SEBI (Listing Obligations and Disclosure Requirements) (Sixth Amendment) Regulations, 2021 pertaining to Related Party, Related Party Transactions, Prior Approvals and Disclosures

What is the Change?

On November 09, 2021, Securities and Exchange Board of India (SEBI) vide Notification No. SEBI/LAD-NRO/GN/2021/55 has amended certain provisions relating to :

When will it be effective?

These amendments shall come into effect from April 01, 2022 unless specified that in some provisions which will be effective from April, 01, 2023.

Discussion on Amendments- Related Party Transactions have often been used by the promoters to benefit them or their related parties at the cost of public and other shareholders. SEBI in its attempt to govern RPT keep amending the provisions relating to RPT. These amendments are mostly as per the recommendations of a SEBI Working Group.

DEFINITION

A.1 Related Party [Regulation 2(1) – Clause (zb)]

Existing Definition:

Related Party means a related party as defined u/s 2 (76) of the Companies Act, 2013 or under the applicable Accounting Standard (AS).

Provided that any person or entity belonging to the promoter or promoter group of a listed entity and holding 20% or more of shareholding in the listed entity shall be deemed to be a related party.

Provided further that this definition shall not be applicable for the units issued by mutual funds which are listed on a recognised stock exchanges.

Amended Definition:

Related Party means a related party as defined u/s 2 (76) of the Companies Act, 2013 or under the applicable Accounting Standard (AS). The 1st proviso has been substituted now stating as follows and earlier 1st proviso is now 2nd proviso which has remained unchanged:

First Proviso added

“Provided that:

(a) any person or entity forming a part of the promoter or promoter group of the listed entity;

or

(b) any person or any entity, holding equity shares:

i. of 20% or more; or

ii. of 10% or more, with effect from April 1, 2023;

in the listed entity either directly or on a beneficial interest basis as provided under section 89 of the Companies Act, 2013, at any time, during the immediate preceding financial year;

shall be deemed to be a related party.”

The change:

In the earlier provisions any person or entity can be considered as Related Party if he/ it is belonging to the promoter or promoter group of listed entity and holding 20% or more of shareholding in the listed entity.

However with this amendment any person or entity can be considered as Related Party if he / it is belonging to the promoter or promoter group of listed entity or if any person or entity is holding 20% or more equity shares either directly or on a beneficial interest basis as per Section 89 of the Companies Act, 2013 at any time during preceding Financial Year and Effective from 1st April 2023, if any person or entity is holding 10% or more equity shares

Definition of Related Party has been widened by covering persons or entity through holding of shares either directly or on a beneficial interest basis, even if he/ it is not forming party of promoter or promoter group of listed entity.

Page Contents

A.2.Related Party Transaction [Regulation 2(1)– Clause (zc)]

Existing Definition:

Related Party Transaction means a transfer of resources, services or obligations between a listed entity and a related party, regardless of whether a price is charged and a “transaction” with a related party shall be construed to include a single transaction or a group of transactions in a contract.

Provided that this definition shall not be applicable for the units issued by mutual funds which are listed on a recognised stock exchanges.

Amended Definition:

Regulation 2 (zc) for the definition of Related Party Transaction (“RPT”) is substituted entirely and now it reads as follows:

“related party transaction” means a transaction involving a transfer of resources, services or obligations between:

(i) a listed entity or any of its subsidiaries on one hand and a related party of the listed entity or any of its subsidiaries on the other hand; or

(ii) a listed entity or any of its subsidiaries on one hand, and any other person or entity on the other hand, the purpose and effect of which is to benefit a related party of the listed entity or any of its subsidiaries, with effect from April 1, 2023;

regardless of whether a price is charged and a “transaction” with a related party shall be construed to include a single transaction or a group of transactions in a contract:

Provided that the following shall not be a related party transaction:

(a) the issue of specified securities on a preferential basis, subject to compliance of the requirements under the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2018;

(b) the following corporate actions by the listed entity which are uniformly applicable/ offered to all shareholders in proportion to their shareholding:

i. payment of dividend;

ii. subdivision or consolidation of securities;

iii. issuance of securities by way of a rights issue or a bonus issue; and

iv. buy-back of securities.

