaration of the interim dividend | Proviso:- In case the company has incurred loss during the current financial year up to the end of the quarter immediately preceding the date of declaration of interim dividend, such interim dividend shall not be declared at a rate higher than the average dividends declared by the company during the immediately preceding three financial years. |

| Section 123 (4) | The amount of the dividend, including interim dividend, shall be deposited in a scheduled bank in a separate account within five days from the date of declaration of such dividend. | |

| Section 123( 5) | No dividend shall be paid by a company in respect of any share therein except to the registered shareholder of such share or to his order or to his banker and shall not be payable except in cash | Proviso I: – Nothing in this sub-section shall be deemed to prohibit the capitalisation of profits or reserves of a company for the purpose of issuing fully paid-up bonus shares or paying up any amount for the time being unpaid on any shares held by the members of the company.

Proviso II:- any dividend payable in cash may be paid by cheque or warrant or in any electronic mode to the shareholder entitled to the payment of the dividend. |

| Section 123 (6) | A company which fails to comply with the provisions of sections 73 and 74 shall not, so long as such failure continues, declare any dividend on its equity shares. | Explanation: – Section 73 refers to Prohibition on acceptance of deposit from public and Section 74 refers to Repayment of deposit, etc. |

III. As per secretarial standard 3- there are following restrictions/conditions on declaration of dividend: –

> A company shall also not declare any Dividend, if it has defaulted in –

(a) Redemption of debentures or payment of interest thereon or creation of debenture redemption reserve,

(b) Redemption of preference shares or creation of capital redemption reserve,

(c) Payment of Dividend declared in the current or previous financial year(s), or

(d) Repayment of any term loan to a bank or financial institution or interest thereon, till such time the default is subsisting.

No Dividend shall be declared by the company during the extended time, if any, granted by the Tribunal/Court for repayment of above liabilities.

> Dividend shall not be declared out of the Securities Premium Account or the Capital Redemption Reserve or Revaluation Reserve or Amalgamation Reserve or out of profits on re-issue of forfeited shares or out of profits earned prior to incorporation of the company

Where a company has issued equity shares with differential rights as to Dividend, Interim Dividend may, at the option of the Board, be declared on all or any one or more of the classes of such shares in accordance with the terms of issue

IV. Payment of Dividend:-

√ Dividend shall be deposited in a separate bank account within five days from the date of declaration and shall be paid within thirty days of declaration. The intervening holidays, if any, falling during such period shall be included.

√ Taxes as applicable on distribution of Dividend shall be paid by the company within the prescribed time.

√ Dividend shall be paid in cash and not in kind.

√ Initial validity of the Dividend cheque or warrant shall be for three months.

√ No Dividend shall bear interest against the company except in case of default in payment of Dividend or despatch of Dividend warrant/cheque within the prescribed period.

√ Section 127 of Companies Act, 2013 provides for Punishment for failure to distribute dividends which states as follows:-

√ Where a dividend has been declared by a company but has not been paid or the warrant in respect thereof has not been posted within thirty days from the date of declaration to any shareholder entitled to the payment of the dividend, every director of the company shall, if he is knowingly a party to the default, be punishable with imprisonment which may extend to two years and with fine which shall not be less than one thousand rupees for every day during which such default continues and the company shall be liable to pay simple interest at the rate of eighteen per cent. per annum during the period for which such default continues

However, no default shall be deemed to have been committed, if –

(a) the Dividend could not be paid by reason of the operation of any law;

(b) a Shareholder has given directions to the company regarding the payment of Dividend and those directions cannot be complied with and the same has been communicated to the concerned Shareholder;

(c) there is a dispute regarding the right to receive the Dividend;

(d) the Dividend has been lawfully adjusted by the company against any sum due to it from the Shareholder; or

(e) for any other reason, the failure to pay the Dividend or to post the cheque or warrant within the prescribed period was not due to any default on the part of the company.

V. Section 124 of the Companies Act, 2013 – Unpaid Dividend Account

The amount of Dividend which remains unpaid or unclaimed after thirty days from the date of its declaration shall be transferred to a special bank account titled as ‘Unpaid Dividend Account’ to be opened by the company in that behalf with any scheduled bank. Such transfer shall be made within seven days from the date of expiry of the thirty days period from the date of declaration of Dividend.

Any amount in the Unpaid Dividend Account of the company which remains unpaid or unclaimed for a period of seven years from the date of transfer of such amount to the Unpaid Dividend Account, along with interest accrued, if any, shall be transferred to the Investor Education and Protection Fund.

Before transferring any unclaimed or unpaid Dividend to the Investor Education and Protection Fund, the company shall give an individual intimation to the Members in respect of whom such unclaimed Dividend is being transferred, at least three months before the due date of such transfer.

Any interest earned on the Unpaid Dividend Account shall also be transferred to the Investor Education and Protection Fund.

All shares in respect of which Dividend has not been paid or claimed for seven consecutive years or more shall be transferred by the company in the name of Investor Education and Protection Fund.

VI. Additional Compliances for listed companies to declare dividend

A Listed Company shall conform to the following:

(i) The equity shares allotted by the company shall rank pari passu with the existing equity shares for the purpose of payment of Dividend, if the same are in existence as on the record date/ book closure.

(ii) The company shall not issue shares in any manner which may confer on any person, superior rights as to voting or Dividend vis-à-vis the rights on equity shares that are already listed.

(iii) The company shall give prior intimation to the Stock Exchange(s) about the Board Meeting in which Dividend is proposed to be recommended / declared, at least two working days in advance excluding the date of the meeting and the date of the intimation.

(iv) The company shall intimate the Stock Exchange(s), the record date fixed for the purpose of payment of Dividend at least seven working days in advance excluding the date of the intimation and the record date.

(v) The company shall recommend or declare Dividend at least five working days before the record date fixed for the purpose. The said period of five working days is excluding the date of declaration/recommendation of Dividend and the record date fixed for the purpose.

The company shall disclose the outcome of the Board Meeting held to consider the Dividend matters, to the Stock Exchange(s) within 30 minutes of closure of the meeting. In case of recommendation / declaration of Dividend, the intimation shall also include the date on which such Dividend shall be paid or Dividend warrant shall be despatched

Provided that in case the meeting of the board of directors closes after normal trading hours of that day but more than three hours before the beginning of the normal trading hours of the next trading day, the listed entity shall disclose the decision pertaining to the event or information, within three hours from the closure of the board meeting.

(vi) In case of payment of Dividend through warrant or cheque payable at par, if the amount of Dividend exceeds one thousand and five hundred rupees, the company shall despatch such Dividend warrant or cheque by speed post to the concerned Member at the registered address.

(vii) The company shall declare and disclose Dividend on per share basis only.

(viii) The company shall not forfeit unclaimed Dividends before the claim becomes barred by law and such forfeiture, if effected, shall be annulled in appropriate cases.

(ix) Top five hundred Listed Companies based on market capitalisation as on 31st March every financial year, shall formulate a Dividend Distribution Policy covering the prescribed parameters by Securities and Exchange Board of India (SEBI). Such policy shall be disclosed in the Annual Report of the company and also be placed on its website.

(x) The company shall disclose in its Corporate Governance Report the Dividend payment date under the General Shareholder Information Section.

Author Bio