BACKGROUND:

With the influx of more and more technology, financial transactions has taken an exchange platform that is totally cashless and people are becoming more dependent on e-transactions due to its advantage of being most user friendly one.

Transactions via e-wallets and Unified Payment Interface (hereinafter referred as “UPI”) transactions have been boosted so steadily in last of couple of months and why should it be so? In today’s time where there are restrictions from same bank ATM, withdrawal charges, transaction limits, people prefer to go cashless and use digital wallets or UPI transfers ,making it a stagnant route for future too. Making an application for UPI payments acting as an engine to transact, gives one more convenience to the level at its best. E-wallets keeps one’s money so handy so that one even do not need to wait to credit e-wallet from his bank account, resulting in a lot in saving time.

E-wallets also allow one to earn cashbacks which also one of the reason people prefer to use it more tremendously.

TAXATION OF TRANSACTIONS THROUGH EWALLET AND UNIFIED OAYMENT INTERFACE (UPI)

And one can never deny the fact that where there is an Income, there is a tax.

It’s a myth that money received from UPI may not get traced , the fact is Income Tax Department Of India traces every transaction, as it is being performed via electronic mode linked with Know Your Customer (hereinafter referred as “KYC”) details.

Funds transacted through these modes are also taxable as per Income tax Rules. As per Income tax Rules, reporting of Income from Capital Gains, Income from Salary, Income from Other Sources is mandatory to mention while filing an Income tax return (hereinafter referred as “ITR”). Likewise, funds received via UPI or E-wallets are also required to be put forth while filing the ITR.

KEY POINTS TO UNDERSTAND TAXATION OF UPI PAYMENTS:

- Maximum limit for transfer of funds via UPI is Rs 1 lakh, exceeding which the amount is subject to tax.

- As per rule 3(7)(iv) of Income Tax Rules, employers gives a gift voucher of over Rs 5,000 through UPI ,then there will be levied a tax on it.

- Furthermore, where it comes to other vouchers like vouchers received from family and friends, that will also be taxable where such voucher worth over Rs 50,000 in a financial year.

Even cashback earned is also taxable if the amount is above Rs 50,000 in a financial Year, under section 56(2)(X) of Income tax Act, 1961.

PARAMOUNT WELFARE TO DEPARTMENT, CONSEQUENT BENEFIT TO NATION:

Speaking of the time where just cash transactions used to take place along with bank transactions, all the transactions did not come under the tracing by the department because the ease UPI money transfer has made is nothing but made people compelling to make use of it to their ease and what people do is do what is tranquil. This has been made a very wide collection counter for tax for Income Tax Department of India because UPI transactions can easily be traced with KYC details of payer or a receiver of such money.

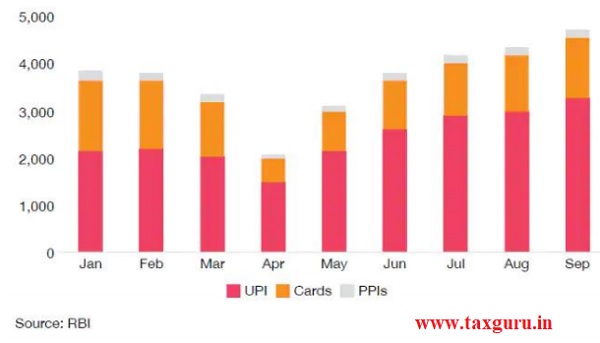

As per the records of National Payments Corporation Of India (NPCI), UPI transactions had touched the Rs 100 crore mark in October,2020 resulting in Rs207.16 Crores. As many as 189 banks are live on the UPI platform, the platform witnessed Rs 180 Crores transcations worth Rs 3.29 Lakh Crores in September. Following Statistics can depict the the increase in use of UPI payments have lowered the use of payments by cards that have taken place in year 2020 in India.

The below graph depicts the Transaction amount that have been made using UPI channel in India in Year 2020

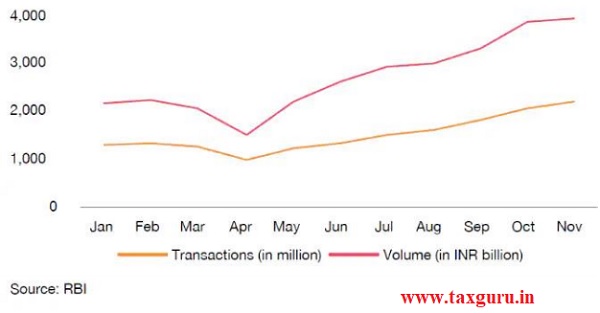

With the arise of pandemic COVID-19 outbreak back in last year, a nationwide lockdown also pushed the digital transactions in the country. Reportedly, 80% of older consumers were showing signs of adopting digital payments in the months following the initial lockdown.

All such details show that Tax earned by the revenue have also boosted up because increase in digital payments resulting in addition to the growth of the nation.

CONCLUSION:

With the increasing use of UPI Payments, Government is having more revenue in the form of tax collection as the transactions which are being incurred in digital mode, being tracked easily through respective bank accounts, which were used to be non accountable as they were usually done in cash earlier, aftermath made easy use for the user making or receiving the payment as well as making easy for the department too to track the respective assessee regarding such income.

Furthermore, as per section 44AD of Income Tax Act, 1961, a Resident Individual /HUF/Firm who has not claimed deduction under section 10AA OR 80IA TO 80RRB, is required to pay tax @6% of the Turnover/Gross Receipts instead of 8% if such turnover/Gross receipts realized by Account Payee Cheque /Demand Draft/Electronic Payment through Bank Account or any other electronic mode, which can also one of the major rationale due to which one can opt to electronic means as Department also wants that lot more transactions must be dealt via electronic platform, resulting in a win-win situation both for the assesse as well as Income Tax Department of India.

Author Bio