On October 21, 2024, the National Financial Reporting Authority (NFRA) issued Order No. 24/2024, which addressed the professional conduct of Chartered Accountant Chirag Doshi regarding the statutory audit of Ushdev International Limited (UIL) for the financial year 2017-18. The order was a resolution to a Show Cause Notice (SCN) issued on October 13, 2023. The NFRA, acting under Section 132(4) of the Companies Act, 2013, conducted a suo motu examination of Doshi’s actions during the audit. The NFRA found significant lapses in Doshi’s duties, including a failure to report fraud, inadequate audit evidence for valuation, and non-compliance with auditing standards.

The NFRA highlighted that Doshi issued a Disclaimer of Opinion on both the financial statements and the internal financial controls over financial reporting. However, he was found to be grossly negligent in fulfilling his responsibilities, particularly regarding indicators of fraud. He relied excessively on a valuation report provided by management without adequately challenging the assumptions or conducting independent assessments, despite the report’s lack of due diligence. Additionally, the order identified deficiencies in the audit working papers, including unverified signatures and the lack of necessary independence declarations from individuals involved in the audit.

The NFRA’s investigation stemmed from a complaint regarding UIL’s alleged fraudulent activities, including manipulation of financial statements to secure bank loans, which led to the company’s insolvency proceedings. The findings of the Central Bureau of Investigation (CBI) indicated that UIL had engaged in fraudulent practices amounting to substantial financial losses, highlighting the importance of auditors maintaining rigorous standards of diligence and ethical conduct. The NFRA’s examination of the audit files confirmed prima facie violations of the auditing standards and the Companies Act, leading to the issuance of the SCN.

After considering Doshi’s responses and providing him an opportunity for a personal hearing, the NFRA found him guilty of professional misconduct. Consequently, a monetary penalty of ₹5,00,000 was imposed. The NFRA underscored that a Disclaimer of Opinion does not exempt auditors from their statutory obligations, emphasizing that they must still report any fraud or misconduct encountered during audits.

Government of India

National Financial Reporting Authority

*****

7th Floor, Hindustan Times House,

Kasturba Gandhi Marg, New Delhi

Order No. 24/2024 | Date: 21.10.2024

In the matter of CA Chirag Doshi (ICAI Membership No 119079) under Section 132(4) of the Companies Act 2013 read with Rule 11(6) of National Financial Reporting Authority Rules 2018.

1. This Order disposes of the Show Cause Notice (‘SCN’ hereafter) dated 13.10.2023, issued to CA Chirag Doshi (‘ Auditor’ or ‘EP’ hereinafter). CA Chirag Doshi is a Member of the Institute of Chartered Accountants of India (‘ICAI’ hereafter) and was the Engagement Partner (‘EP’ hereafter) for the Statutory Audit of Ushdev International Limited, Mumbai (‘UIL’ or ‘the Company’ hereafter) for the Financial Year (‘FY’ hereafter) 2017-18.

2. This Order is divided into the following sections:

A. Executive Summary

B. Introduction and Background

C. Lapses in the of Audit

D. Articles of Charges

E. Penalty and Sanctions

3. EXECUTIVE SUMMARY

3. National Financial Reporting Authority (NFRA) is India’s independent regulator in respect of matters relating to accounting and auditing of Public Interest Entities (PIEs).

4. NFRA suo motu examined the professional conduct of the EP, CA Chirag Doshi, for the statutory audit ofUIL for the FY 2017-18, under Section 132(4) of the Companies Act, 2013 (the Act).

5. This Order finds that while the EP issued a Disclaimer of Opinion both on the Financial Statements and on the Internal Financial Controls over Financial Reporting for the FY 2017-18, the EP failed to-

i. Perform his duties with due diligence and displayed gross negligence in relation to his obligations to report fraud under Section 143(12) of the Companies Act, 2013 and SA 2401 despite existence of several indicators of fraud.

ii. Obtain sufficient appropriate audit evidence (SAAE) in the audit of valuation of UIL’s investments in two fellow subsidiaries, namely UIL Singapore Pte Ltd and UIL Hong Kong Ltd and another company, UGFL. The EP relied on the valuation report of the management’s expert without challenging the assumptions and methods and without independently assessing the impairment requirements of these investments, even though the valuation expert had stated that he had not carried out any due diligence, nor had he independently verified the data provided.

iii. Comply with Para 9 of SA 2302 as there were deficiencies in the audit working papers such as lack of authentication by preparer, undated signatures of EP and some working papers prepared by a person who was not member of the ET and who had not even given the independence declaration required of him.

iv. Report the non-compliances with Ind AS 163 which requires that the Financial Statements shall disclose the existence and amounts of restrictions on title, and property, plant and equipment pledged as security for liabilities in respect of the items of PPEs mortgaged with banks for the company’s borrowings.

v. Give proper basis for Disclaimer of Opinion on Internal Financial Control over Financial Reporting (ICOFR) as the Disclaimer of Opinion was based only on the NCLT, Mumbai Bench Order dated 14.05.2018.

