The table turning judgement of the Permanent Court of Arbitration at The Hague came after a decade long battle fought by the Vodafone Plc against the Indian Income Tax Authorities and Government of India.

The Indian Income-tax Authorities have been burdened with substantial cost by the Permanent Court of Arbitration at The Hague by making the authorities liable to compensate Vodafone towards legal representation, assistance cost etc. amidst already piling fiscal deficits in this Covid Struck Era.

1. WHAT TRIGGERED ALL THIS?

1.1 Key Facts

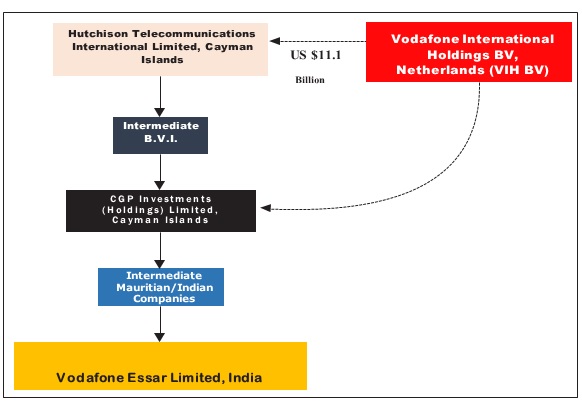

The main companies involved are as under:

| HTIL | Hutchison Telecommunications International Ltd. – a company incorporated in Cayman Island in 2004. It was listed on Hong Kong and New York Stock Exchanges. It was the seller and earner of Capital Gain. |

| VIH | Vodafone International Holdings BV – a company incorporated in Netherlands. It was the purchaser of one share of CGP. |

| CGP | CGP Investments (Holdings) Ltd. (CI) – a company incorporated in Cayman Islands in 1998. It is the company whose share has been transferred. |

| HEL | Hutchison Essar Ltd. – a company incorporated in India. It is the main business company. Controlling shareholding in the same has been transferred by virtue of Share Purchase Agreement and several related documents. Transfer of CGP share was one of several documents. |

Hutchison group is a Hong Kong group. Its listed company (HTIL) held a major portion of shares in HEL through a structure of several companies. The investment hierarchy was as given below :

1.2 Chronology of Events that Followed:

| 1992 | The Hutchison Group of Hong Kong acquired interest in the mobile telecommunications industry in india, through a joint venture vehicle, Hutchison Max Telecom Ltd, (renamed Hutchison Essar Ltd- (HEL) in August, 2005); |

| Jan 1998 | The Hutchison Group Incorporation CGP Investments (Holdings) Ltd (CGP) in Cayman Islands; |

| 2004 | Hutchison Telecommunication International Ltd (HTIL) was incorporated and listed on the Hong Kong and New York Stock Exchanges. HTIL and its downstream companies (including CGP) held interest in the mobile telecommunications business in several countries including India; |

| Dec 2006 | HTIL puts its 67% stake in HEL up for sale, seeks bids from interested parties; Vodafone; Hinduja, Reliance Communications among the bidders. |

| Feb 11,2007 | Vodafone Group Plc makes a final binding offer of around US $ 11.10 billion, based on an enterprise value of US $ 18.800 billion of HEL. Hutch board accepts Vodafone Offer. |

| Mar 6, 2007 | Essar files objection with FIPB to Hutch-Vodafone deal, asserts that it has a ‘Right of First Refusal’. |

| Mar 15,2007 | HTIL arrives at a settlement with JV partner Essar, pays the latter $415mn. Essar agrees to support the Hutch – Vodafone deal. |

| Mar 15,2007 | The Joint Director of Income Tax (International Taxation) issues a notice under section 133(6) of the Income Tax Act, 1961 to HEL seeking information regarding the sale of stake of the Hutchison group in HEL, including the Shareholders agreements and details of the transaction for acquisition of the share capital of CGP; |

| Aug, 2007 | IT Department issues show-cause notice to VEL u/s 163(1) of the Income Tax Act, 1961 to explain why it should not be treated as a representative assesses of Vodafone International Holdings (VIH BV); |

| Sept, 2007 | IT Departments issues notice u/s. 201(1) and 201(1A) to VIH BV to show cause as to why it should not be treated as an assessee in default for failure to withhold tax; |

| Oct,2007 | VIH BV files a writ petition in the Bombay High Court contending that it was not liable to pay as the transaction between HTIL and VIH did not involve the transfer of any capital asset situated in India; |

| Dec,2008 | Bombay high court, which decided that Vodafone was liable to pay the taxes as claimed by the income tax authorities. Vodafone files SLP in Supreme Court against Bombay HC Order; |

| Jan, 2009 | Supreme Court dismisses SLP, orders that tax department first pass an order on jurisdiction issue, against which VIH BV can approach the Bombay HC; |

| May, 2010 | IT Dept issues 763 pages final order, claiming jurisdiction to tax the deal. It calculates a liability of around Rs. 12000 Cr; |

| June, 2010 | VIH BV files a writ petition in Bombay HC challenging the IT Department’s final order of May 2010; |

| Sep, 2010 | Bombay HC again rules in favor of IT Dept, says the target company at all times was HEL; |

| Oct, 2010 | IT Dept fixes liability of Rs. 11,297 Crore; |

| Nov, 2010 | SC directs VIH BV to deposit Rs. 2500 Cr and provide bank guarantee for Rs. 8500 Cr; |

| March,2011 | IT Dept issues penalty notice u/s.271C to VIH BV for failure to deduct tax at source; |

| April,2011 | VIH BV files SLP in Supreme Court against penalty notice. SC Orders IT dept to pass penalty order, but not to enforce it; |

| May, 2011 | IT Department passes Rs. 7900 Cr penalty order on VIH BV; |

| 2012 | VIH BV challenged the notice before the Hon’ble Supreme Court of India. The Hon’ble Court decided the appeal in favor of VIH BV and held that “the Indian revenue authorities do not have the jurisdiction to impose tax on an offshore transaction between two non-residents entities wherein controlling interest in a (Indian) resident company is acquired by the non-resident company in the transaction”. |

