Reserve Bank of India

Monetary Policy Statement, 2023-24 Resolution of the Monetary Policy Committee (MPC) December 6 to 8, 2023

On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (December 8, 2023) decided to:

- Keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 6.50 per cent.

The standing deposit facility (SDF) rate remains unchanged at 6.25 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 6.75 per cent.

- The MPC also decided to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns to the target, while supporting growth.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth.

Assessment and Outlook

2. Global growth is slowing at a divergent pace across economies. Inflation continues to ebb though it remains above target with underlying inflationary pressures staying relatively stubborn. Market sentiments have improved since the last MPC meeting – sovereign bond yields have declined, the US dollar has depreciated, and global equity markets have strengthened. Emerging market economies (EMEs) continue to face volatile capital flows.

3. Domestic economic activity is exhibiting resilience. Real gross domestic product (GDP) grew year-on-year (y-o-y) by 7.6 per cent in Q2:2023-24, underpinned by robust investment and government consumption, which cushioned the drag from net external demand. On the supply side, gross value added (GVA) rose by 7.4 per cent in Q2, driven by buoyant manufacturing and construction activities.

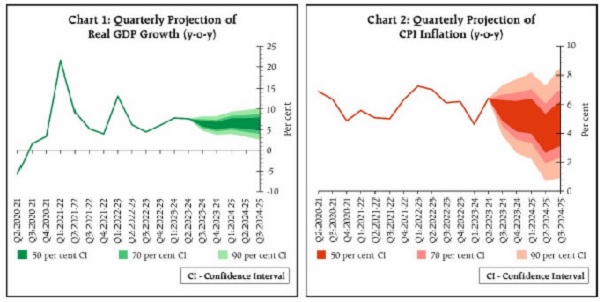

4. Continued strengthening of manufacturing activity, buoyancy in construction, and gradual recovery in the rural sector are expected to brighten the prospects of household consumption. Healthy balance sheets of banks and corporates, supply chain normalisation, improving business optimism, and rise in public and private capex should bolster investment going forward. With improvement in exports, the drag from external demand is expected to moderate. Headwinds from the geopolitical turmoil, volatility in international financial markets and geoeconomic fragmentation pose risks to the outlook. Taking all these factors into consideration, real GDP growth for 2023-24 is projected at 7.0 per cent with Q3 at 6.5 per cent; and Q4 at 6.0 per cent. Real GDP growth for Q1:2024-25 is projected at 6.7 per cent; Q2 at 6.5 per cent; and Q3 at 6.4 per cent (Chart 1). The risks are evenly balanced.

5. CPI headline inflation fell by about 2 percentage points since the last meeting of the MPC to 4.9 per cent in October 2023 on sharp correction in prices of certain vegetables, deflation in fuel and a broad-based moderation in core inflation (CPI inflation excluding food and fuel).

6. Uncertainties in food prices along with unfavourable base effects are likely to lead to a pick-up in headline inflation in November-December. Kharif harvest arrivals and progress in rabi sowing together with El Niño weather conditions need to be monitored. Adequate buffer stocks for cereals and a sharp moderation in international food prices, along with pro-active supply side interventions by the Government may keep these food price pressures under check. Crude oil prices may remain volatile. Early results from the firms polled in the Reserve Bank’s enterprise surveys indicate softer growth in input costs and selling prices for the manufacturing firms in Q4 relative to the previous quarter, while price pressures persist for services and infrastructure firms. Taking into account these factors, CPI inflation is projected at 5.4 per cent for 2023-24, with Q3 at 5.6 per cent; and Q4 at 5.2 per cent. Assuming a normal monsoon next year, CPI inflation for Q1:2024-25 is projected at 5.2 per cent; Q2 at 4.0 per cent; and Q3 at 4.7 per cent (Chart 2). The risks are evenly balanced.

7. The MPC observed that recurring food price shocks are impeding the ongoing disinflation process. Core disinflation has been steady, indicative of the impact of past monetary policy actions. Headline inflation, however, remains volatile, with possible implications for the anchoring of expectations. Domestic food inflation unpredictability, and volatility in crude oil prices and financial markets in an uncertain international environment pose risks to the inflation outlook. The path of disinflation needs to be sustained. The MPC will carefully monitor any signs of generalisation of food price pressures which can fritter away the gains in easing of core inflation. On the growth front, improved momentum in investment demand along with business and consumer optimism, would support domestic economic activity and ease supply constraints. As the cumulative policy repo rate hike is still working its way through the economy, the MPC decided to keep the policy repo rate unchanged at 6.50 per cent in this meeting, but with preparedness to undertake appropriate and timely policy actions, should the situation so warrant. Monetary policy must continue to be actively disinflationary to ensure anchoring of inflation expectations and fuller transmission. The MPC will remain resolute in its commitment to aligning inflation to the target. The MPC also decided to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns to the target, while supporting growth.

