CBDT issued Income Tax Circular No. 04/2022 on 15th March 2022 and explained all provisions related to deduction of Tax At Source (TDS) on Salary or Income Tax Payable on Salary for the Financial Year 2021-22 / Assessment Year 2022-23.

GOVERNMENT OF INDIA

MINISTRY OF FINANCE

(DEPARTMENT OF REVENUE)

CENTRAL BOARD OF DIRECT TAXES

DEDUCTION OF TAX AT SOURCE-

INCOME-TAX DEDUCTION FROM SALARIES

UNDER SECTION 192 OF THE INCOME-TAX ACT, 1961

DURING THE FINANCIAL YEAR 2021-22

CIRCULAR NO. 04/2022

NEW DELHI, the 15th March, 2022

F.No. 275/192/2020-IT(B)

Government of India

Ministry of Finance

Department of Revenue

Central Board of Direct Taxes

*****

North Block, New Delhi

Dated the 15th March, 2022

SUBJECT: INCOME-TAX DEDUCTION FROM SALARIES DURING THE FINANCIAL YEAR 2021-22 UNDER SECTION 192 OF THE INCOME-TAX ACT, 1961.

*****

Reference is invited to Circular No. 20/2020 dated 03.12.2020 whereby the rates of deduction of income-tax from the payment of income under the head “Salaries” under Section 192 of the Income-tax Act, 1961 (hereinafter ‘the Act’), during the financial year 2020-21, were intimated. The present Circular contains the rates of deduction of Income-tax from the payment of income chargeable under the head “Salaries” during the financial year 2021-22 and explains certain related provisions of the Act and Income-tax Rules, 1962 (hereinafter the Rules). All the sections and rules referred are of Income-tax Act, 1961 and Income-tax Rules, 1962 respectively unless otherwise specified. The relevant Acts, Rules, Forms and Notifications are available at the website of the Income Tax Department-www. incometaxindia.gov. in.

As per section 192 (1) of the Act, any person responsible for paying any income chargeable under the head “Salaries” shall, at the time of payment, deduct income-tax on the amount payable at the average rate of income-tax computed on the basis of the rates in force for the financial year in which the payment is made, on the estimated income of the assessee under the head of Salary income for that financial year.

The section also provides that a person responsible for paying any income chargeable under the head “Salaries” shall furnish to the person to whom such payment is made a statement giving correct and complete particulars of perquisites or profits in lieu of salary provided to him and the value thereof.

Page Contents

- 1. Definition of “salary”, “perquisite” and “profit in lieu of salary” (section 17)

- 2. Rates of Income-Tax as Per Finance Act, 2021

- 3.2 Payment of Tax on Perquisites by Employer

- 3.3 Computation of Average Income Tax

- 3.4 Salary from more than one employer

- 3.5 Relief When Salary Paid in Arrear or Advance

- 3.6 Information regarding Income under any other head

- 3.7 Computation of income under the head `Income from house property”

- 3.8 Adjustment for Excess or Shortfall of Deduction

- 3.9 Salary Paid in Foreign Currency

- 4 Persons Responsible For Deducting Tax And Their Duties

- 4.1 Tax Deduction at Source

- 4.2 Deduction of Tax at Nil or Lower Rate

- 4.3 Deposit of Tax Deducted

- 4.4 Mode of Payment of TDS

- 4.5 Interest, Penalty & Prosecution for Failure to Deposit Tax Deducted

- 4.6 Furnishing of Certificate for Tax Deducted (Section 203)

- 4.7 Furnishing of particulars pertaining to perquisites, etc. – Section 192(2C)

- 4.8 Mandatory Quoting of PAN or Aadhaar number as the case may be and TAN

- 4.9 Compulsory Requirement to furnish PAN or Aadhaar by employee (Section 206AA)

- 4.10 Statement of deduction of tax under section 200(3) [Quarterly Statement of TDS1

- 4.11 Fee for default in furnishing statements u/s 200(3) of the Act

- 4.12 Rectification of mistake in filing TDS Statement

- 4.13 Penalty for failure to furnishing statements or furnishing incorrect information (section 271H)

- 4.14 TDS on Income from Pension

- 5. Computation Of Income Under The Head “Salaries”

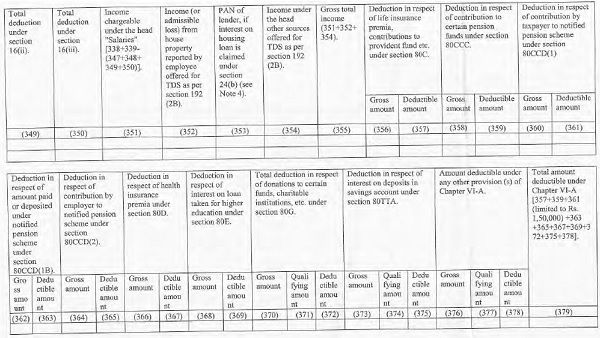

- 5.5 Deductions Under Chapter VI-A of the Act

- 5.5.1 Deduction in respect of Life insurance premia, deferred annuity, contributions to provident fund, subscription to certain equity shares or debentures, etc. (section 80C)

- 5.5.2 Deduction in respect of contribution to certain pension funds (Section 80CCC)

- 5.5.3 Deduction in respect of contribution to pension scheme of Central Government (Section 80CCD):

- 5.5.4 Deduction in respect of health insurance premia paid, etc. (Section 80D)

- 5.5.5 Deductions in respect of expenditure on persons or dependants with disability

- 5.5.6 Deduction in respect of medical treatment, etc. (Section 80DDB):

- 5.5.7 Deduction in respect of interest on loan taken for higher education (Section 80E):

- 5.5.8 Deduction in respect of interest on loan taken for certain house property (Section 80EEA):

- 5.5.9 Deduction in respect of the interest payable on loan taken for the purpose of purchase of an electric vehicle (80EEB)

- 5.5.10 Deductions on respect of donations to certain funds, charitable institutions. etc. (Section 80G):

- 5.5.11 Deductions in respect of rents paid (Section 80GG):

- 5.5.12 Deductions in respect of certain donations for scientific research or rural development (Section 80 GGA):

- 5.5.13 Deduction in respect of interest on deposits in savings account (Section 80TTA):

- 5.5.14 Deduction in respect of interest on deposits in case of senior citizens (Section 80TTB):

- 6. Rebate of Rs12,500 For Individuals Having Total Income Upto Rs 5 Lakh [Section 87A]

- 7. TDS on payment of accumulated balance under recognised provident fund and contribution from approved superannuation fund:

- 8. DDOs to obtain evidence/proof of claims:

- 9. Calculation of income-tax to be deducted:

- 10. Miscellaneous:

- ANNEXURE-I

- III. Procedure of preparation and furnishing Form 24G at TIN-Facilitation Centres (TIN-FCs):

- ANNEXURE IV Furnishing of Monthly Form No. 24G Statements by Pay and Accounts Officers (PAOs)/District Treasury Officers (DTOs)/Cheque Drawing and Disbursing Officers(CDDOs)

