Beyond the accounting sheet, employees are the asset of the organisation and like any asset, your people need to be invested in. Companies offers various benefits to the workers who offer their valuable expertise in the organisation. There is a way of EQUITY COMPENSATION for the employees who give their hard work and perspire for the company.

Company rewards the employees or directors through equity compensation for felicitating their efforts. As equity shares are treated as ownership of companies, employees who get equity shares work harder to increase the profits of the companies which in turn increase the ROI on shares.

Sweat Equity Shares is governed by Section 54 of the Companies Act, 2013 and Rule 8 of Companies (Share capital and debentures) Rules, 2014. The listed companies need to comply the SEBI regulations.

As per Section 2(88) of the Companies Act, 2013 Sweat equity shares means such equity shares as are issued by a company to its directors or employees at a discount or for consideration other than cash, for providing their know-how or making available right in nature of Intellectual Property Rights or value additions, by whatever name called.

Although Section 53 prohibits discount on issue of shares but it provides an exception to section 54. Hence equity shares can be issued to employees or directors at discount or consideration other than cash for their non-monetary contribution for the business.

As Per Section 54 “If a company wishes to issue Sweat Equity share, then it must issue to a class, it has already issued.

Generally, in Indian Context, Companies are allowed to issue two class of equity shares Differential Voting rights Shares (DVRs) and Normal Equity Shares.

Such Companies who are contemplating to issue sweat equity shall issue only of the class of equity which they already issued.

Legal Requirements.

- Issue must be authorized by special resolution passed at general meeting and form MGT-14 has been filed with Registrar within 30 days of passing of Special Resolution ( Complying section 117)

( the resolution specifies the number of shares, the current market price, consideration, if any, and the class or classes of directors or employees to whom such equity shares are to be issued)• The above resolution passed to authorize the board to issue such sweat equity shares, and shall be valid for making the allotment with in period of not more than 12 months from the date of passing of special resolution. - The resolution must contain details of number of shares, their current market price, consideration (if any) and the class of director or employees to whom such equity shares are proposed to be issued.

(Independent Director are eligible to participate in such issue)

- Where the equity shares of the issuing company are listed on a recognized stock exchange, the sweat equity shares of such company shall be issued in accordance with SEBI (Issue of sweat equity) Regulation 2002. However for unlisted company a special resolution passed at general meeting is sufficient enough.

- The rights, limitations, restrictions and provisions which were applicable to equity shares shall be applicable to sweat equity share as well and the holder of such sweat equity shares shall be rank on the same platform (pari passu) with other equity shareholders.

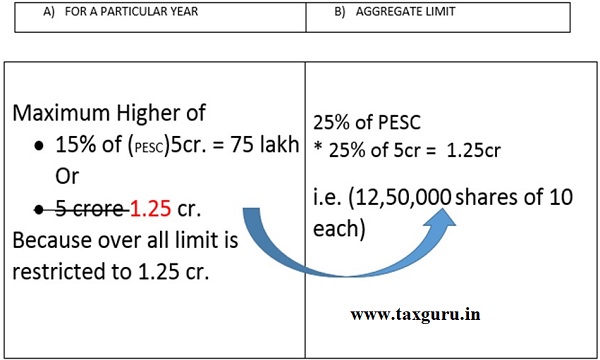

- The company shall not issue sweat equity shares for more than 15% of the existing paid up equity share capital in a year or shares of issue value of Rupees 5 crores. ( whichever is higher)

- The overall issuance of Sweat Equity Shares in the company shall not exceed 25% of the paid up equity capital of the company at any time.

Let’s understand the said provision by taking a practical example (considering the relevant info only)

A company X Ltd. Which is having a paid-up equity share capital of Rupees 5 cr. ( 50 lakh share @ 10 each).

Let’s check maximum limit of sweat equity share that X ltd. Can issue.

- The sweat equity shares issued to directors or employees shall be non-transferable for 3 years from the date of allotment.

- The sweat equity shares proposed to be issued shall be valued at a price determined by the registered-valuer (as defined in section 247) as the fair price giving justification for such valuation.

- A copy of valuation report shall be attached with notice sent to the shareholders.

Key Take Away:

- The Companies Amendment Act, 2017 has removed the one year provision i.e. earlier it was “not less than one year has, at the date of such issue, elapsed since the date on which the company had commenced business.

- An Independent Director is eligible to participate in sweat equity shares however he is not eligible for ESOP scheme.

- The holder of sweat equity share shall be on the same foot where the existing equity share holders are and therefore all the right and restriction shall apply to them as well.

- Class and kind are two different things, reader may refer section 43 as there are only 2 kinds of share.

- Even the limit of a single year is maximum in (case b) as shown above is 5cr. One need to check the overall limit and should ensure the overlapping as shown in example solved above.

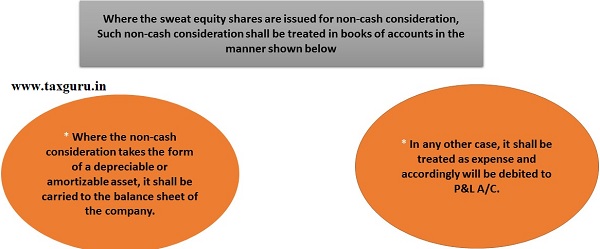

- Non- cash consideration- where bank a/c is not debited in the books of a company for e.g. company has received any award by the director or employee concerned or has given any IPR to the company and the company is issuing sweat equity shares for praising them.

HOWEVER, A STARTUP COMPANY MAY ISSUE SWEAT EQUITY SHARE NOT EXCEEDING 50% OF PAID-UP CAPITAL UP TO 5 YEARS FROM THE DATE OF INCORPORATION OR REGISTRATION.

Disclaimer: The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. Although care has been taken to ensure the accuracy, completeness, and reliability of the information provided, I assume no responsibility, therefore. Users of this information are expected to refer to the relevant existing provisions of applicable Laws. The user of the information agrees that the information is not professional advice and is subject to change without notice. I assume no responsibility for the consequences of the use of such information.

Author Bio