8. All members of the MPC – Dr. Shashanka Bhide, Dr. Ashima Goyal, Prof. Jayanth R. Varma, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das – unanimously voted to keep the policy repo rate unchanged at 6.50 per cent.

9. Dr. Shashanka Bhide, Dr. Ashima Goyal, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns to the target, while supporting growth. Prof. Jayanth R. Varma expressed reservations on this part of the resolution.

10. The minutes of the MPC’s meeting will be published on December 22, 2023.

11. The next meeting of the MPC is scheduled during February 6-8, 2024.

(Yogesh Dayal)

Chief General Manager

Press Release: 2023-2024/1438 Date : Dec 08, 2023

*****

Statement on Developmental and Regulatory Policies

This Statement sets out various developmental and regulatory policy measures relating to (i) Financial Markets; (ii) Regulations; and (iii) Payment Systems and Fintech.

I. Financial Markets

1. Review of the regulatory framework for hedging of foreign exchange risks

The regulatory framework governing the hedging of foreign exchange risks was comprehensively reviewed in 2020 with a view to ushering in a principle-based regime. Based on the feedback received from market participants and experience gained since then, the regulatory framework has been made more comprehensive by consolidating the directions in respect of all types of transactions – over-the-counter (OTC) and exchange traded – under a single Master Direction. The framework has also been refined to enhance operational efficiency and ease access to foreign exchange derivatives, especially for users with small exposures. This will also ensure that a broader set of customers with the necessary risk management expertise are given the flexibility to manage their exposures efficiently. The Master Direction will be issued separately.

II. Regulations

2. Framework for Connected Lending

Connected lending or lending to persons who are in a position to control or influence the decision of a lender can be of concern, if the lender does not maintain an arm’s length relationship with such borrowers. Such lending can involve moral hazard issues leading to compromise in pricing and credit management. The extant guidelines on the issue are limited in scope and are not applicable uniformly to all regulated entities. It has accordingly been decided to come out with a unified regulatory framework on connected lending for all the regulated entities of the Reserve Bank. A draft circular in this regard will be issued for public comments.

3. Regulatory Framework for Web-Aggregation of loan products

The Reserve Bank had accepted, vide its Press Release dated August 10, 2022, the recommendation of the Working Group on Digital Lending (Chairman: Shri Jayant Kumar Dash) to come up with a regulatory framework for web-aggregators of loan products (WALP). WALP entails aggregation of loan offers from multiple lenders on an electronic platform which enables the borrowers to compare and choose the best available option to avail loan from one of the available lenders.

Based on the recommendation of the Working Group, it has been decided to bring such loan aggregation services offered by the Lending Service Providers (LSPs) under a comprehensive regulatory framework. The framework will focus on enhancing the transparency in the operations of WALPs, increase customer centricity and enable the borrowers to make informed choices. The detailed guidelines will be issued separately.

III. Payment Systems and Fintech

4. Enhancing UPI transaction limit for Specified Categories

Unified Payments Interface or UPI continues to grow in popularity. The transaction limit for UPI is capped at ₹1 lakh, except a few categories like Capital Markets (AMC, Broking, Mutual Funds, etc.), Collections (Credit card payments, Loan re-payments, EMI), Insurance etc. where the transaction limit is ₹2 lakh. In December 2021, the transaction limit for UPI payments for Retail Direct Scheme and for IPO subscriptions was increased to ₹5 lakh.

To encourage the use of UPI for medical and educational services, it is proposed to enhance the limit for payments to hospitals and educational institutions from ₹1 lakh to ₹5 lakh per transaction. Separate instructions will be issued shortly.

5. e-Mandates for recurring online transactions – Enhancement of limit for specified categories

The framework for processing of e-mandates for recurring transactions was introduced in August 2019 to balance the safety and security of digital transactions with customer convenience. The limits for execution of e-mandates without Additional Factor of Authentication (AFA) currently stands at ₹15,000/- (last updated in June 2022).