- V. “Person Responsible for filing Form No. 24G in case of State Govt. Departments”

- ANNEXURE VI POINT NO.4.9 OF DRAFT CIRCULAR OF DEDUCTION OF TAX AT SOURCE FROM SALARIES U/S 192 OF THE INCOME TAX ACT, 1961 — FINANCIAL YEAR 2015-16

- ANNEXURE-VII DEPTT. OF ECO. AFFAIRS NOTIFICATION DATED 22.12.2013

- ANNEXURE-VIII BOARD’S NOTIFICATION DATED 24.11.2000

- ANNEXURE-X FORM NO. 10BA

- ANNEXURE-B

1. Definition of “salary”, “perquisite” and “profit in lieu of salary” (section 17)

1.1 What is salary?

As per section 15 of the Act, the following incomes are chargeable to income-tax under the head “Salaries”—

(a) any salary due from an employer or a former employer to an assessee in the previous year, whether paid or not;

(b) any salary paid or allowed to him in the previous year by or on behalf of an employer or a former employer though not due or before it became due to him;

(c) any arrears of salary paid or allowed to him in the previous year by or on behalf of an employer or a former employer, if not charged to income-tax for any earlier previous year.

As per section 17 of the Act, Salary includes the following:

i) wages;

ii) any annuity or pension;

iii) any gratuity;

iv) any fees, commissions, perquisites or profits in lieu of or in addition to any salary or wages;

v) any advance of salary;

vi) any payment received by an employee in respect of any period of leave not availed of by him;

vii) the portion of the annual accretion to the balance at the credit of an employee participating in a recognised provident fund, to the extent to which it is chargeable to tax under rule 6 of Part A of the Fourth Schedule;

a) contributions made by the employer to the account of the employee in a recognized provident fund in excess of 12% of the salary of the employee, and

b) interest credited on the balance to the credit of the employee in so far as it is allowed at a rate exceeding such rate as may be fixed by Central Government by notification in the Official Gazette;

vii) the contribution made by the Central Government or any other employer to the account of the employee under the New Pension Scheme as notified vide Notification F.N. 5/7/2003- ECB&PR dated 22.12.2003 (enclosed as Annexure VII) referred to in section 80CCD (para 5.5.3 of this Circular);

ix) the aggregate of all sums that are comprised in the transferred balance as referred to in sub rule (2) of rule 11 of Part A of the Fourth schedule of the Act in case of an employee participating in a recognized provident fund, to the extent to which it is chargeable to tax under sub-rule (4) thereof.

It may be noted that, since salary includes pension, tax at source would have to be deducted from pension also, unless otherwise so required. However, no tax is required to be deducted from the commuted portion of pension to the extent exempt under section 10 (10A).

Family Pension is chargeable to tax under the head “Income from other sources” and not under the head “Salaries”. Therefore, provisions of section 192 of the Act are not applicable. Hence, DDOs are not required to deduct TDS on family pension paid to person.

1.2 What is a Perquisite?

As per Section 17(2) of the Act, perquisites include:

i) The value of rent-free accommodation provided to the employee by his employer;

ii) The value of any concession in the matter of rent in respect of any accommodation provided to the employee by his employer;

iii) The value of any benefit or amenity granted or provided free of cost or at concessional rate in any of the following cases:

a) By a company to an employee who is a director of such company;

b) By a company to an employee who has a substantial interest in the company;

c) By an employer (including a company) to an employee, who is not covered by (a) or (b) above and whose income under the head “Salaries” (whether due from or paid or allowed by, one or more employers), exclusive of the value of all benefits or amenities not provided for by way of monetary payment, exceeds Rs.50,000/-.

[What constitutes concession in the matter of rent have been prescribed in Explanations 1 to 4 below section 17(2)(ii) of the Act.]

iv) Any sum paid by the employer in respect of any obligation which would otherwise have been payable by the assessee.

v) Any sum payable by the employer, whether directly or through a fund, other than a recognized provident fund or an approved superannuation fund or other specified funds u/s 17, to effect an assurance on the life of an assessee or to effect a contract for an annuity.

vi) The value of any specified security or sweat equity shares allotted or transferred, directly or indirectly, by the employer, or former employer, free of cost or at concessional rate to the employee. For this purpose,

(a) “specified security” means the securities as defined in section 2(h) of the Securities Contracts (Regulation) Act, 1956 and, where employees’ stock option has been granted under any plan or scheme therefore, includes the securities offered under such plan or scheme;

(b) “sweat equity shares” means equity shares issued by a company to its employees or directors at a discount or for consideration other than cash for providing know-how or making available rights in the nature of intellectual property rights or value additions, by whatever name called;

(c) the value of any specified security or sweat equity shares shall be the fair market value of the specified security or sweat equity shares, as the case may be, on the date on which the option is exercised by the assessee as reduced by the amount actually paid by, or recovered from the assessee in respect of such security or shares;

(d) “fair market value” means the value determined in accordance with the method as may be prescribed (refer Rule 3(9) of the IT Rules);

(e) “option” means a right but not an obligation granted to an employee to apply for the specified security or sweat equity shares at a predetermined price;

(vii) the amount or the aggregate of amounts of any contribution made to the account of the assessee by the employer—

(a) in a recognised provident fund;

(b) in the scheme referred to in sub-section (1) of section 80CCD; and

(c) in an approved superannuation fund, to the extent it exceeds seven lakh and fifty thousand rupees in a previous year;

(viia) the annual accretion by way of interest, dividend or any other amount of similar nature during the previous year to the balance at the credit of the fund or scheme referred to in clause (vii) above to the extent it relates to the contribution referred to in the said clause which is included in total income; and

(viii) the value of any other fringe benefit or amenity as prescribed in Rule 3.

1.3 What is profit in lieu of salary?

As per Section 17(2) of the Act, Profits in lieu of salary’ include:

I. the amount of any compensation due to or received by an assessee from his employer or former employer at or in connection with the termination of his employment or the modification of the terms and conditions relating thereto;

II. any payment (other than any payment referred to in clauses (10), (I OA), (10B), (11), (12) (13) or (13A) of section 10) due to or received by an assessee from an employer or a former employer or from a provident or other fund, to the extent to which it does not consist of contributions by the assessee or interest on such contributions or any sum received under a Keyman insurance policy including the sum allocated by way of bonus on such policy.

“Keyman insurance policy” shall have the same meaning as assigned to it in section 10(IOD);

III. any amount due to or received, whether in lump sum or otherwise, by any assessee from any person—

(A) before his joining any employment with that person; or

(B) after cessation of his employment with that person.