6. Based on the proceedings under Section 132(4) of the Companies Act, 2013 and after giving the EP an opportunity to present his case, we find the EP guilty of professional misconduct and impose through this Order, a monetary penalty of Rs.5,00,000/- (Rupees Five Lakhs only) upon CA Chirag Doshi.

B. INTRODUCTION AND BACKGROUND

7. The NFRA is a statutory authority set up under Section 132 of the Act to monitor implementation and enforce compliance of the auditing and accounting standards and to oversee the quality of service of the professions associated with ensuring compliance with such standards. NFRA has the responsibility to protect the public interest, and the interests of the investors, creditors and others associated with the companies or bodies corporate that come under its purview. Under Section 132(4) of the Act, NFRA is vested with the powers of a civil court, and power to investigate the prescribed classes4 of companies and impose penalty for professional or other misconduct of the individual members or firms of chartered accountants.

8. The Statutory Auditors, both individual and firm of chartered accountants, are appointed under Section 139 of the Act. The Statutory Auditors, including the Engagement Partners and the Engagement Team that conducts the audit are bound by the duties and responsibilities prescribed in the Act, the rules made thereunder, the Standards on Auditing (SA hereafter), including the Standards on Quality Control and the Code of Ethics, the violation of which constitutes professional or other misconduct, and is punishable with penalties prescribed under Section 132(4) (c) of the Act, 2013.

9. On receipt of information from CEIB5 vide letter dated 09.09.2022, NFRA started its investigation under Section 132(4) of the Act of possible violations of the SAs by the EP in the statutory audit of UIL, a company located at Mumbai and listed6 on the Bombay Stock Exchange (BSE). The EP took up the audit assignment vide Engagement Letter dated 13. 09.2017. The company went into insolvency proceedings under IBC, 20167 vide NCL T8, Mumbai Bench Order dated 14.05.2018. The EP issued a Disclaimer of Opinion both on the Financial Statements and on the Internal Financial Controls over Financial Reporting (ICOFR) in his audit report dated 25.07.2018.

10. The information sent by CEIB indicated that an FIR dated 05.07.2022 had been registered by Central Bureau of Investigation (CBI) against UIL, based on a complaint from SBI dated 09.12.2020 relating to bank fraud, which involves violation of Companies Act, 2013, manipulation of books of accounts/financials, submission of fake/forged/fabricated Financial Statements before banks to avail credit facilities. According to the FIR, as on June 2015, the total credit facilities given to UIL by a consortium of 15 banks led by SBI stood at Rs.2630 Crores (approx.) which was classified as NPA subsequently. While the company defaulted in its payment obligations to banks, the debtors of the company too defaulted and a provision of Rs.2,859.69 Crore for Expected Credit Loss (ECL) was recognised in the books as on 31.03.2018 on Trade Receivables and Rs.215.36 Crores on Advances given (Other Current Assets). The FIR also alleged that while the company defaulted in India, some overseas entities (TMT Metal Holdings Ltd., UK; Hangi Global Ltd., Virgin Island; UD Trading GP Holding Ltd., Singapore; Mis. Ultravolt Power Pte Ltd., Singapore; Metal Mining Pte Ltd., Singapore; Metal Industrial Pte Ltd., Singapore; M/s. Singapore Slammers) were floated by UILs directors in FY 2017-18. Further, in FY 2017-18, UIL sold goods worth Rs.421 crores (which was outstanding on 31.03.2018) to three other UK based dormant companies-Edenbridge Ltd., Rosscull Ltd. and Culross Mayfair. Though the total turnover of UIL for the FY 2017-18 is shown as Rs. l 03 Crores in the Statement of Profit and Loss, these three entities are appearing in the list of trade receivables in the ageing bracket of 3 66 to 720 days amounting to Rs.431 Crores approx.