The number of e-mandates registered currently stands at 8.5 crore, processing nearly ₹2800 crores of transactions per month. The system has stabilised, but in categories such as subscription to mutual funds, payment of insurance premium and credit card bill payments, where the transaction sizes are more than ₹15,000, a need to enhance the limit has been expressed as adoption has been lagging.

It is, therefore, proposed to exempt the requirement of AFA for transactions up to ₹1 lakh for the following categories, viz., subscription to mutual funds, payment of insurance premium and payments of credit card bills. The other existing requirements such as pre- and post-transaction notifications, opt-out facility for user, etc. shall continue to apply to these transactions. The revised circular will be issued shortly.

6. Establishment of Cloud Facility for the Financial Sector in India

Banks and financial entities are maintaining an ever-increasing volume of data. Many of them are utilising various public and private cloud facilities for this purpose. The Reserve Bank is working on establishing a cloud facility for the financial sector in India. The proposed facility would enhance the security, integrity and privacy of financial sector data. It is also expected to facilitate scalability and business continuity. The cloud facility will be set up and initially operated by Indian Financial Technology & Allied Services (IFTAS), a wholly-owned subsidiary of RBI. Eventually, the cloud facility will be transferred to a separate entity owned by the financial sector participants. This cloud facility is intended to be rolled out in a calibrated fashion in the medium term.

7. Setting up of Fintech Repository

To ensure a resilient FinTech sector and promote best practices, regulators and stakeholders need to have relevant and timely information on FinTech entities, including the nature of their activities. Today, FinTechs are using emerging technologies like Distributed Ledger Technology (DLT), Artificial Intelligence / Machine Learning (AI / ML), and so on. For better understanding of the developments in the FinTech ecosystem with an objective to appropriately support the sector, it is proposed to set-up a Repository for capturing essential information about FinTechs, encompassing their activities, products, technology stack, financial information etc. FinTechs would be encouraged to provide relevant information voluntarily to the Repository which will aid in designing appropriate policy approaches. The Repository will be operationalised by the Reserve Bank Innovation Hub in April 2024 or earlier. Necessary guidelines for this will be issued separately.

(Yogesh Dayal)

Chief General Manager

Press Release: 2023-2024/1439 Date : Dec 08, 2023

****

Governor’s Statement: December 8, 2023

As 2023 comes to an end and a new year begins, the long-awaited normality still eludes the global economy. The years 2020 to 2023 will perhaps go down in history as the period of ‘Great Volatility’, comprising a host of black swan events in quick succession. The global economy is showing signs of slowdown, though unevenly across geographies and sectors. The Emerging Market Economies (EMEs) as a group have remained resilient during the current bout of volatility, unlike previous episodes. While headline inflation has receded from the highs of last year, it remains above target in many countries. Core inflation continues to be sticky, impeding the last mile of disinflation. Major central banks have kept rates on hold while refraining from forward guidance in view of the prevailing uncertainties. Financial markets remain volatile in their quest for definitive signals about the future path of interest rates.

2. Against this unsettled global economic backdrop, the Indian economy presents a picture of resilience and momentum. The real gross domestic product (GDP) growth for Q2 of the current financial year has exceeded all forecasts. The fundamentals of the Indian economy remain strong with banks and corporates showing healthier balance sheets; fiscal consolidation on course; external balance remaining eminently manageable; and forex reserves providing cushion against external shocks. These factors, combined with consumer and business optimism, create congenial conditions for sustained growth of the Indian economy. Looking ahead, it is our endeavour to further build on these fundamentals which are the best buffer against global shocks in today’s uncertain world.

Decisions and Deliberations of the Monetary Policy Committee (MPC)

3. The Monetary Policy Committee (MPC) met on 6th, 7th and 8th December 2023. After a detailed assessment of the evolving macroeconomic and financial developments and the outlook, it decided unanimously to keep the policy repo rate unchanged at 6.50 per cent. Consequently, the standing deposit facility (SDF) rate remains at 6.25 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 6.75 per cent. The MPC also decided by a majority of 5 out of 6 members to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns to the target, while supporting growth.

4. I shall now briefly set out the rationale for these decisions. Since the last policy, CPI headline inflation moderated to 4.9 per cent in October from 7.4 per cent in July. The moderation was observed in all components of CPI – food, fuel and core (CPI excluding food and fuel). There has been broad-based easing in core inflation which is indicative of successful disinflation through monetary policy actions. The near-term outlook, however, is masked by risks to food inflation which might lead to an inflation uptick in November and December. This needs to be watched for second round effects, if any. Domestic economic activity is holding up well as assessed in the previous MPC meetings and as reflected in the Q2:2023-24 GDP growth.