2. Rates of Income-Tax as Per Finance Act, 2021

As per the Finance Act, 2021, the rates of income tax for the FY 2021-22 (i.e. Assessment Year 2022-23) are as follows:

2. 1 Rates of tax

A. Normal Rates of tax: In the case of every individual other than the individuals referred to in para (B) and (C) below:

| S. No |

Total Income | Rate of tax |

| 1 | Where the total income does not exceed Rs. 2,50,000/-. | Nil; |

| 2 | Where the total income exceeds Rs. 2,50,000/- but does not exceed Rs. 5,00,000/-. | 5 per cent of the amount by which the total income exceeds Rs. 2,50,000/-; |

| 3 | Where the total income exceeds Rs. 5,00,000/- but does not exceed Rs. 10,00,000/-. | Rs. 12,500/- plus 20 per cent of the amount by which the total income exceeds Rs. 5,00,000/-; |

| 4 | Where the total income exceeds Rs. 10,00,000/-. | Rs. 1,12,500/- plus 30 per cent of the amount by which the total income exceeds Rs. 10,00,000/-. |

B. Rates of tax for every individual, being a resident in India, who is of the age of sixty years or more but less than eighty years at any time during the financial year:

| SI No | Total Income | Rate of tax |

| 1 | Where the total income does not exceed Rs. 3,00,000/- | Nil; |

| 2 | Where the total income exceeds Rs. 3,00,000 but does not exceed Rs. 5,00,000/- | 5 per cent of the amount by which the total income exceeds Rs. 3,00,000/-; |

| 3 | Where the total income exceeds Rs. 5,00,000/- but does not exceed Rs. 10,00,000/- | Rs. 10,000/- plus 20 per cent of the amount by which the total income exceeds Rs. 5,00,000/-; |

| 4 | Where the total income exceeds Rs. 10,00,000/- | Rs. 1,10,000/- plus 30 per cent of the amount by which the total income exceeds Rs. 10,00,000/- |

C. In case of every individual, being a resident in India, who is of the age of eighty years or more at any time during the financial year:

| SI No | Total Income | Rate of tax |

| 1 | Where the total income does not exceed Rs. 5,00,000/- | Nil; |

| 2 | Where the total income exceeds Rs. 5,00,000 but does not exceed Rs. 10,00,000/- | 20 per cent of the amount by which the total income exceeds Rs. 5,00,000/-; |

| 4 | Where the total income exceeds Rs. 10,00,000/- | Rs. 1,00,000/- plus 30 per cent of the amount by which the total income exceeds Rs. 10,00,000/-. |

2.2 Surcharge on Income-tax

The amount of Income-tax computed in accordance with the provisions of section 111A or section 112 or section 112A or the provisions of section 115BAC of the Income-tax Act, shall be increased by a surcharge for the purposes of the Union, calculated, in the case of every individual or Hindu undivided family or association of persons or body of individuals, whether incorporated or not, or every artificial juridical person referred to in sub-clause (vii) of clause (31) of section 2 of the Income-tax Act 1961—

(a) having a total income (including the income by way of dividend or income under the provisions of section 111A and section 112A of the Income-tax Act) exceeding fifty lakh rupees but not exceeding one crore rupees, at the rate of ten per cent. of such income-tax;

(b) having a total income (including the income by way of dividend or income under the provisions of section 111A and section 112A of the Income-tax Act) exceeding one crore rupees but not exceeding two crore rupees, at the rate of fifteen per cent. of such income-tax;

(c) having a total income (excluding the income by way of dividend or income under the provisions of section 111A and section 112A of the Income-tax Act) exceeding two crore rupees but not exceeding five crore rupees, at the rate of twenty-five per cent of such income-tax;

(d) having a total income (excluding the income by way of dividend or income under the provisions of section 111A and section 112A of the Income-tax Act) exceeding five crore rupees, at the rate of thirty-seven per cent of such income-tax; and

(e) having a total income (including the income by way of dividend or income under the provisions of section 111A and section 112A) exceeding two crore rupees, but is not covered under clauses (c) and (d), shall be applicable at the rate of fifteen per cent. of such income-tax:

Provided that in case where the total income includes any income by way of dividend or income chargeable under section 111A and section 112A of the Income-tax Act, the rate of surcharge on the amount of Income-tax computed in respect of that part of income shall not exceed fifteen per cent.:

Provided further that in the case of persons mentioned above having total income exceeding,

(a) fifty lakh rupees but not exceeding one crore rupees, the total amount payable as income-tax and surcharge on such income shall not exceed the total amount payable as income-tax on a total income of fifty lakh rupees by more than the amount of income that exceeds fifty lakh rupees;

(b) one crore rupees but does not exceed two crore rupees, the total amount payable as income-tax and surcharge on such income shall not exceed the total amount payable as income-tax and surcharge on a total income of one crore rupees by more than the amount of income that exceeds one crore rupees;

(c) two crore rupees but does not exceed five crore rupees, the total amount payable as income-tax and surcharge on such income shall not exceed the total amount payable as income-tax and surcharge on a total income of two crore rupees by more than the amount of income that exceeds two crore rupees;

(d) five crore rupees. the total amount payable as income-tax and surcharge on such income 7 shall not exceed the total amount payable as income-tax and surcharge on a total income of five crore rupees by more than the amount of income that exceeds five crore rupees.

2.3 Health and Education Cess

The amount of Income tax as increased by the applicable surcharge shall be further increased by an additional surcharge, for the purposes of Union, to be called “Health and Education Cess on Income-tax”.

Health and Education Cess on Income-tax shall be levied at the rate of four percent of income tax including surcharge wherever applicable. No marginal relief shall be available in respect of such cess.

2.4 Concessional Rates of Tax u/s 115BAC

Section 115BAC of the Income-tax Act, 1961 was inserted by the Finance Act, 2020 w.e.f. Assessment Year 2021-22. The new section 115BAC provides that the income-tax payable in respect of the total income of a person, being an individual or a HUF, for any previous year relevant to the assessment year beginning on or after the lst day of April, 2021, shall, at the option of such person, be computed at the concessional rates as given in table below:

| Sl. No. | Total Income | Rate of tax |

| 1 | Up to Rs. 2,50,000 | Nil |

| 2 | From Rs. 2,50,001 to Rs. 5,00,000 | 5 per cent |

| 3 | From Rs. 5,00,001 to Rs. 7,50,000 | 10 per cent |

| 4 | From Rs. 7,50,001 to Rs. 10,00,000 | 15 per cent |

| 5 | From Rs. 10,00,001 to Rs. 12,50,000 | 20 per cent |

| 6 | From Rs. 12,50,001 to Rs. 15,00,000 | 25 per cent |

| 7 | Above Rs. 15,00,000 | 30 percent |

Such person is required to exercise the option in the prescribed manner along with the return of income to be furnished under section 139(1) of the Act for the previous year relevant to the assessment year. The concessional rates of tax provided under section 115BAC are subject to the condition that the total income of the individual or HUF shall be computed : –

a) Without any exemption or deduction specified under clause (i) of sub-section (2) of section 115BAC.

b) Without set off of any loss specified in clause (ii) of sub-section (2) of section I I5BAC.

c) Without any exemption or deduction for allowances or perquisite, by whatever name called, provided under any other law for the time being in force, as specified in the clause (iv) of sub-section (2) of section 115BAC.