(c) acceptance of fixed deposits by banks/Non-Banking Finance Companies at the terms uniformly applicable/offered to all shareholders/public, subject to disclosure of the same along with the disclosure of related party transactions every six months to the stock exchange(s), in the format as specified by the Board:

Provided further that this definition shall not be applicable for the units issued by mutual funds which are listed on a recognized stock exchange(s).

The Change:

Earlier Related Party Transactions covered all transaction of transfer of resources, services or obligation between a listed entity and a related party of the listed entity.

Now the definition of Related Party Transactions is widened and it covers any transaction of transfer of resources, services or obligation between

(a) Listed entity or any of its subsidiaries , with any related party of the listed entity or any of the subsidiaries and

(b) Effective from 01 April 2023 Listed entity or any of its subsidiaries on one hand, and any other person or entity on the other hand, the purpose and effect of which is to benefit a related party of the listed entity or any of its subsidiaries.

Fortunately after many representation by corporate finally SEBI has exempted certain transactions from considering it as RPT , if such transactions are uniformly applicable/offered to all shareholders/public, subject to compliance of the law.

There will be challenge in compliance from 1st April 2023 with respect to identification of any related party transactions where the Purpose and Effect of the transaction will be beneficial to the listed entity or any of its subsidiary. It’s very complex task to find the purpose/ intend and its effect, which benefit to the listed entity or any of its subsidiary. This will be a herculean task for any listed entity as such transactions requires prior approval of the appropriate authority as per these regulation.

B. REGULATION 23– RELATED PARTY TRANSACTIONS

Amendments were made for the following

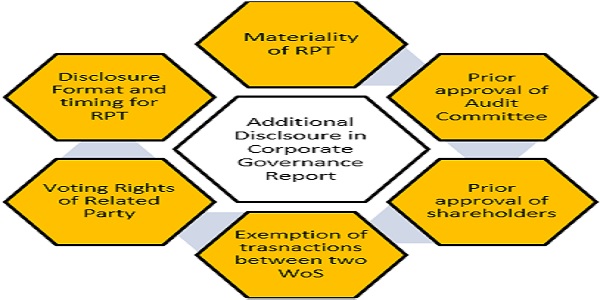

B.1 Material Related Party Transactions [Regulation 23 (1)]:

Explanation for Materiality of Related Party Transaction has been substituted

Earlier Provision:

Earlier any transaction was considered as material during a financial year, if it exceeds 10% of the annual consolidated turnover of the listed entity as per the last audited financial statement of the listed entity

Amended Provision:

Now any transaction is considered as material during a financial year, if it exceeds Rs.1,000 Crores or 10% of the annual consolidated turnover of the listed entity as per the last audited financial statement of the listed entity,, whichever is lower

The Change

The Policy on Materiality of Related Party Transaction need to be amended covering new threshold limit and now many listed entity may have to seek approval of the shareholders.

B.2 Prior Approval of the Audit Committee [Regulation 23(2)]:

Addition and substitution of few word in approval of Audit Committee.

Earlier Provision:

All related party transactions shall require prior approval of the Audit Committee.

Amended Provision:

All related party transactions and subsequent material modification shall require prior approval of the Audit Committee of the listed entity

The Change:

Now any related party transactions and any change in material modification ( which shall be defined by the Audit Committee) shall require prior approval of Audit Committee.

B.3 Prior Approval of the Audit Committee [Regulation 23(2)]:

New proviso is inserted for obtaining prior approval of Audit Committee.

Earlier Provision: Earlier there was no proviso.

Amended Provision: Following new Proviso is added:

Provided further that:

(a) the audit committee of a listed entity shall define “material modifications” and disclose it as part of the policy on materiality of related party transactions and on dealing with related party transactions;

(b) a related party transaction to which the subsidiary of a listed entity is a party but the listed entity is not a party, shall require prior approval of the audit committee of the listed entity if the value of such transaction whether entered into individually or taken together with previous transactions during a financial year exceeds ten per cent of the annual consolidated turnover, as per the last audited financial statements of the listed entity;

(c) with effect from April 1, 2023, a related party transaction to which the subsidiary of a listed entity is a party but the listed entity is not a party, shall require prior approval of the audit committee of the listed entity if the value of such transaction whether entered into individually or taken together with previous transactions during a financial year, exceeds ten per cent of the annual standalone turnover, as per the last audited financial statements of the subsidiary;

(d) prior approval of the audit committee of the listed entity shall not be required for a related party transaction to which the listed subsidiary is a party but the listed entity is not a party, if regulation 23 and sub-regulation (2) of regulation 15 of these regulations are applicable to such listed subsidiary.