5. Against this backdrop, the MPC decided to keep the policy repo rate unchanged at 6.50 per cent, but remain highly alert and prepared to undertake appropriate policy actions, as warranted. Monetary policy must continue to be actively disinflationary to ensure fuller transmission and anchoring of inflation expectations. The rate action so far is still working its way into the economy. Hence, the MPC decided to remain focused on withdrawal of accommodation to ensure that inflation progressively aligns to the target, while supporting growth.

Assessment of Growth and Inflation

Global Growth

6. The global economy continues to remain fragile. World trade is decelerating amidst global tide of protectionism.1Despite significant restoration of global supply chains,2factors like elevated debt levels, lingering geopolitical hostilities and extreme weather conditions aggravate the risks to global growth and inflation outlook. Easing of inflation in advanced economies has led to expectations of an early end to the monetary tightening cycle, shoring up market sentiments. Sovereign bond yields are softening as markets are not factoring in any further rate hikes.

Domestic Growth

7. Economic activity exhibited buoyancy in Q2 aided by strong domestic demand. GDP posted a robust growth of 7.6 per cent in Q2:2023-24, driven by investment and government consumption.3

8. Turning to Q3, two-third of rabi sowing has been completed despite late harvest of kharif crops in some states.4Manufacturing sector gained strength with easing input cost pressures and pick up in demand conditions.5Eight core industries recorded healthy growth in October and continued their high growth since June this year.6 The purchasing managers’ index (PMI) for manufacturing rose in November.7 The services sector buoyancy has remained intact as reflected in high frequency indicators.8 GST collections at ₹1.68 lakh crore in November 2023 were buoyant.9 Services PMI displayed healthy expansion in November.10

9. On the demand side, households’ consumption is supported by durable urban demand11and gradual turnaround in rural demand as reflected in sales of fast moving consumer goods (FMCG) and other indicators.12Festival related demand is also spurring households’ discretionary consumption in Q3.13 Investment activity continues to be aided by buoyancy in public sector capex.14 This is also reflected in the strong growth in steel consumption, cement production and imports of capital goods.15 Capacity utilisation (CU) in the manufacturing sector continues to remain above the long period average.16 Investments in fixed assets by listed private manufacturing companies also registered healthy growth in H1:2023-24, primarily driven by key industries such as petroleum, steel, chemicals and cement. The total flow of resources to the commercial sector from banks and other sources at ₹17.6 lakh crore during the current financial year so far is significantly higher than that of last year (₹14.5 lakh crore). Despite weakness in external demand, both goods and services exports returned to positive territory in October.17

10. Looking ahead, private consumption should gain support from gradual improvement in rural demand, strengthening of manufacturing activity and continued buoyancy in services. The healthy twin balance sheets of banks and corporates, high capacity utilisation, continuing business optimism and government’s thrust on infrastructure spending should propel private sector capex. The drag from external demand is also expected to moderate with a turnaround in merchandise and services exports. The protracted geopolitical turmoil, volatility in global financial markets and growing geo-economic fragmentations, however, pose risks to the outlook. Taking all these factors into consideration, real GDP growth for 2023-24 is projected at 7.0 per cent with Q3 at 6.5 per cent; and Q4 at 6.0 per cent. Real GDP growth for Q1:2024-25 is projected at 6.7 per cent; Q2 at 6.5 per cent; and Q3 at 6.4 per cent. The risks are evenly balanced.

Inflation

11. Food inflation, which was in double-digits in July, has since then moderated to 6.2 per cent in October with the correction in vegetable prices.18Fuel inflation slipped into deflation since September primarily reflecting the sharp fall in LPG prices in end-August. The disinflation in core gathered momentum during September-October and reached levels last seen during Q4:2019-20 due to the combined effect of policy rate increases and reduction in cost-push pressures across core goods and services.

12. Going ahead, inflation outlook would be considerably influenced by uncertain food prices. High frequency food price indicators point to an increase in prices of key vegetables which may push CPI inflation higher in the near-term. The ongoing rabi sowing progress for key crops like wheat, spices and pulses needs to be closely monitored. Elevated global sugar prices is also a matter of concern.