Further, surcharge on income-tax as contained in Para 2.2 shall be applicable in case of person opting for concessional tax regime. Where the person fails to satisfy the conditions contained in sub-section (2) in any previous year, the option shall become invalid in respect of the assessment year relevant to that previous year and other provisions of the Act shall apply, as if the option had not been exercised for the assessment year relevant to that previous year. Further, where the option is exercised under clause (i) of sub-section (5), in the event of failure to satisfy the conditions contained in sub-section (2), it shall become invalid for subsequent assessment years also and other provisions of the Act shall apply for those years accordingly.

The conditions specified in subsection (2) of section 115BAC is as follows:

For the purposes of sub-section (1), the total income of the individual or Hindu undivided family shall be computed—

(i) without any exemption or deduction under the provisions of clause (5) or clause (13A) or prescribed under clause (14) (other than those as may be prescribed for this purpose) or clause (17) or clause (32), of section 10 or section 10AA or section 16 or clause (b) of section 24 (in respect of the property referred to in sub-section (2) of section 23) or clause (iia) of sub-section (1) of section 32 or section 32AD or section 33AB or section 33ABA or sub-clause (ii) or sub-clause (iia) or sub-clause (iii) of sub-section (1) or subsection (2AA) of section 35 or section 35AD or section 35CCC or clause (iia) of section 57 or under any of the provisions of Chapter VI–A other than the provisions of subsection (2) of section 80CCD or section 80JJAA;

(ii) without set off of any loss,—

(a) carried forward or depreciation from any earlier assessment year, if such loss or depreciation is attributable to any of the deductions referred to in clause (i);

(b) under the head “Income from house property” with any other head of income;

(iii) by claiming the depreciation, if any. under any provision of section 32, except clause (iia) of sub-section (1) of the said section, determined in such manner as may be prescribed; and

(iv) without any exemption or deduction for allowances or perquisite, by whatever name called, provided under any other law for the time being in force.

Furthermore, in case of a person having income from business or profession, such person is required to exercise the option in prescribed manner on or before the due date specified under such-section (1) of section 139 of the Act for any previous year relevant to assessment year commencing on or after 01.04.2021 and such option once exercised shall apply to subsequent assessment years. However, in case of such persons, the option once exercised can be withdrawn only once and such person shall never be eligible to exercise the option again unless such person ceases to have income from business or profession.

3. SECTION 192 OF THE INCOME-TAX ACT. 1961: BROAD SCHEME OF TAX DEDUCTION AT SOURCE FROM “SALARIES”

3.1 Method of Tax Calculation

Every person who is responsible for paying any income chargeable under the head “Salaries” shall deduct income-tax on the estimated income of the assessee under the head “Salaries” for the financial year 2021-22. The income-tax is required to be calculated on the basis of the rates given in para 2 above, subject to the provisions related to requirement to furnish PAN or Aadhaar number, as the case may be, as per sec 206AA of the Act, and TDS u/s 192 shall be deducted at the time of each payment.

As per section 192(1C) of the Act, a person, being an eligible start-up referred to in section 80-IAC, responsible for paying any income to the assessee being perquisite of the nature specified in sub-clause (vi) of clause (2) of Section 17 in any previous year relevant to Assessment year 2021-22 and thereafter, shall deduct or pay, as the case may be, tax on such income within 14 days—

a) after the expiry of 48 months from end of the relevant assessment year; or

b) from the date of sale of such specified security or sweat equity share by the assessee; or

c) from the date of the assessee ceasing to be the employee of the person,

whichever is the earliest, on the basis of rates in force for the financial year in which the said specified security or sweat equity share is allotted or transferred.

Any employee intending to opt for the concessional rates of tax under section 115BAC of the Act, may intimate the deductor, being his employer, of such intention for each previous year and upon such intimation, the deductor shall compute his total income, and make TDS thereon in accordance with the provisions of section 1 1 5BAC. If such intimation is not made by the employee, the employer shall make TDS without considering the provision of section 115BAC of the Act. The intimation so made to the deductor shall be only for the purpose of TDS during the previous year and cannot be modified during that year. (CBDT Circular No. Cl of 2020 dated 13.04.2020)

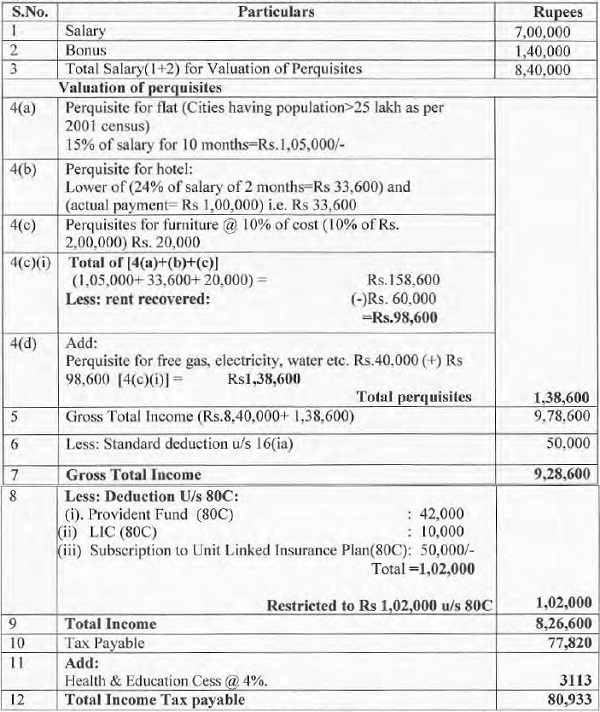

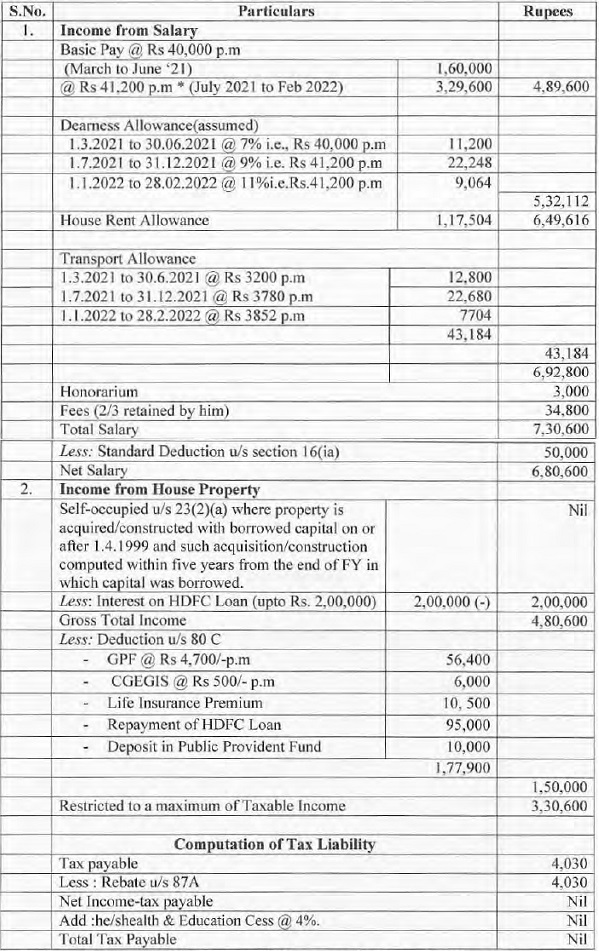

No tax, however, will be required to be deducted at source in a case unless the estimated salary income including the value of perquisites is taxable after giving effect to the exemptions, deductions and relief as applicable. (Some typical illustrations of computation of tax are given at Annexure-I).