‘ . .In some cases, however, the applicable laws and regulations may require auditors to provide opinion or other specific matters, such as effectiveness of internal control, or the consistency of a separate management report with the financial statements. While the SAs include requirements and guidance in relation to such matters to the extent that they are relevant to forming an opinion on the financial statements, the auditor would be required to undertake further work if the auditor had additional responsibilities to provide such opinions …. ‘

11. Vide NFRA letter dated 10.11.2022, the Audit Files and other documents for the FY 2017-18 were called for. The audit firm submitted the same on 13.01.2023. UIL has disclosed under the significant accounting policies in its Annual Report for the FY 201718 that the Financial Statements had been prepared in accordance with accounting principles generally accepted in India including Indian Accounting Standards (Ind AS) prescribed under Section 133 of the Companies Act, 2013 read with Rule 3 of the Companies (Indian Accounting Standard) Rules, 2015 and the Companies (Accounting Standards) Amendment Rules, 2016.

12. On examination of the Audit Files and on being satisfied that there were prima facie violations of the SAs and the relevant requirements of the Companies Act, 2013 such that sufficient cause existed to act under sub section (4) of Section 132 of the Act, a SCN was issued to the EP on 13.10.2023 under Section 132 ( 4) of the Act read with Rule 11 of the NFRA Rules 2018. The SCN asked the EP to show cause why action should not be taken against him for professional misconduct in respect of his audit of UIL for FY 2017-18.

13. The reply to the SCN was received vide email and letter dated 29.01.2024. The EP also availed personal hearing, which was held on 01.08.2024 at the office of NFRA, New Delhi. This Order is based on the review of the Financial Statements, the Audit Files, written responses of the EP and submissions made during the personal hearing. Each of the charges in the SCN is analysed and discussed below. However, before these are discussed, a general point raised by EP questioning the rationale for the SCN when he had issued a Disclaimer, must be addressed.

14. While audit of Financial Statements of companies under the Companies Act 2013 is conducted primarily to express an opinion on the Financial Statements by conducting the audit in accordance with the SAs prescribed u/s 143 (10), the auditor also has other reporting obligations under the Companies Act 2013, for example: –

a. Reporting to MCA in relation to frauds under Section 143 (12)

b. CARO Report under Section 143 (11) which has many additional reporting obligations including matters relating to frauds, related parties, compliance with Companies Act, 2013 provisions regarding loans, investments, guarantees etc., and companies internal audit system and so on.

c. Other reporting obligations under Section 143 (1) (a) to (f) and 143 (3) of the Companies Act, 2013, for example, Independent Auditor’s opinion on adequacy and operating effectiveness of the intemal financial controls under Section 143.

15. In case the auditor disclaims an opinion on the Financial Statements, the auditor has to perform certain obligations as stated below:

‘ . .In some cases, however, the applicable laws and regulations may require auditors to provide opinion or other specific matters, such as effectiveness of internal control, or the consistency of a separate management report with the financial statements. While the SAs include requirements and guidance in relation to such matters to the extent that they are relevant to forming an opinion on the financial statements, the auditor would be required to undertake further work if the auditor had additional responsibilities to provide such opinions …. ‘

16. In case the auditor disclaims an opinion on the Financial Statements, the auditor has to perform certain obligations as stated below:

Even if the auditor has expressed an adverse opinion or disclaimed an opinion on the financial statements, the auditor shall describe in the Basis for Opinion section the reasons for any other matters of which the auditor is aware that would have required a modification to the opinion, and the effects thereof [Para 27 of SA 705 (Revised)].

Therefore, it is evident that a Disclaimer of Opinion in itself cannot be a basis for absolving an auditor of his other statutory responsibility under the Companies Act, 2013. We now proceed to discuss the individual charges in the SCN.

C. LAPSES IN THE AUDIT

C.1. Responsibilities relating to Fraud

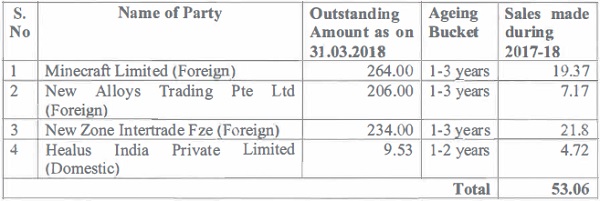

17. The EP was charged with failure to discharge his responsibilities relating to fraud as laid down in SA 240, reporting obligations under Section 143(12) of the Act and CARO10, 2016. It was alleged that the EP failed to examine the sudden and significant increase in the provisions for Expected Credit Loss (ECL) provision on Trade Receivables and on Advances to Vendors. The ECL had increased by 2,583.39% from Rs.106.57 Crores in FY 2016-17 to Rs.2,859.69 Crore in FY 2017-18 Crores; and the provision for doubtful advances to vendors for purchase of steel amounted to Rs.215.36 Crores. There was however no evidence in the Audit File that the EP had carried out existence checking for around 17 major foreign parties against whom Rs.2301 Crores was booked as ECL, accounting for approximately 80% of the total ECL on Trade Receivables booked during FY 2017-18. It was also alleged that fresh sales totalling to Rs.53 Crores approx. were made during the FY 2017-18 to the same parties that were in default for one to three years, but the EP did not question the rationale for the same. The details of such sales are given below:

18. The EP in his reply to the SCN submitted that the provision had been made because the Trade Receivables and advances to vendors for purchase of steel had not been recovered for more than 2 years and there were minimal chances of recovery; that making a provision for the amounts, recovery of which was doubtful, was not a fraud; that the EP in his professional judgement concluded that there was no fraud risk while performing risk of material misstatement; that had the management not recorded the provision, the Financial Statements would have been materially misstated; that only the provision was made during the FY 2017-18 and the same had not been written off; and that the transactions relating to these receivables and advances pertained to prior years and had been subjected to statutory audit, wherein no fraud had been reported in audit reports of prior years’ audited by the predecessor auditors.

19. It is to be noted that UIL had working capital facilities, availed from a consortium of public and private banks of Rs.2416 Crores approx. as on 31.03.2018, which along with interest of Rs.293 Crores approx., was overdue on 31.3.2018, and had been classified as NonPerforming Assets by the banks. These facts are disclosed in the Financial Statements of the company for the FY 2017-18. The EP ignored the fact that the company had defaulted on the payment of loans from the banks and yet sold goods on credit basis to parties who had defaulted in making payments for the earlier sales. Such transactions should have aroused suspicion in a professionally skeptic auditor to identify whether there was any potential fraud being committed by the company through its borrowings from banks and/or credit sales, especially when the EP knew that the company was already under the CIRP when the audit was in progress.

20. The argument of the EP that the amounts of Trade Receivables were only provided for and not written off and therefore there was no trigger for having suspicion of fraud being committed is not acceptable as the amounts were pending for 1-3 years, and the company was already under CIRP11, raising doubts about chances of their recovery. The EP, without exercising necessary professional skepticism, chose the easy option of giving a disclaimer on the Trade Receivables and the related ECL without examining the same from fraud angle. The argument of the EP that the transactions for the Trade Receivables and Advances pertain to prior years and had been subjected to statutory audit wherein no fraud was reported by the predecessor auditors is not acceptable as the EP’s responsibilities on reporting of fraud under Section 143(12) covers the frauds being committed or already committed.

21. As regards the charge that the EP failed to verify the existence of 17 major foreign parties accounting for 80% of the total ECL on Trade Receivables, the EP submitted that he had carried out procedures viz., balance confirmation of major parties, background search of parties and had reviewed the follow-up actions taken by the company viz., letters/ emails sent, and documents of legal actions taken by the company. However, we did not find sufficient evidence in the Audit File to show that the EP had done even the existence checking for the 17 major foreign parties. Considering that these 17 major foreign parties constituted approximately 80% of the total ECL provision on Trade Receivables for the FY 2017-18, the EP ought to have shown skepticism and should have ascertained at least the existence of such foreign parties in order to rule out fraud.

22. As regards the charge regarding fresh sales of Rs.53 Crores made during FY 2017-18 to the defaulting parties, which was another red flag indicating possible fraud, the EP only stated that there were certain collections during the year from such parties, without giving any details. However, the EP remained silent on the rationale for fresh sales ofRs.53 Crores during FY 2017-18 to the defaulting parties and whether he had taken up the issue with the management or Those Charged with Governance. There is no evidence in the Audit File to show that collections were being received, as stated by the EP. We find that the EP failed to sufficiently question these transactions to rule out possible fraud, thereby showing lack of due diligence and gross negligence.

23. We find that issuing a Disclaimer of Opinion in respect of Trade Receivables, Advances given and ECL provision made, ignoring indicators of potential frauds, does not absolve the EP of his duties to report fraud under Section 143(12) of the Act, and show professional skepticism and due diligence. Despite clear indicators such as the substantial rise in ECL provision, default on loans taken from banks, fresh credit sales to defaulting parties and the ongoing insolvency proceedings, the EP failed to consider the requirement of reporting fraud under Section 143(12) of the Companies Act, 2013 and CARO, 2016. There is no evidence in the Audit File to show that the EP even examined this issue from a potential fraud angle. We, therefore, find the EP to be grossly negligent in his duties relating to SA 240 and having failed to discharge his statutory obligations under Section 143(12) of the Act and CARO, 2016.