13. On the positive side, global commodity prices, particularly, agricultural commodity prices, have softened except rice.19For highly import dependent food items like edible oils, international prices continue to remain soft. Domestic milk prices are stabilising. Pro-active supply side interventions by the government are also containing domestic food price pressures. Crude oil has softened considerably, though it may remain volatile. Taking into account these factors and on the assumption of normal monsoons, CPI inflation is projected at 5.4 per cent for 2023-24, with Q3 at 5.6 per cent and Q4 at 5.2 per cent. CPI inflation for Q1:2024-25 is projected at 5.2 per cent; Q2 at 4.0 per cent; and Q3 at 4.7 per cent. The risks are evenly balanced.

What do these Inflation and Growth Conditions mean for Monetary Policy?

14. We have made significant progress in bringing down inflation to below 5 per cent in October 2023 despite occasional blips due to intermittent supply shocks. The summer of 2022 is behind us. Our policy of prioritising inflation over growth, hiking policy rate by 250 basis points in a calibrated manner and draining out excess liquidity have worked well, alongside supply-side measures taken by the government, to bring about this disinflation. The fact that core inflation has also trended lower and household inflation expectations have become better anchored gives us the confidence and conviction that monetary policy is doing its job.20On the other hand, growth remains resilient and robust, surprising everyone on the upside.

15. Notwithstanding this progress, the target of 4.0 per cent CPI is yet to be reached and we have to stay the course. Headline inflation continues to be volatile due to multiple supply side shocks which have become more frequent and intense. The trajectory of food inflation needs to be closely monitored. Intermittent vegetable price shocks could once again push up headline inflation in November and December. While monetary policy would look-through such one-off shocks, it has to stay alert to the risk of such shocks becoming generalised and derailing the ongoing disinflation process. In the midst of these uncertainties, monetary policy has to remain actively disinflationary to ensure a durable alignment of headline inflation to the target rate of 4.0 per cent, while supporting growth.

Liquidity and Financial Market Conditions

16. Like most other central banks, the Reserve Bank had injected additional liquidity into the system to counter the COVID-19 related onslaught on the economy. Consequently, the size of Reserve Bank’s balance sheet had expanded significantly. Persistence of such expanded balance sheet far too long could have created macroeconomic and financial instability. It is worth noting that the Reserve Bank has successfully reduced its balance sheet size well in time. Illustratively, the size of the Reserve Bank’s balance sheet swelled to 28.6 per cent of GDP in 2020-21. With modulation in liquidity in the post COVID period, the balance sheet size moderated to 23.3 per cent of GDP in 2022-23 and further to 21.6 per cent in the current financial year (up to December 1).21We consider this as a significant achievement.

17. System liquidity, as measured by the net position under the liquidity adjustment facility (LAF), turned into deficit mode for the first time in September 2023 after a gap of nearly four and a half years since May 2019. Deficit liquidity conditions persisted during October and November prompting large recourse to the marginal standing facility (MSF) by banks.22In parallel, utilisation of the standing deposit facility (SDF) has also been high.23

18. The overall tightening of liquidity conditions is attributed mainly to higher currency leakage during the festive season, government cash balances and Reserve Bank’s market operations. Driven by these autonomous factors, system liquidity tightened significantly compared to what was envisaged in the October policy statement. Consequently, the need to undertake auction of OMO sales has not arisen so far. The evolution of liquidity conditions has been in alignment with the monetary policy stance. More recently, however, as government spending has picked up and system liquidity has got more evenly balanced among market participants, pressures have eased and the net LAF position has evened out broadly. Going forward, government spending is likely to further ease liquidity conditions. On our part, the Reserve Bank will remain nimble in liquidity management.

19. Different segments of the financial market have witnessed monetary transmission of varying extent. Long-term G-sec yields have softened, reflecting strong demand for these bonds from financial institutions and softening of global bond yields. In the credit market, monetary policy transmission is still working its way through the system.24

20. With regard to the standing facilities of the Reserve Bank under the LAF, we have noticed simultaneous high utilisation of both MSF and SDF by the banks. This was pointed out in the last monetary policy statement. We propose to address this situation and have decided to allow reversal of liquidity facilities under both SDF and MSF even during weekends and holidays with effect from December 30, 2023.25It is expected that this measure will facilitate better fund management by the banks. This measure will be reviewed after six months or earlier, if needed.

21. The Indian rupee has exhibited low volatility compared to its EME peers in the calendar year 2023, despite elevated US treasury yields and a stronger US dollar.26The relative stability of the Indian rupee reflects the improving macroeconomic fundamentals of the Indian economy and its resilience in the face of formidable global tsunamis.