3.2 Payment of Tax on Perquisites by Employer

Perquisites are divided in two parts i.e. monetary perquisites and non-monetary perquisites. Monetary perquisites are taxable for all employees and non-monetary perquisites are taxable in the hands of specified employees. The following employees are deemed as specified employees:

1) A director-employee

2) An employee who has substantial interest (i.e. beneficial owner of equity shares carrying 20% or more voting power) in the employer-company

3) An employee whose monetary income under the salary exceeds Rs.50,000.

The taxable value of perquisites can be determined on the basis of specific rules for valuation of certain perquisites as laid down in Rule 3 of the Income-tax Rules

An option has been given to the employer to pay the tax on non-monetary perquisites given to an employee. The employer may, at its option, make payment of the tax on such perquisites himself without making any TDS from the salary of the employee. As per Section 10(10CC) of the Act, the tax paid on such non-monetary perquisites by the employer is exempt from tax in the hands of the employee. However, the employer will have to pay the tax at the time when such tax was otherwise deductible i.e. at the time of payment of income chargeable under the head “salaries” to the employee.

3.3 Computation of Average Income Tax

For the purpose of making the payment of tax on the payment of any income in the nature of non-monetary perquisites, mentioned in para 3.2 above, tax payable is to be determined by calculating the average rate of tax on the income chargeable under the head “salaries”, including the value of perquisites for which tax has been paid by the employer himself.

Illustration:

The income chargeable under the head ‘salaries” of an employee below sixty years of age during the Financial Year 2021-22, is Rs. 6,00,000/- (inclusive of all perquisites), out of which, Rs. 50,000/- is on account of non-monetary perquisites and the employer opts to pay the tax on such perquisites as per the provisions discussed in para 3.2 above.

STEPS:

| Income Chargeable under the head -“Salaries” inclusive of all perquisites |

Rs. 6,00,000/- |

| Tax as per normal rates on Total Salary (including Cess) | Rs. 33,800/- |

| Average Rate of Tax [(33, 800/6,00,000) X100] | 5.63% |

| Tax payable on Rs.50,000/= (5.63% of 50,000) | Rs. 2815 |

| Amount required to be deposited each month | Rs. 235= 2815/12 |

The tax so paid by the employer shall be deemed to be TDS made from the salary of the employee.

3.4 Salary from more than one employer

Section 192(2) deals with situations where an individual is working under more than one employer or has changed from one employer to another. It provides for deduction of tax at source by such employer (as the tax payer/employee may choose) from the aggregate salary of the employee, who is or has been in receipt of salary from more than one employer. The employee is now required to furnish to the present/chosen employer details of the income under the head “Salaries” due or received from the former/other employer and also tax deducted at source therefrom, in writing and duly verified by him and by the former/other employer. The present/chosen employer will be required to deduct tax at source on the aggregate amount of salary (including salary received from the former or other employer).

3.5 Relief When Salary Paid in Arrear or Advance

3.5.1 Section 89 of the Act provides for relief to an assessee to whom salary is being paid in arrear or advance as a result of which, his total income is assessed at a higher rate than that at which it would otherwise have been assessed. Such an assessee can make an application to the Assessing Officer who shall grant relief in the prescribed manner. Rule 21A of the Rules provide the manner for computation of such relief.

3.5.2 Under section 192(2A) where the assessee, being a Government servant or an employee in a company, co-operative society, local authority, university, institution, association or body is entitled to the relief under Section 89, he/she may furnish to the person responsible for making the payment referred to in Para (3.1), such particulars in Form No. 10E (Rule 21AA of the Income tax Rules) duly verified by him, and thereupon the person responsible, as aforesaid, shall compute the relief on the basis of such particulars and take the same into account in making the deduction under Para(3.1) above. Further, such assessee shall upload the aforesaid Form 10E electronically in the e-Filing portal along with the return of income.

3.5.3 Here “university” means a university established or incorporated by or under a Central, State or Provincial Act, and includes an institution declared under Section 3 of the University Grants Commission Act, 1956 to be a university for the purpose of that Act.

3.5.4 With effect from 1/04/2010 (AY 2010-11), no such relief shall be granted in respect of any amount received or receivable by an assessee on his voluntary retirement or termination of his service, in accordance with any scheme or schemes of voluntary retirement or in the case of a public sector company referred to in section 10(10C)(i) (read with Rule 2BA), a scheme of voluntary separation, if an exemption in respect of any amount received or receivable on such voluntary retirement or termination of his service or voluntary separation has been claimed by the assessee under section 10(10C) in respect of such, or any other, assessment year.

3.6 Information regarding Income under any other head

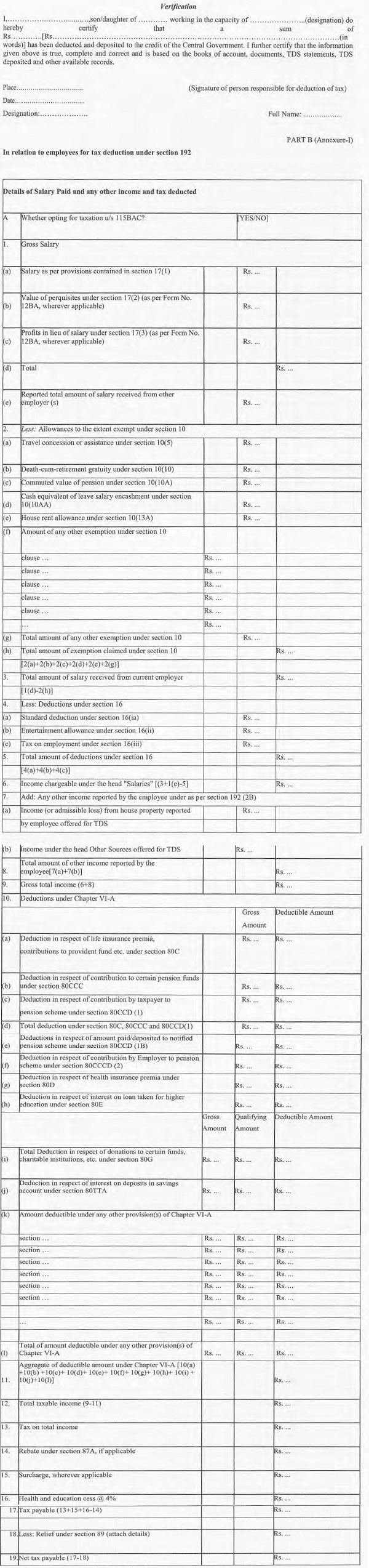

Section 192(2B) enables a taxpayer to furnish particulars of income under any head other than “Salaries” (not being a loss under any such head other than the loss under the head —’Income from house property’) received by the taxpayer for the same financial year and of any tax deducted at source thereon. The particulars may now be furnished in a simple statement, which is properly signed and verified by the taxpayer in the manner as prescribed under Rule 26B(2) of the Rules and shall be annexed to the simple statement. The form of verification is reproduced as under:

I, (name of the assessee), do declare that what is stated above is true to the best of my information and belief.