24. In similar case, the US regulator, PCAOB, in the matter of Wander Rodrigues Teles12, censured Teles, barred him from being an associated person of a registered public accounting firm and imposed a civil money penalty of $10,000. The Board imposed these sanctions on the basis of its findings that Teles violated PCAOB rules and standards inter alia in testing net accounts receivable which was identified as areas having increased risks of material misstatement, including a risk of fraud.

C.2 Audit Evidence – SA 500

C.2(a) Management Expert’s work pertaining to Non-Current Investments

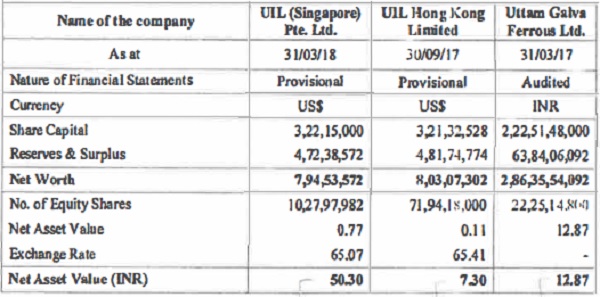

25. The SCN charged the EP with failure to comply with Para 6 of SA 50013 which requires the auditor to design and perform audit procedures that are appropriate in the circumstances for the purpose of obtaining sufficient appropriate audit evidence in respect of evaluation of UIL’s investments in two fellow subsidiaries namely, UIL Singapore Pte Ltd. and UIL Hong Kong Ltd. and another entity named Uttam Galva Ferrous Ltd. UIL had invested Rs.66.26 Crores in these three entities which accounted for approximately 8% of its Balance Sheet size as on 31.03.2018. The EP was charged for not evaluating whether the management’s expert14 who prepared the report on valuation of investments, had appropriate and adequate expertise in the domain of fair valuation; and for relying on valuation report and the assumptions and method used without questioning the same. The EP was also charged for not evaluating whether there was any requirement for impairment in the investment made by UIL in these companies.

26. The EP replied that the management’s expert was a Registered Valuer and had expertise in business consultancy which the EP stated included the valuation related expertise; that the A WP also documents that the audit firm (of the management’s expert) offered services of business consultancy, however, there is no document supporting the valuation related expertise of the management’s expert, CA Vivek Newatia. In respect of valuation of investments in UIL Singapore Pte Ltd. and UIL Hongkong Ltd., the EP replied that since both companies were engaged in trading activities, the future profitability could not be estimated with reliability, hence, the asset-based approach was considered as the most suitable method of valuation. As regards UGFL, the EP stated that the asset-based approach was used as the company did not have any concrete business plans and was at a nascent stage, the Enterprise Value (EV) to EBITDA multiple cannot be used. Moreover, the priceto-earnings (PE) multiple could not be used since the company did not have any income in the previous year.

27. We find from the copy of the valuation report that the management expert had added the following disclaimer in his report:

‘In the course of valuation, we were provided with both written and verbal information. We have however, evaluated the information provided to us by the Company through broad inquiry, ana~vsis and review, but have not carried out a due diligence or audit of the Companv for the purpose of this engagement, nor have we independently investigated or otherwise verified data provided. The terms of our engagement were such that we were entitled to rely upon the information provided by the Company without detailed inquiry. Also, we have been given to understand by the Management that they have not omitted any relevant material factors and, that they have checked out relevance or materiality of any specific information to the present exercise with us. Our conclusions are based on these assumptions, forecasts and other information given by/on behalf of the Company. Accordingly. We do not express any opinion or offer any form of assurance regarding its accuracy and completeness. We do not accept any liability to any third party in relation to the issue of this report. Neither the report nor its contents may be referred to or quoted in any other agreement or documents given to third parties without our prior written consent. We retain the right to deny permission for the same.

28. The declaration by the valuation expert that he relied completely on the information provided by the management and did not carry out a due diligence or audit of the company for the purpose of this engagement was not questioned by the EP, pointing to gross negligence and absence of due diligence on EP’s part.

29. The management’s expert included in the report a table giving details of the share capital and reserves & surplus, an extract of which is placed below:

‘ We have used the data as per the latest available financial statements of the companies for the purpose of relative valuation of their equity shares.