22. Recently, the Reserve Bank and the Bank of England have signed a Memorandum of Understanding on cooperation and exchange of information relating to the Clearing Corporation of India Ltd (CCIL), a Central Counterparty (CCP),27regulated and supervised by the Reserve Bank. The MOU will enable the Bank of England to assess CCIL for recognition as a third country CCP for UK based banks to clear their transactions through CCIL. This MOU is based on principles of mutual cooperation and trust among regulators of both the countries. We hope regulators of other jurisdictions also accept these principles.

Financial Stability

23. Financial stability is a public good. The Reserve Bank judiciously uses micro and macro-prudential tools to safeguard financial stability. The recent pre-emptive measures28taken by the Reserve Bank in respect of Banks and NBFCs were geared towards addressing potential risks and preserving the resilience of the financial sector.29We do not wait for the house to catch fire and then act. Prudence at all times should be the guiding philosophy, both for the regulators and the regulated entities.

External Sector

24. In October 2023, both merchandise exports and imports came back into the expansionary zone. Services exports remained buoyant during Q2:2023-24. India has remained the top remittance-receiving country.30The net balance under services and remittances is expected to partly offset India’s current account deficit and keep it within the parameters of viability.

25. On the financing side, foreign portfolio investment (FPI) flows have seen a significant turnaround in 2023-24 with net FPI inflows of US$ 24.9 billion (up to December 6) as against net outflows in the preceding two years.31Net foreign direct investment (FDI), on the other hand, moderated to US$ 10.4 billion in April-October 2023 from US$ 20.8 billion a year ago. Net inflows under external commercial borrowings (ECBs) and non-resident deposit accounts are much higher than last year.32India’s external vulnerability indicators33 exhibit higher resilience in comparison with EME peers as well as since the taper tantrum period. India’s foreign exchange reserves stood at US$ 604 billion as on December 1, 2023. We remain confident of meeting our external financing requirements comfortably.

Additional Measures

26. I shall now announce certain additional measures.

Review of the Regulatory Framework for Hedging of Foreign Exchange Risks

27. The regulatory framework for foreign exchange derivative transactions was last reviewed in 2020. Based on market developments and feedback received from market participants, the extant regulatory framework for forex derivative transactions has been refined and consolidated under a single master direction. This will further deepen the forex derivatives market by enhancing operational efficiency and ease of access for users.

Framework for Connected Lending

28. The extant guidelines on connected lending are limited in scope. It has been decided to come out with a unified regulatory framework on connected lending for all regulated entities of the Reserve Bank. This will further strengthen the pricing and management of credit by regulated entities.

Regulatory Framework for Web-Aggregation of Loan Products

29. The Reserve Bank had introduced the regulatory framework for digital lending in August/September 2022. The digital lending ecosystem also comprises of services that aggregate loan offers from lenders (called web-aggregation of loan products) for guidance of customers. Several concerns relating to such web-aggregation of loan products harming consumers’ interest have come to our notice. It has, therefore, been decided to lay down a regulatory framework for web-aggregation of loan products. This is expected to result in enhanced customer centricity and transparency in digital lending.

Setting up of Fintech Repository

30. Financial entities like banks and NBFCs in India are increasingly partnering with Fintechs. For better understanding of developments in the Fintech ecosystem and to support this sector, it is proposed to set-up a Fintech Repository. This will be operationalised by the Reserve Bank Innovation Hub in April 2024 or earlier. FinTechs would be encouraged to provide relevant information voluntarily to this Repository.

Enhancing UPI Transaction Limit for Specified Categories

31. The limit for various categories of UPI transactions has been reviewed from time to time. It is now proposed to enhance the UPI transaction limit for payment to hospitals and educational institutions from ₹1 lakh to ₹5 lakh per transaction. This will help the consumers to make UPI payments of higher amounts for education and healthcare purposes.

e-Mandates for recurring online transactions – Enhancement of limit for specified categories

32. e-Mandates for making payments of recurring nature have become popular among customers. Under this framework, an additional factor of authentication (AFA) is currently required for recurring transactions exceeding ₹15,000. It is now proposed to enhance this limit to ₹1 lakh per transaction for recurring payments of mutual fund subscriptions, insurance premium subscriptions and credit card repayments. This measure will further accelerate the usage of e-mandates.

Establishment of Cloud Facility for the Financial Sector in India

33. Banks and financial entities are maintaining an ever-increasing volume of data. Many of them are utilising the cloud facilities for this purpose. The Reserve Bank is working on establishing a cloud facility for the financial sector in India for this purpose. Such facility would enhance data security, integrity and privacy. It would also facilitate better scalability and business continuity. The cloud facility is intended to be rolled out in a calibrated fashion over the medium term.