It is reiterated that the DDO can take into account loss only under the head “Income from house property”. Loss under any other head cannot be considered by the DDO for calculating the amount of tax to be deducted. It may be noted that loss under the head “Income from house property” can be set off only up to Rs. 2.00 lakh with the income under any other head of income in view of the amendment to section 71 of the Act vide Finance Act, 2017. Hence, loss under the head “Income from house property” in excess of Rs. 2.00 lakh is to be ignored for calculating the amount of tax deduction.

3.7 Computation of income under the head `Income from house property”

Section 192(2D) enables the person responsible for making the payment, to obtain the evidence or proof of the prescribed claims, including claim for set-off of loss. While taking into account the loss from House Property, the DDO shall ensure that the employee files the declaration referred to above and encloses therewith a computation of such loss from house property. Following details shall be obtained and kept by the employer in respect of loss claimed under the head “Income from House Property” separately for each house property:

a) Gross annual rent/value

b) Municipal Taxes paid, if any

c) Deduction claimed for interest paid, if any

d) Other deductions claimed

e) Address of the property

The DDO shall also ensure furnishing of the evidence or particulars in Form No. 12BB in respect of deduction of interest as specified in Rule 26C read with section 192 (2D).

3.7.1 Conditions for claim of deduction of interest on borrowed capital for computation of Income from House Property [section 24(b)1

Section 24(b) of the Act allows deduction from income from houses property on interest on borrowed capital as under :

i. the deduction is allowed only in case of house property which is owned and is in the occupation of the employee for his own residence. In case the house property is not occupied by the employee in view of his place of the employment being at other place, then his residence in that other place should not be in a building belonging to him.

ii. the quantum of deduction allowed as per table below:

| Si No |

Purpose of borrowing capital | Date of borrowing capital |

Maximum Deduction Allowable |

| 1 | Repair or renewal or reconstruction of the house | Any time | Rs. 30,000/- |

| 2 | Acquisition or construction of the house | Before 01.04.1999 | Rs. 30,000/- |

| 3 | Acquisition or construction of the house | On or after 01.04.1999 | Rs. 1,50,000/-

(upto AY 2014-15) |

| Rs. 2,00,000/- (w. e. f. AY 2015-16) |

|||

| 4 | Aggregate deduction of Si. I and Si. 3 of the table above shall not exceed Rs.2.00,000/- from the Financial Year 2019-20. | ||

In case of Serial No. 3 above:

(a) The acquisition or construction of the house should be completed within 5 years from the end of the FY in which the capital was borrowed. Hence, it is necessary for the DDO to have the completion certificate of the house property against which deduction is claimed either from the builder or through self-declaration from the employee.

(b) Further any prior period interest for the FYs upto the FY in which the property was acquired or constructed (as reduced by any part of interest allowed as deduction under any other section of the Act) shall be deducted in equal installments for the 14 FY in question and subsequent four FYs.

(c) The employee has to furnish before the DDO a certificate from the person to whom any interest is payable on the borrowed capital specifying the amount of interest payable. In case a new loan is taken to repay the earlier loan, then the certificate should also show the details of Principal and Interest of the loan so repaid.

As discussed in para 4.7.4, section 192(2D) read with rule 26C makes it mandatory for the DDO to obtain following details/evidences in respect of Interest deductible.

(i) Interest payable or paid

(ii) Name of the lender

(iii) Address of the lender

(iv) PAN or Aadhaar number of the lender

PAN or Aadhaar number, as the case may be, of the lender being financial institution or employer, is to be provided if it is available with the employee. However, in case of other lenders, obtaining of PAN or Aadhaar number is mandatory by the DDO.

3.8 Adjustment for Excess or Shortfall of Deduction

The provisions of Section 192(3) allow the deductor to make adjustments for any excess or shortfall in Tax deduction arising out of any previous deduction or failure to deduct during the financial year.

3.9 Salary Paid in Foreign Currency

For the purposes of deduction of tax on salary payable in foreign currency, the value in rupees of such salary shall be calculated at the “Telegraphic transfer buying rate” of such currency as on the date on which tax is required to be deducted at source (see Rule 26 and Rule 115).

4 Persons Responsible For Deducting Tax And Their Duties

Section 204 of the Act explains the meaning of the expression “Person responsible for paying”.

As per Clause (i) of section 204, in the case of payment of Salary, other than payments by the Central Government or the State Government, the “person responsible for paying” for the purpose of Section 192 means the employer himself or if the employer is a Company, the Company itself including the Principal Officer thereof.

As per Clause (iv) of section 204, in case the credit, or as the case may be. the payment of any sum chargeable under the Act, is made by or on behalf of Central Government or State Government, the Drawing and Disbursing Officer or any other person by whatever name called, responsible for crediting, or as the case may be, paying such sum is the “person responsible for paying” for the purpose of Section 192.

As per Clause (v) of section 204, in case of a person not resident in India, the “person responsible for paying” means the person himself or any person authorised by such person or the agent of such person in India including any person treated as an agent under section 163.

4.1 Tax Deduction at Source

The concept of Tax deduction at Source (TDS) was introduced with an aim to collect tax from the source of income. As per this concept, a person (deductor) who is liable to make payment of specified nature to any other person (deductee) shall deduct tax at source and remit the same into the account of the Central Government. The deductee, from whose income, tax has been deducted at source, would be entitled to get credit of the amount so deducted on the basis of Form 26AS or TDS certificate issued by the deductor.

4.1.2 Rates for tax deduction at source

Section 192 does not specify any TDS rate. However as per section 192(1), the tax deduction shall be made at the average rate of income tax on the amount payable, computed on the basis of the rates in force for the financial year in which the payment is made, on the estimated income under the head of Salary for that financial year. The rates as per different income slabs are specified in the First Schedule to the Finance Act. In the case of payment to non-resident persons, the withholding tax rates specified under the Double Taxation Avoidance Agreements shall also be considered.

4.2 Deduction of Tax at Nil or Lower Rate

If the jurisdictional TDS officer of the employer issues a certificate of No Deduction or Lower Deduction of Tax under section 197 of the Act, in response to the application filed before him in Form No 13 by the employee, then the DDO should take into account such certificate and deduct tax on the salary payable at the rates mentioned therein. (see Rule 28AA). The Unique Identification Number of the certificate is required to be reported in Quarterly Statement of TDS (Form 24Q),

4.3 Deposit of Tax Deducted

As per section 200 of the Act, any person responsible for deducting any sum has to pay within the prescribed time, the sum so deducted to the credit of the Central Government.