On the basis of such working the relative fair value per share of the companies on the Valuation Date-

(i) M/s UILSPL- Rs.50.30 per share

(ii) M/s UILHKL-Rs. 7.30 per share

(iii) M/s UGFL-Rs. I 2. 87 per share. ‘

30. As can be seen from the above, management’s expert performed the valuation on the basis of the net worth figure without any evidence whether he had done sufficient work in performed and the date and extent of such review. The deficiencies noted in the Audit Working Paper included: no authentication by preparer, no date affixed by EP with his signature and authentication by person who was not a member of the ET. The role of EP in reviewing the working papers is not evidenced in the Audit Working Papers as they do not have the authentication by the EP. Further, in view of the fact that audit documentation was prepared by a person who was not a member (Hitesh Sevada) of the ET for 2017-18, the integrity of the Audit File is questionable and also indicated possible tampering before submission to NFRA.

35. The EP submitted that the A WPs have been prepared, compiled and documented with due diligence as mentioned in Para 9 of SA 230. However, inadvertently in some cases the preparers had missed the sign off. All these documents were reviewed by the audit manager, who provided his sign off on all such documents.

36. The EP further referred to Para A1816 of SA 220 Quality Control for an Audit of Financial Statements and stated that as required by SA 220, the EP had reviewed the working papers related to critical areas of judgement and significant risk. The EP submitted that he had inadvertently missed mentioning the review date while signing off a few of the A WPs, and accordingly, submitted that he was in compliance with the requirements of Para 9 of SA 230. The EP also submitted that FY 2017-18 was the first year of their engagement and he was involved right from the beginning i.e., acceptance of client to the conclusion phase of the audit engagement; that though Hitesh Sevada was not the initial member of ET, he was temporarily engaged and since his involvement was very limited, his name was not listed in the list of ET members; that the audit files submitted to NFRA were not tampered with and integrity of the same is not questionable.

37. We find that the absence of authentication by the preparers of the audit documentation and not affixing the date with the signature of the EP is a lapse as it fails to establish who prepared the audit document and when it was reviewed by the EP. As stated above, Para 9 of SA 230 requires the auditor to record who performed the audit work and the date such work was completed; and who reviewed the audit work and the date and extent of such review. We also find that the EP failed to review critical workpapers such as journal entry review and trial balance tracing, fraud risk questionnaire, indicators of fraud (undated signature of EP) etc. Consequently, the EP’s assertion that he complied with Para A18 of SA 220 as the critical areas of judgment were reviewed by him is incorrect. Further, the preparation of working papers by a person (Hitesh Sevada) in respect of whom independence confirmation is also not available in the Audit File, is a serious lapse on part of the EP. We therefore find that the EP violated Para 9 of SA 230.

38. Such lapses are viewed seriously by other regulators also. In its order dated 19.03.2019 in the matter of Bharat Parikh & Associates Chartered Accountants, the US audit regulator PCAOB took a serious view of the lack of sufficient documentation and imposed penalties and sanctions for violations including insufficient documentation. The PCAOB order states that ” … .Audit documentation must contain sufficient information to enable an experienced auditor, having no previous connection with the engagement to: (a) understand the nature, timing, extent, and results of the procedures performed, evidence obtained, and conclusions reached, and (b) determine who performed the work and the date such work was completed as well as the person who reviewed the work and the date of such review………………….. the documentation for each of those audits was insufficient to demonstrate the nature, timing, extent, and results of the procedures performed, evidence obtained, and conclusions reached, including in those areas of the audits involving significant risks. For the FY 2016 and 2017 Issuer A audits, the documentation also failed to demonstrate who performed the work and the date such work was completed. Additionally, in each of the Issuer A and Issuer B audits, the audit documentation was insufficient to demonstrate which aspects of the audit and which audit documentation Bharat Parikh reviewed. ”

39. In another case, the Executive Counsel to the Financial Reporting Council (FRC), the UK Audit Regulator, in the matter pertaining to Deloitte LLP and John Charlton in the audit of Mi tie Group plc. for the year ended 31 March 2016, imposed a financial sanction of Two Million Pounds, a published statement in the form of severe reprimand against Deloitte and a financial sanction of 65,000 Pounds and a published statement in the form of a severe reprimand against Charlton besides other things, for breach of ISA 230 as they failed to adequately document the audit work papers.

C.4 Non-Compliance with Companies Act, 2013

40. The EP was charged with non-compliance with Section 143(3)(e) of the Companies Act, 2013, which requires the auditor to state in his report whether, in his opinion, the Financial Statements comply with the accounting standards. The EP was charged for not reporting the non-compliances by the company with Ind AS 16 and Ind AS 10717.