Explanation: For related party transactions of unlisted subsidiaries of a listed subsidiary as referred to in (d) above, the prior approval of the audit committee of the listed subsidiary shall suffice.

The Change:

1. Audit Committee of a listed entity to define “Material Modifications” in Related Party Transaction and disclose it as a part of Policy for Related Party Transactions.

2. Even if the listed entity is not a party to Related Party Transaction but its subsidiary is a party, then also Prior Approval of Audit Committee of the listed entity will be required if the value of such transaction ( singly or taken together) in a FY is >10% of annual consolidated turnover, as per audited financial statement of the listed entity

3. Effective from 1st April, 2023, even if the listed entity is not a party to Related Party Transaction but its subsidiary is a party, then also Prior Approval of Audit Committee of the listed entity will be required if the value of such transaction (singly or taken together) in a FY is >10% of annual standalone turnover, as per audited financial statement of the subsidiary.

4. No need to have prior approval of Audit Committee of listed entity for a related party transaction where listed entity is not a party and its listed subsidiary is a party if this regulation 23 and 15 (2) is applicable to such listed subsidiary.

B.4 Prior Approval of Shareholder for Material Related Party Transactions [Regulation 23(4)]:

“Subsequent Material Modification” word is added for obtaining approval of all material related party transaction and a Proviso with explanation is inserted before the existing proviso.

Earlier Provision:

All materials Related Party Transactions will require approval of shareholders of the listed entity.

Amended Provision:

All materials Related Party Transactions and subsequent material modifications as defined by the Audit Committee under sub regulation (2) shall require prior approval of the shareholders through resolution and no related party shall vote to approve such resolutions whether the entity, is a related party to the particular transaction or not.

Provided that prior approval of the shareholders of a listed entity shall not be required for a related party transaction to which the listed subsidiary is a party but the listed entity is not a party, if regulation 23 and sub-regulation (2) of regulation 15 of these regulations are applicable to such listed subsidiary.

Explanation: For related party transactions of unlisted subsidiaries of a listed subsidiary as referred above, the prior approval of the shareholders of the listed subsidiary shall suffice.

The Change:

All material Related Party Transactions required approval of shareholders but now all material Related Party Transactions and subsequent material modifications require PRIOR approval of shareholders.

One relief is granted from obtaining prior approval of the Shareholders of a listed entity for any material related party transaction, if the listed entity is not the party but its listed subsidiary is a party.

B.5. Exemption for certain Related Party Transactions [Regulation 23(5)]

One more exemption is granted for transactions between two wholly owned subsidiary of listed holding company for which no prior approval of Audit Committee, Omnibus approval or shareholders’ approval is required.

Earlier Provision:

Prior approval of Audit Committee and Shareholders’ approval for material RPT shall not be required for Transaction(s) between two Government Companies and Transaction(s) entered into between a Holding Company and its Wholly Owned Subsidiary.

Amended Provision:

No Prior approval of Audit Committee, Omnibus approval or Shareholders’ is required for any related party transactions between two wholly owned subsidiary of listed holding company.

The Change:

One more exemption is given from obtaining any approval of Audit Committee, Omnibus approval or Shareholders’ for any related party transactions between two wholly owned subsidiary of listed holding company.

B.6 Voting Rights: [Regulation 23(7)]

Earlier Provision:

For the purpose of this regulation, all entities falling under the definition of related parties shall not vote to approve the relevant transaction irrespective of whether the entity is a party to the particular transaction or not.

Amended Provision:

This provisions of Regulation 23(7) shall stand omitted.

The Change:

Since the provisions are already covered under Regulation 23 (4) that all materials Related Party Transactions, and now subsequent material modification in related party transaction shall require prior approval of shareholders through resolution and no related party shall vote to approve such resolution whether the entity is related party to the particular transaction or not , hence Regulation 23 (7) is deleted.

B.7 Enhanced Disclosure of RPTs and squeezing of timelines: [Regulation 23(9)]

This provision has been substituted

Earlier Provision:

The listed entity shall submit within 30 days from the date of publication of its standalone and consolidated financial results for the half year, disclosures of related party transactions on a consolidated basis in the format specified in the relevant accounting standards for annual results to the Stock Exchange and publish the same on its website

Amended Provision:

The listed entity shall submit to the stock exchanges disclosures of related party transactions in the format as specified by the Board from time to time, and publish the same on its website.