1.3 Retrospective Amendment in Income Tax Act :

In May 2012, Parliament passed Finance Act, 2012 introducing retrospective amendments in Section 2(47) [Definition of “Transfer”], Section 2(14) [Definition of “Capital Asset”] and Section 9 [Income deemed to accrue or arise in India], thereby clarifying the applicability of tax on any gain on transfer of shares in a non-resident company, which derives significant value from underlying Indian assets. The amendments overruled Hon’ble Supreme Court’s decision and Vodafone was made liable to pay the tax along with interest approximating to INR 20,000 Crores.

1.4 Vodafone Retaliates through Arbitration:

Vodafone retaliated under Bilateral Investment Treaties (BIT) against Union of India in 2014 under the India-Netherlands Bilateral Investment Promotion & Protection Agreement (BIPA)[1]. Vodafone argued that the imposition of tax claims through retrospective amendment, even when the final word had already been said by the Supreme Court, amounts to a violation of fair and equitable treatment (FET) promised under the India-Netherlands BIT. The India-Netherlands BIT in its Article 4.1 provides that “the investors shall at all times be accorded fair and equitable treatment, which includes an obligation to ensure a stable and predictable regulatory environment”.

Vodafone in continuation of existing India-Netherlands BIPA initiated second arbitration under India-UK BIPA in 2017. The second proceedings were initiated by Vodafone because India questioned the jurisdictional objection in the arbitration under India-Netherlands BIPA. The Indian government approached the Delhi high court seeking an anti-arbitration injunction against Vodafone to keep it from initiating arbitration under the India-UK BIT. India argued that this would amount to an abuse of process as two different arbitrations on the same issue would amount to parallel proceedings, and would run the risk of inconsistent awards. Initially, the Delhi HC granted an ex parte interim order on August 22, 2017 restraining arbitration under India-UK BIT. However later, on May 7, 2018, the Delhi HC in final judgment dismissed the plea of the government seeking an anti-arbitration injunction on the ground of abuse of process.

What weighed heavily on the mind of the court to dismiss the government’s plea of abuse of process was the offer made by Vodafone to consolidate the arbitrations under the India-UK BIT and the India-Netherlands BIT. The court held that such an offer and undertaking is sufficient to placate India’s concerns regarding double relief which may be granted by two tribunals in respect of the same matter.

The case before the Permanent Court of Arbitration at The Hague was concluded in the month of September 2020, wherein, the International Court pronounced the conduct of Indian Tax Department of imposing tax liability along with interest and penalties levied on Telecom Giant, as breach of Article 4(1).

Further, the Indian government has not been asked to pay any compensation, it has been asked to pay approx. Rs 40 crore as partial compensation for the legal cost, and to refund the tax which has been collected so far.

2. WHAT LIES AHEAD?

There is considerable speculation as to whether this award would have any bearing on another Vodafone-type case, namely, the ongoing tax-related arbitration proceedings with Cairn Energy. It all depends on the government’s next course of action in the arbitration case with Vodafone. If it decides to retaliate by challenging the award before the High Court of Singapore – Singapore being the seat of the arbitration while The Hague was chosen as venue for the hearings – the issue may continue to remain contentious.

Moreover, the favorable award may also encourage more foreign investors to challenge retrospective tax measures under respective bilateral investment treaties. However, the government’s current position is that it will not introduce retrospective tax legislations, going forward.

India introduced a new Model Bilateral Investment Treaty in 2015, which restricts the scope of such treaties, and specifically seeks to exclude tax matters within the ambit of the ‘fair and equitable treatment’ clause. Thereafter, India unilaterally terminated many of its key investment treaties (including the ones with the Netherlands and the UK).

So, will the award impact existing and new bilateral investment and tax treaties?

The protections under investment treaties provide a recourse to foreign investors in addition to remedies in domestic courts. These protections will continue to be integral in bilateral or multilateral trade and investment negotiations.

Ultimately, claims under bilateral investment treaties are not going to go away in the near future. So, the Government should play a proactive role in factoring and planning for such litigation risk which may proceed.

3. CAN GOVERNMENT LEVERAGE FROM THIS AWARD?

Instead of viewing it as a loss of potential revenue amidst a rising fiscal deficit, by accepting the arbitration ruling, the Government of India could leverage this opportunity to restructure its course on retrospective taxation. This would certainly send a positive signal to the investor community in the UK, as well as in the rest of the world.

Economic reforms in India amidst the challenging times of Covid-19 pandemic have already created a negative sentiments among investors. As India advances its dream to emerge as the manufacturing hub of the world under the Aatmanirbhar Bharat and Make in India missions, it’s time to show the world that India is self-reliant as far as stability of tax policy is concerned. Several developed countries are contemplating the relocation of part of their manufacturing supply chains to destinations other than China. Far beyond bilateral treaties, acceptance of the Vodafone arbitration ruling and amendments in the law related to retrospective taxation would surely propel India’s rightful claim as a worthwhile global manufacturing destination that is a viable and competitive alternative to China.

To conclude, the stability of taxation and economic policies, in general, could be a key driver for increased inflow of FDI from the UK and the rest of the world to India in both the short to medium-term horizons.

[1] BIPA is an agreement between two sovereign contracting states to strengthen, extend and intensify the economic relations between them particularly with respect to investments by the investors of one contracting nation in the territory of the other contracting nation.

Disclaimer: The contents of this article are for information purposes only and do not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

Author Bio