41. The EP was charged for failure to report that the company did not comply with Para 74(a) of Ind AS 16 which requires that the Financial Statements shall disclose the existence and amounts of restrictions on title, and property, plant and equipment pledged as security for liabilities. The EP replied that the Disclaimer of Opinion in the Financial Statements includes borrowings as well. We have reviewed the EP’s workpapers related to the borrowings, the work paper ‘1822M001 Current Borrowings March 2018’ concludes that the EP was unable to comment on the correctness of the borrowings for want of supporting documents. The work paper also does not discuss the pledge on PPE, nor does it show any efforts by the EP to obtain the details of the restrictions on PPE due to pledge etc. Since these restrictions were known to the EP, as is evident from the valuation reports of the PPE which are part of the Audit File, the BP evidently failed to report non-disclosure of these restrictions in its Financial Statements. Therefore, it is evident that BP failed to exercise due diligence in the audit of the disclosures w.r.t Ind AS 16 Property, Plant and Equipment.

42. The BP was also charged for not pointing out the non-compliances by the company in respect of Para 35 of Ind AS 107 as there are no disclosures in the Financial Statements regarding credit risk exposure of trade receivable i.e., provision matrix used, the loss allowance percentage used and the loss allowance against each past due bucket and other risk evaluation tools. The BP stated that he had given a Disclaimer of Opinion in respect of Trade Receivables and ECL provisioning. Accordingly, we are not proceeding further with the charge.

C.5. Internal Financial Control over Financial Reporting

43. The EP was charged for non-compliance with Section 143(3)(i) of the Companies Act, 2013 for not giving a proper basis for the Disclaimer of Opinion issued on the Internal Financial Control over Financial Reporting (ICoFR). The EP in the Annexure-B to the Independent Auditor’s Report i.e., the report on the Internal Financial Controls for the FY 201 7-18 has mentioned that the disclaimer was based on the fact that the company had not established internal financial controls due to commencement of Corporate Insolvency Resolution Process (CIRP) against the company vide NCLT, Mumbai bench Order dated 14.05.2018. The EP submitted that the CIRP process was initiated in December 2017 and the independent directors resigned in February 2018. The EP submitted that even though the directors contented that proper internal financial controls had been laid down and those controls were adequate and operating effectively, the EP was unable to obtain sufficient appropriate audit evidence regarding the design and operating efficiency of such internal financial controls. However, these facts are not documented in the Audit File.

44. As the basis for Disclaimer of Opinion was only based on NCLT, Mumbai bench Order dated 14.05.2018 and the EP failed to record in the Audit File the facts mentioned above, we find that the basis of Disclaimer of Opinion on Internal Financial Control over Financial Reporting was deficient, and the EP showed gross negligence and lack of due diligence in performing this work.

C.6. Inadequate Disclosures in Statement of Cash Flows

45. The EP was charged with non-compliance with Para 10 and Para 25(a) of SA 31518 which required the auditor to discuss the susceptibility of the entity’s Financial Statements to material misstatement. In the Statement of Cash Flows for FY 2017-18 under the head Cash flows from Investing Activities, the Company had disclosed an amount of Rs.86.16 Crores as cash outflow on account of’Payments for Fixed Assets/Reversal of Fixed Assets’. It was pointed out that this transaction was a non-cash transaction, the disclosure of which in the Cash Flow Statement was erroneous and is not in compliance with the prescriptions oflnd AS ?19.

46. The EP replied that the same was reversal of ‘cash flows from operations’ to ‘cash flows to investment activities’ resulting in off-setting disclosure between operating and investing activities, not affecting the overall cash flow generation disclosed. However, the EP submitted that ET will be more diligent and cautious in future to ensure additional disclosures are made in the Financial Statements.

47. We find that the disclosure was inadequate for the users of the Financial Statements. However, in view of the reply of the EP and his admission to be more cautious in future, we are inclined not to proceed further with the charge.

C.7 Accounting Estimates SA 54020

48. The EP was charged with not reporting non-provisioning for advance of Rs.39.80 Crore under ‘Advance recoverable in cash or kind or for value to be received’. This included an amount of Rs.39.53 Crores due from Windworld (India) Limited which was undergoing voluntary liquidation under IBC, 2016. However, in view of the explanation furnished by the EP that he had given a Disclaimer of Opinion on the recoverability of the loans & advances, we are not proceeding further with this charge.

C.8 Non-Compliances with Other SAs

49. The EP was charged with noncompliance with SA 22021; Para 13 of SA 25022; Para 11, 21 and 22 of SA 26023; Para 25 (b) of SA 315; Para 7 and 11 of SA 53024 and Para 13(a) of SA 55025. However, based on the Disclaimer of Opinion, the written reply of the EP and submissions made during the personal hearing held on 01.08.2024, we are not proceeding further with the charges.