Conclusion

34. In a global economy clouded by uncertainties, monetary policy actions and communication can be a stabilising force by anchoring the expectations of economic agents. Clarity and consistency in action and communication is a time-tested principle for effective monetary policy. Policy makers have to be mindful of the risk of being carried away by a few months of good data or by the fact that CPI inflation has come within the target range. They have to be also mindful of the risk of overtightening, especially when large structural changes, geopolitical and geoeconomic shifts are taking place. On top of this, they have to be watchful of the risks from new shocks that could hit the economy from anywhere anytime.

35. We have now reached a stage when every action has to be thought through even more carefully to ensure overall macroeconomic and financial stability; more so, because the conditions ahead could be fickle. We have to remain vigilant and ready to act, as per the evolving outlook. India is better placed to withstand the uncertainties compared to many other countries. As the Indian economy treads the path to a brighter future, I recall the wise words of Mahatma Gandhi: “Progress is absolutely assured whenever there is …… an unalterable determination.”34

Thank you. Namaskar.

(Yogesh Dayal)

Chief General Manager

Press Release: 2023-2024/1437 Date : Dec 08, 2023

Notes:

1 The International Monetary Fund (IMF) in October 2023, projected world trade volume (goods and services) growth to decline sharply from 5.1 percent in 2022 to 0.9 percent in 2023 (revised down by 1.1 percentage points from the July 2023 projection before rising to 3.5 percent in 2024 (revised down by 0.2 percentage points).

2 The global supply chain pressures index (GSCPI), as released by Federal Reserve Bank of New York, eased during the current financial year. It continues to remain below its historical average since February 2023 and fell sharply from the pandemic-era highs.

3 In Q2:2023-24, the government final consumption expenditure increased by 12.4 per cent, while gross fixed capital formation (investment) posted a growth of 11.0 per cent. On the supply side, real gross value added (GVA) rose by 7.4 per cent, powered by 13.9 per cent increase in manufacturing and 13.3 per cent in construction activity.

4 As of December 1, 2023, rabi sowing stood at 434.7 lakh hectares (out of full season normal area of 648.3 lakh hectares) which is 5.3 per cent lower than last year, but 4.3 per cent higher than 5-year average (normal acreage) as on date.

5 Results of 1,703 manufacturing companies for Q2:2023-24 exhibit robust growth in profits as well as salaries and wages component.

6 Eight core industries grew by 8.4 per cent in June; 8.5 per cent in July; 12.5 per cent in August; 9.2 per cent in September; and 12.1 per cent in October.

7 PMI manufacturing continued to expand at 56.0 in November 2023.

8 In October 2023, e-way bills (30.5 per cent), toll collections (13.0 per cent), port traffic (13.8 per cent), railway freight traffic (8.5 per cent) and diesel consumption (9.3 per cent) recorded robust growth. In November 2023, e-way bills (8.5 per cent), toll collections (12.3 per cent) and port traffic (17.0 per cent) continued to post strong growth.

9 The growth of GST collections in November 2023 was the highest in 11 months.

10 PMI services continued to expand at 56.9 in November 2023.

11 Indicators of urban demand like domestic air passenger traffic, passenger vehicle sales and household credit expanded by double-digit rate in October.

12 According to Nielsen data, FMCG volumes in rural segment grew by 6.4 per cent in Q2:2023-24 as compared to (-) 3.6 per cent during Q2:2022-23 (4.0 per cent in Q1:2023-24). Amongst rural demand indicators, two-wheeler sales posted a significant turnaround and the contraction in tractor sales moderated in October.

13 According to Federation of Automobile Dealers Associations (FADA), for the 42 days festive period during October-November 2023, retail sales of two-wheeler and passenger vehicles recorded a growth of 20.7 per cent and 10.3 per cent, respectively

14 The combined (Centre plus States) Capital Outlay (viz., capital expenditure minus loans and advances) recorded a growth of 36.7 per cent in April-October 2023 as against 29.4 per cent last year.

15 Steel consumption (15.3 per cent), cement production (17.1 per cent) and imports of capital goods (9.4 per cent) grew strongly in October.

16 Early survey results suggest capacity utilisation increased by 40 bps to 74.0 per cent in Q2:2023-24. The long-term average is 73.7 per cent which pertains to the period Q1:2008-09 to Q1:2023-24 excluding Q1:2020-21. Seasonally adjusted CU, however, declined by 90 bps and stands at 74.5 per cent in Q2.

