Month: May 2026

2,201 articlesSEBI

SEBI

SEBI Proposes 5% Utilization of IPF Income

SEBI

SEBI

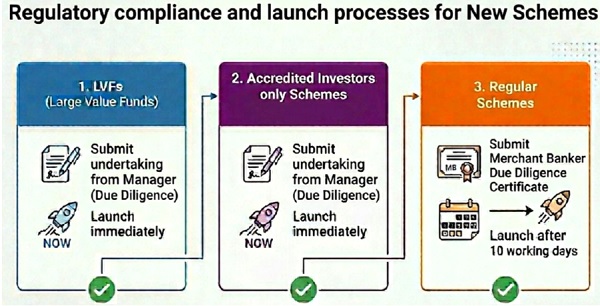

SEBI Proposes Faster AIF Scheme Launches Through GARUDA Mechanism

DGFT

DGFT

DGFT Notifies Agencies Authorised for India-UK CETA Certificates of Origin

Finance

Finance

Authority approves draft IFSCA (Managing General Agents) Regulations, 2026

Income Tax

Income Tax

ITAT Upholds Section 12AB Rejection as Trust Deed Allowed Benefits Outside India

Income Tax

Income Tax

Delhi HC Allows Inspection of Foreign Tax Documents as Fair Cross-Examination Rights Must Be Protected

Income Tax

Income Tax

ITAT Delhi Deletes Section 69A Addition as Sales Were Recorded in Books

Income Tax

Income Tax

ITAT Allows Carry Forward of LTCG Loss as Section 54F Exemption Must Be Applied First

Income Tax

Income Tax

SC Upholds Delay Condonation in Form 10B Filing as Audit Report Was Already Submitted

Service Tax

Service Tax