Rule 30 prescribes time and mode of payment of tax deducted at source to the account of Central Government.

4.3.1 Due dates for payment of TDS

Prescribed time of payment/deposit of TDS to the credit of Central Government account is as under:

In case of deduction by au Office of Government:

| Si No. | Description | Time up to which the tax deducted is to be deposited |

| 1 | Tax deposited without Challan [Book Entry] | same day |

| 2 | Tax deposited with Challan | 7th day of next month |

| 3 | Tax on perquisites opted to be deposited by the employer. | 7th day of next month |

In case of deduction by deductor other than an Office of Government

| SL No. | Description | Time up to which to be deposited. |

| I | Tax deducted in March | 30th April next financial year |

| 2 | Tax deducted in any other month | 7th day of next month |

| 3 | Tax on perquisites opted to be deposited by the employer | 7th day of next month |

As per Rule 30(3), an Assessing officer with prior approval of the Joint Commissioner of Income Tax may permit quarterly payments of TDS under section 192, for the quarters of the financial year on the dates specified in Table below:

| SI. No. | Quarter of the financial year ended on | Date for quarterly payment |

| 1 | 30th June | 7th July |

| 2 | 30th September | 7th October |

| 3 | 31′ December | r January |

| 4 | 31″ March | 30th April of the next Financial Year |

4.4 Mode of Payment of TDS

4.4.1 Compulsory filing of Statement by PAO, Treasury Officer, etc in case of payment of TDS by Book Entry u/ s 200 (2A)

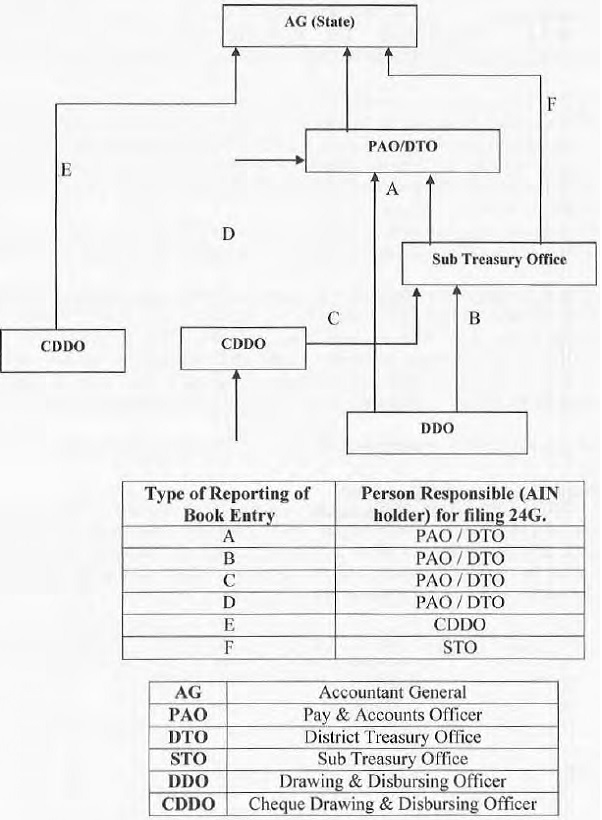

In case of an office of the Government, where tax has been paid to the credit of the Central Government without the production of a challan [Book Entry], the Pay and Accounts Officer or the Treasury Officer or the Cheque Drawing and Disbursing Officer or any other person, by whatever name called, to whom the deductor reports about the tax deducted and who is responsible for crediting such sum to the credit of the Central Government, shall-

(a) submit a statement in Form No. 24G under section 200 (2A) on or before the 30th day of April where statement relates to the month of March; and in any other case, on or before 15 days from the end of relevant month to the agency authorized by the Principal Director General of Income-tax (Systems) [TIN Facilitation Centres currently managed by M/s National Securities Depository Ltd] in respect of tax deducted by the deductors and reported to him for that month; and

(b) intimate the number (hereinafter referred to as the Book Identification Number or BIN) generated by the agency to each of the deductors in respect of whom the sum deducted has been credited. BIN consist of receipt number of Form 24G, DDO sequence number in Form No. 24G and date on which tax is deposited.

The statement in Form 24G shall be furnished electronically under digital signature or electronically along with the verification in Form 27A.

If the Pay and Accounts Officer or the Treasury Officer or the Cheque Drawing and Disbursing Officer or any other person, by whatever name called, as stated above, fails to deliver the statement within the time as required u/s 200(2A), he/she will be liable to pay, by way of penalty, under section 272A(2)(m), a sum which shall be Rs.100/- for every day during which the failure continues. However, the amount of such penalty shall not exceed the amount of tax which is deductible at source.

The procedure of furnishing Form 24G is detailed in Annexure III. PAOs/DDOs should go through the FAQs in Annexure IV to understand the correct process to be followed. The ZAO / PAO of Central Government Ministries is responsible for filing of Form No. 24G on monthly basis. The person responsible for filing Form No. 24G in case of State Govt. Departments is shown at Annexure V.

(Note: The TDS book adjustment statement in Form 24G for the month of May 2021, required to be furnished on or before 15th June 2021 under rule 30 was to be furnished on or before 30th June 2021, as per Circular no. 9 of 2021 dated 20th May 2021.)

4.4.2 Payment by an Income Tax Challan

(i) In case the payment is made by an income-tax challan, the amount of tax so deducted shall be deposited to the credit of the Central Government by remitting it, within the time specified in Table in para 4.4.1 above, into any branch of the Reserve Bank of India or of the State Bank of India or of any authorized bank;

(ii) In case of a company and a person (other than a company), to whom provisions of section 44AB are applicable, the amount deducted shall be electronically remitted into the Reserve Bank of India or the State Bank of India or any authorised bank accompanied by an electronic income-tax challan (Rule125).

The amount shall be construed as electronically remitted to the Reserve Bank of India or to the State Bank of India or to any authorized bank, if the amount is remitted by way of:

(a) Internet banking facility of the Reserve Bank of India or of the State Bank of India or of any authorized bank; or

(b) debit card. {Rule 30(7)1

4.5 Interest, Penalty & Prosecution for Failure to Deposit Tax Deducted

If a person fails to deduct the whole or any part of the tax at source, or, after deducting, fails to pay the whole or any part of the tax to the credit of the Central Government within the prescribed time, he/she shall be deemed to be an assessee-in-default in respect of such tax in accordance with the provisions of section 201, and shall also be liable to penal action u/s 221 of the Act. Further Section 201(1A) provides that such person shall be liable to pay simple interest at the rate of 1% for every month or part of the month on the amount of such tax from the date on which such tax was deductible to the date on which such tax is deducted: and at the rate of one and one-half percent for every month or part of a month on the amount of such tax from the date on which such tax was deducted to the date on which such tax is actually paid. Such interest shall be paid before furnishing the statement in accordance with the provisions of subsection (3) of section 200.