D. ARTICLES OF CHARGES

50. Based on the detailed analysis and discussion above, we conclude that even though the EP has issued a Disclaimer of Opinion, he failed to exercise due diligence and displayed gross negligence in failure to adequately address the risks related to fraud, disclosures requirements and deficiencies in audit documentation and make appropriate reports under Section 143(12).

51. Based on the foregoing discussion and analysis, we conclude that the EP has committed professional misconduct as defined in Section 132 (4) of the Companies Act, read with Section 22 the Chartered Accountants Act 1949 (the CA Act), as amended from time to time, as detailed below:

a. The EP committed professional misconduct by not exercising due diligence and being grossly negligent in the conduct of his professional duties. (refer to Clause 7 of Part I of the Second Schedule of the CA Act). This charge is proved as explained in Section C.l, C.2(a), C.3, C.4 and C.5 above.

b. The EP committed professional misconduct by failing to invite attention to any material departure from the generally accepted procedure of audit applicable to the audit engagement (refer to Clause 9 of Part I of the Second Schedule of the CA Act). This charge is proved as explained in Section CJ, C.2(a) and C.3 above.

E. PENAL TY AND SANCTIONS

52. Section 132(4) of the Companies Act, 2013 provides for penalties in a case where professional misconduct is proved. The seriousness with which proved cases of professional misconduct are viewed is evident from the fact that a minimum punishment is laid down by the law.

53. Absent a robust system of auditing, investors, creditors and other users of Financial Statements would be handicapped and their interest compromised. The best of systems fails if the professionals implementing the system do not perform their job. This could lead to a serious failure of the financial system which could ultimately result in a breakdown in trust and confidence of investors and the public at large.

54. The EP in the present case was required to ensure compliance with SAs and requirements of the Act to achieve the necessary audit quality and lend credibility to Financial Statements to facilitate its users. As detailed in this Order, inspite of issuing a Disclaimer of Opinion, deficiencies in the audit on the part of CA Chirag Doshi establishes his professional misconduct. Despite being a qualified professional, CA Chirag Doshi has not adhered to the Standards and requirements of the Act and has thus not discharged the duty cast upon him.

55. As per information provided by the auditor, CA Chirag Doshi received a remuneration of Rs…………. and a share of profit of Rs.- for FY 2017-18, however the EP did not receive any specific remuneration from the statutory audit ofUIL for the FY 2017-18.

56. The professional misconduct of CA Chirag Doshi has been detailed in the foregoing paragraphs of this Order. Considering the professional misconducts have been proved and keeping in mind the nature of violations, principles of proportionality and deterrence against future professional misconduct, we, in exercise of powers under Section 132(4)(c) of the Companies Act, 2013, hereby order imposition of monetary penalty of Rs. 5,00,000/(Rupees Five Lakhs only). In light of the judgement of the Hon’ble National Company Law Appellate Tribunal (NCLAT) dated 01.12.202326, we have limited this monetary penalty to Rupees Five Lakhs only since the violations relate to FY 2017-18.

57. This Order will become effective after 30 days from the date of its issue.

Notes-

1 SA 240, The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial Statements

2 SA 230, Audit Documentation

3 Indian Accounting Standard (Ind AS) 16 Property, Plant and Equipment

4 As per Rule 3 ofNFRA, 2018

5 Central Economic Intelligence Bureau

6 The secwities ofUIL were suspended from trading from the BSE w.e.f. November 20, 2023

7 Insolvency and Bankruptcy Code, 2016

8 National Company Law Tribunal

9 SA 200, Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with Standards on Auditing.

10 Companies (Auditor’s Report) Order, 2016

11 Corporate Insolvency Resolution Process

12 PCAOB Release No. 105-2017-007 dated March 20, 2017

13 SA 500, Audit Evidence

14 Report on Valuation of Investments by CA Vivek Newatia (ICAI M.no.062636)

15 PCAOB Release No. 105-2015-041 dated December 3, 2015

16 Para Al 8 Of SA 220: Timely reviews of the following by the engagement partner at appropriate stages during the engagement allow significant matters to be resolved on a timely basis to the engagement partner’s satisfaction on or before the date of the auditor’s report: Critical areas of judgment, especially those relating to difficult or contentious matters identified during the course of the engagement; Significant risks; and other areas tbe engagement partner considers important. The engagement partner need not review all audit documentation but may do so.

17 Indian Accounting Standard (Ind AS) I 07 Financial Instruments: Disclosures

18 SA 315, Identifying and Assessing the Risks of Material Misstatement Through Understanding the Entity and Its Environment