Provided that a ‘high value debt listed entity’ shall submit such disclosures along with its standalone financial results for the half year:

Provided further that the listed entity shall make such disclosures every six months within fifteen days from the date of publication of its standalone and consolidated financial results:

Provided further that the listed entity shall make such disclosures every six months on the date of publication of its standalone and consolidated financial results with effect from April 1, 2023.

The Change:

1. Earlier the format of disclosure of related party transactions every half year was as specified in the relevant Accounting Standard, however now the format will be as specified by SEBI.

2. Earlier the disclosure of related party transactions to the stock exchange and publication on website to be made in 30 days from the date of publication of its standalone and consolidated financial results for the half year.

Now the same to be disclosed as follows:

(a) High value debt listed entity to disclose related party transactions along with its standalone financial results for the half year

(b) Listed entity to disclose related party transactions every six months within 15 days from the date of publication of its standalone and consolidated financial results

(c) With effect from April 1, 2023, the listed entity to disclose related party transactions every six months on the date of publication of its standalone and consolidated financial results.

C. SCHEDULE II: CORPORATE GOVERNANCE

Part C: Role of the Audit Committee and review of information by Audit Committee:

Para B which is related to mandatory review of documents by Audit Committee, point (2) statement of significant related party transactions (as defined by the shall stand omitted.

D. SCHEDULE V: ANNUAL REPORT

In Para A– Related Party Disclosure,

(a) Point 1 – Listed entity shall make disclosures in compliance with the Accounting Standard on “Related Party Disclosures”. Now amended that listed entity which has listed their non-convertible securities shall make disclosures in compliance with the Accounting Standard on “Related Party Disclosures”.

(b) Point 3 –change in wordings only that the above disclosures of related party shall be applicable to all listed entities except for listed banks now amended that the above disclosures of related party shall not be applicable to listed bank.

In Para C– Corporate Governance Report,

Point 10 – Other Disclosures, one new point (m) is inserted which reads as follows:

(m) Disclosure by listed entity and its subsidiaries of ‘Loans and advances in the nature of loans to firms/companies in which directors are interested by name and amount’:

Provided that this requirement shall be applicable to all listed entities except for listed banks.

E. ACTION REQUIRE

fghfgh

Listed entity need to take following actions:

1. Update Audit Committee members with the proposed changes effective from 1st April 2022 and 1st April 2023.

2. Audit Committee to define “ Material Modification” in Related Party Transaction

3. Amendment to RPT Policy

4. Revise Data base of Related Party with RP of subsidiary(ies)

5. Revise Data base of Related Party Transactions with RPTs of subsidiary(ies) and its value

6. Review all existing RPT which are approved, with value of transaction

7. Review all existing RPT which were earlier not part of RP or RPT

8. Check % of holding of any person or entity directly or indirectly through beneficial holding

9. Check and add in data base, last audited standalone financials of subsidiary company and its annual standalone turnover and threshold limit of 10% of it

10. Check new format of disclosure of RPT which will be specified by SEBI ( earlier it was as per Accounting Standard)

11. Take note of additional disclosure in Corporate Governance Report by listed entity and its subsidiaries of ‘Loans and advances in the nature of loans to firms/companies in which directors are interested by name and amount.

Conclusion:

SEBI has tighten the norms of Related Party Transactions (RPT) and with the change in the definition of Related Party and RPT, many persons/ entities and transaction with them will be under the scanner and governance.

Task of Audit Committee is increased as it has to define “Material Modification”(this term is not defined under the regulation) and reviewing RPTs even if the listed entity is not the party but its subsidiary is the party.

There may be new format prescribed by SEBI for half yearly disclosure of RPT and additional disclosure will be required under Corporate Governance.

It will be most challenging task to find the purpose and effect of any transaction which may benefit a related party of the listed entity or any of its subsidiaries.

*****

Disclaimer*This brief article is not intended for solicitation of any work or advertising. This is of a general nature for knowledge sharing only. This should not be construed as our legal opinion. The views expressed are my personal based on the reading of the Notification issued by SEBI.

Author Bio

Well Explained!