17 India’s merchandise exports expanded by 6.1 per cent to $33.5 billion, while imports increased by 9.6 per cent to $63.5 billion in October. Services exports expanded by 10.8 per cent, while imports declined by 0.4 per cent in October.

18 The persistence of inflation pressures across various sub-groups, such as cereals, pulses and spices, and pick-up in inflation in eggs, fruits and sugar, however, has kept food inflation in October still elevated.

19 Bloomberg Commodity Price Index moderated since the last MPC meeting. As per United States Department of Agriculture (USDA) most agricultural commodities prices have moderated. Food and Agriculture Organization’s (FAO’s) food price index has eased since August 2023.

20 According to the Reserve Bank’s survey of households, between September 2022 and November 2023 inflation expectations for 3 months ahead and 1 year ahead softened by 170 and 90 basis points, respectively.

21 As on December 1, 2023, the balance sheet size was Rs.65.1 lakh crore and based on the estimated nominal GDP of Rs.301.8 lakh crore in the Union Budget 2023-24, the balance sheet size to GDP ratio works out to 21.6 per cent.

22 MSF borrowing averaged nearly ₹0.95 lakh crore during September which further increased to ₹1.2 lakh crore during October-November 2023.

23 Average fund parked under the SDF was at ₹0.62 lakh crore and ₹0.58 lakh crore in October and November, respectively.

24 The weighted average lending rate (WALR) on fresh rupee loans rose by 199 basis points (bps) while that on outstanding loans rose by 112 bps during the current tightening cycle (May 2022 – October 2023). The weighted average domestic term deposit rates (WADTDRs) on fresh deposits and outstanding deposits rose by 228 bps and 172 bps, respectively, during the same period.

25 At present, the standing facilities of the Reserve Bank under the LAF – the SDF and the MSF – can be availed from 17:30 hours to 23:59 hours on all days including weekends and holidays. However, the reversal of the facilities – withdrawal of deposited funds for SDF and repayment of borrowed funds for MSF – for the transactions over the weekends and holidays, is available only on the next working day in Mumbai.

26 The coefficient of variation for the daily INR exchange rate vis-à-vis the US dollar was 0.66 (CY 2023), which is the lowest among peer emerging economies, including China, Malaysia, Russia, Turkey, Vietnam, South Africa and Thailand.

27 Central counterparties (CCPs) help manage counterparty credit risk and consequently reduce systemic risks of financial markets by mitigating the impact of failure of an institution.

28 On November 16, 2023, the Reserve Bank increased the risk weights on unsecured consumer credit exposures of banks and NBFCs (including credit card receivables) as well as bank lending to NBFCs, other than housing finance companies (HFCs). The regulated entities have also been advised to put in place Board approved limits for various sub-segments under consumer credit, specifically unsecured consumer credit.

29 The key financial indicators of scheduled commercial banks (SCBs) show further improvement. In September 2023, CRAR of SCBs increased to 16.8 per cent from 16.0 per cent in September 2022. Gross non-performing assets (GNPA) and net non-performing assets (NNPA) ratios declined to a decadal low of 3.3 per cent and 0.8 per cent, respectively as of September 2023. The return on asset (RoA) of SCBs increased to 1.3 per cent as of September 2023 from 1.0 per cent in September 2022. Net interest margin (NIM) of SCBs improved to 3.7 per cent as of September 2023 from 3.5 per cent in September 2022. The liquidity coverage ratio (LCR) of SCBs was comfortable at 135.4, much above the minimum stipulation of 100. The indicators of non-banking financial companies are also in line with that of the banking system as per the latest available data.

30 As per India’s balance of payments statistics, India’s inward remittances stood at US$ 112.5 billion in 2022-23.

31 Net outflows of US$ 14.1 billion in 2021-22 and US$ 4.8 billion in 2022-23.

32 Net inflows of ECBs to India were US$ 3.9 billion during April-October 2023 as against net outflows of US$ 4.2 billion a year ago. Non-resident deposit accounts witnessed higher net inflows at US$ 5.4 billion during April-September 2023 as compared with US$ 2.8 billion a year ago.

33 External debt to GDP ratio and reserves to external debt ratio were placed at 18.6 per cent and 94.6 per cent at end-June 2023, respectively. The reserve cover of imports is over 10 months.

34 Collected Works of Mahatma Gandhi, Volume 46.