Even though the companies act, 2013 talks about compounding of offences but the word compounding is defined under the companies act, 2013 and neither was it defined under the companies act, 1956.

The legal meaning of compounding is “to settle a matter by payment of money, in lieu of other liability.”

In terms of a company compounding can be defined as a mechanism to settle the offences committed by the company or any officer in default, by admission of guilt of violation of law, either voluntarily or on a receipt of notice of default or initiation of prosecution and by paying money in lieu of prolonged litigation.

Thus, compounding consist of receipt of compounding fees in return for an agreement not to prosecute one who has committed an offence.

Advantages of Prosecution

- No personal appearance for officer in default, as in case of prosecution for an offence in a criminal court.

- Summary proceeding less time consuming.

- The defaulter can be discharged on payment of composition `fee, which cannot be more than the maximum fine leviable under the relevant provision.

- There cannot be any prosecution after compounding is decided. Ref: P P Varkey vs. STO

- Fees payable on compounding are not treated as penalty, hence no disqualification for Directors.

- No appeal from order of compounding,

Ref: S.Viswanathan vs. State of Kerela

Section 441 of companies act, 2013: compounding of certain offences-

- The section begins with the clause “Notwithstanding anything contained in CrPC, 1973”, since the criteria for compounding under S 320 of CrPC is very different compared with companies act this clause has been added to remove any inconsistencies.

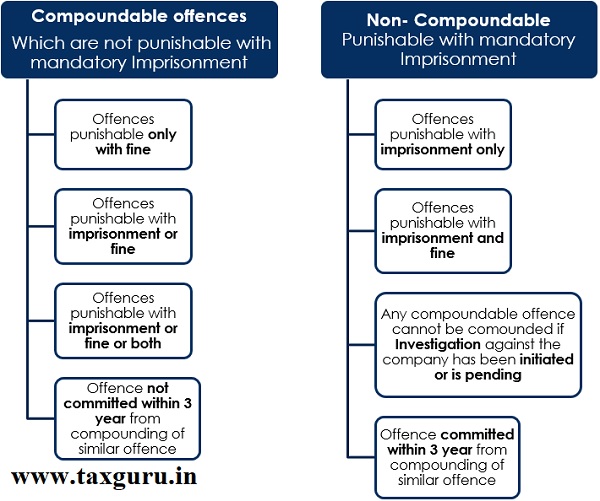

- Offences which can be compounded

According to section 441(1) as amended by the companies (Amendment) ACT, 2017,the following offences can be compounded.

- Permission of Special Court Not required:

Before the Companies (Amendment) Ordinance, 2018, permission of the Special Court was required for compounding of any offence which were punishable under this Act, with imprisonment or fine, or with imprisonment or fine or both. However, with the amendment ordinance, 2018 the requirement of taking permission from special court has been omitted, effective from 02.11. 2018.

- The application of compounding can be filed either before or after the institution of any prosecution. The company or the officer in default can file the application either on suo-moto basis, once it/he becomes aware of the default or can file the application on of the notice or on initiation of prosecution.

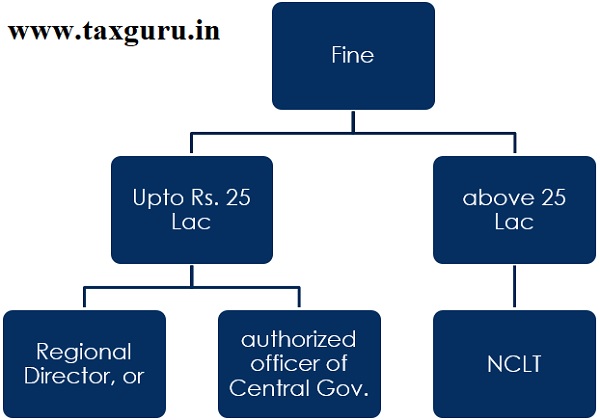

- Power to Compound

Where the maximum amount of fine does not exceed 25lac., the power to compound has been vested with the Regional Director or an authorized officer of the central government.

In any other matter, the power to compound is vested with the NCLT.

The offence is compounded after the company or the officer pays the sum, as specified by the RD or Tribunal, to the central government.

It shall be noted that the sum, specified by the RD or Tribunal, shall not exceed the maximum amount of penalty/ fine for that offence, if such offence was not compounded.

Note: Any compoundable offence shall not be compounded if the investigation, under companies act, 2013, has been initiated or is pending against the company.

- Interval between similar offences for compounding

There shall be an interval of at least 3 years between the date of committing a subsequent offence and the date of compounding of a similar offence which was committed by the company or the officer in the past.

Therefore, any second or subsequent offence committed after the expiry of a period of three years from the date on which the offence was previously compounded, shall be deemed to be a first offence

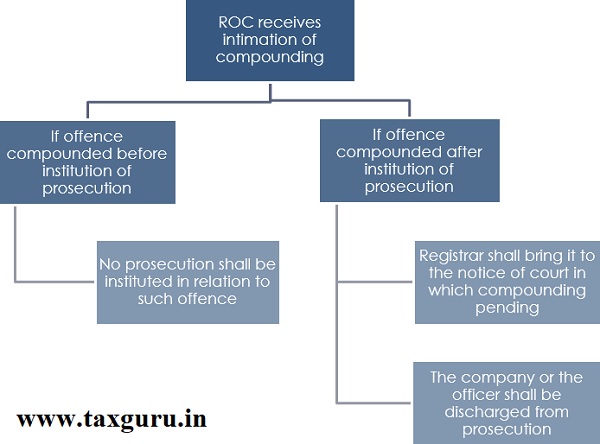

Process of Compounding

The process of compounding is illustrated hereunder:

–

Further, while dealing with the application of compounding regarding non-compliance with any provision of the act which requires filing of any return/document/account, then the NCLT/RD/officer of CG may direct any officer or other employee of the company to file such return/document/account along with the fees and additional fees as per S 403, within the prescribed time.

In case of failure to comply with the order of filing the record/document/account, the officer or other employee who has committed such default shall be punishable with,

Imprisonment up to six months, or

Fine not exceeding one lakh rupees, or

Both.

Application for compounding of offences shall be filed in Form GNL-1, along with the following documents:

- Petition in triplicate.

- Board resolution authorizing the officer to file the application.

- Evidence which reflects that the offence has been made good

- Copies of attested financial statements pertaining to the last three years

- ROC/RD notice (if received).

- Affidavit.

- Other documents based on requirements.

Recently, the Finance minister, Nirmala Sitharaman, in the COVID-19 stimulus package announced that a majority of the compoundable offences would be adjudged internally and the powers of Regional Director for compounding would also be enhanced.

Really helpful