Section 271C inter alia lays down that if any person fails to deduct whole or any part of tax at source or fails to pay the whole or part of tax under the second proviso to section I 94B, he/she shall be liable to pay, by way of penalty, a sum equal to the amount of tax not deducted or paid by him.

Further, section 276B lays down that if a person fails to pay to the credit of the Central Government within the prescribed time, as above, the tax deducted at source by him or tax payable by him under the second proviso to Section I 94B, he/she shall be punishable with rigorous imprisonment for a term which shall not be less than three months but which may extend to seven years and with fine.

4.6 Furnishing of Certificate for Tax Deducted (Section 203)

4.6.1 Section 203 requires the DDO to furnish to the employee a certificate in Form 16 detailing the amount of TDS and certain other particulars. Rule 31 prescribes that Form 16 should be furnished to the employee by 15th June after the end of the financial year in which the income was paid and tax deducted. Even the banks deducting tax at the time of payment of pension are required to issue such certificates. Through Circular No. 12 of 2021 dated 25’1′ June 2021, the Central Board of Direct taxes extended the due date for furnishing Form 16 for F.Y. 2020-21 to the employee up to 31st July, 2021.

4.6.2 The certificate in Form 16 shall specify the following:

(a) Valid permanent account number (PAN) or Aadhaar number, as the case may be, of the deductee;

(b) Valid tax deduction and collection account number (TAN) of the deductor;

(c) (i) Book identification number or numbers (BIN) where deposit of tax deducted is without production of challan in case of an office of the Government;

(ii) Challan identification number or numbers (CIN*) in case of payment through bank.

(*CIN means the number comprising the Basic Statistical Returns (BSR) Code of the Bank branch where the tax has been deposited, the date on which the tax has been deposited and challan serial number given by the bank.)

(d) Receipt numbers of all the relevant quarterly statements of TDS (24Q). The receipt number of the quarterly statement is of 8 digit.

4.6.3 Further as per Circular 04/2013 dated 17-04-2013 all deductors (including Government deductors who deposit TDS in the Central Government Account through book entry) shall issue the Part A of Form No. 16, by generating and subsequently downloading it through TRACES Portal and after duly authenticating and verifying it, in respect of all sums deducted on or after the 1st day of April, 2012 under the provisions of section 192 of Chapter XVII-B. Part A of Form No 16 shall have a unique TDS certificate number. The deductor shall generate Tart B (Annexure)’ of Form No. 16 from the Traces website and issue to the deductee after due authentication and verification along with the Part A of the Form No. 16.

4.6.4 It may be noted that under the new TDS procedure, TAN of deductor/ PAN or Aadhaar number of the deductee and receipt number of TDS statement filed by the deductor act as unique identifier for granting online credit of TDS to the deductee. Hence due care should be taken in filling these particulars. Due care should also be taken in indicating correct CIN/ BIN in TDS statement.

4.6.5 If the DDO fails to issue these certificates to the person concerned, as required by section 203, he/she will be liable to pay, by way of penalty, under section 272A(2)(g), a sum which shall be Rs.100/- for every day during which the failure continues. However, the amount of such penalty shall not exceed the amount of tax which is deductible at source.

It is, however, clarified that there is no obligation to issue the TDS certificate in case tax at source is not deductible/deducted by virtue of claims of exemptions and deductions.

4.6.6 Vide CBDT notification 36/2019 dated 12.04.2019, Income-Tax (3rd Amendment Rules) 2019 were notified in which the ‘Part-B (Annexure)’ of Form 16 under Appendix-II of the Income Tax Rules, was modified. Form 16 has been further modified vide Income-tax (26th Amendment) Rules, 2021 notified on 02.09.2021. The modified Form 16 is placed at Annexure B of this TDS Circular.

4.6.7 Following points are to be kept in mind while filling amended Form 16:

1. Government deductors are required to fill information in item I of Part A if tax is paid without production of an income-tax challan and in item II of Part A if tax is paid accompanied by an income-tax challan.

2. Non-Government deductors are to fill information in item II of Part A.

3. The deductor shall furnish the address of the Commissioner of Income-tax (TDS) having jurisdiction as regards TDS statements of the assessee.

4. If an assessee is employed under one employer only during the year, certificate in Form No. 16 issued for the quarter ending on 31st March of the financial year shall contain the details of tax deducted and deposited for all the quarters of the financial year.

5. (i) If an assessee is employed under more than one employer during the year, each of the employers shall issue Part A of the certificate in Form No. 16 pertaining to the period for which such assessee was employed with each of the employers.

(ii) Part B (Annexure-I) of the certificate in Form No.16 may be issued by each of the employers or the last employer at the option of the assessee.

(iii) Part B (Annexure-11) of the certificate in Form 16 may be issued by the specified bank to a specified senior citizen (refer section 194P of the Act).

6. In Part A, in items I and II, in the column for tax deposited in respect of deductee, furnish total amount of tax, surcharge and health and education cess.

7. Deductor shall duly fill details, where available, in item numbers 2(f) and 10(k) before furnishing of Part B (Annexure) to the employee.

8. If an assessee is employed by more than one employer during the year, each of the employers shall issue Part A of the certificate in Form No. 16 pertaining to the period for which such assessee was employed with each of the employers and Part B may be issued by each of the employers or the last employer at the option of the assessee.

9. TDS certificate (Form16) would be generated for the deductee only if Valid PAN or Aadhaar number as the case may be, is correctly mentioned in the Annexure II of Form 24Q in Quarter 4 filed by the deductor. Moreover, employers are advised to ensure in Rom 16 that the status of “matching” with respect to “Form 24G/OLTAS” is ‘F’. If the status of matching is other than ‘ F’, kindly take necessary action promptly to rectify the same. It is pertinent to mention here that certain facilities have been provided to the deductors at website www.tdscpc.gov.in/including online correction of statements (Form 24Q).

[Note: TRACES is a web-based application of the Income-tax Department that provides an interface to all stakeholders associated with TDS administration. It enables viewing of challan status, downloading of NSDL Conso File, Justification Report and Form 16 / 16A as well as viewing of annual tax credit statements (Form 26AS). Each deductor is required to Register in the Traces portal, Form 16/16A issued to deductees should mandatorilv be generated and downloaded from the TRACES portal].

4.6.8 Certain essential points regarding the filing of the Statement in Form 24Q are mentioned below:

a. The employer should quote the gross amount of salary (including any amount exempt under section 10 and the deductions under chapter VI A) in column 321 (Amount paid/credited) of Annexure I of Form 24Q as per NSDL RPU (hereafter Return Preparation Utility).

b. The employer should quote the amount of salary excluding any amount exempt under section 10 in column 338 (Total amount of gross salary) of Annexure 11 of Form 24Q as per NSDL RPU.

c. The reason for non-deduction, lower rate of deduction (as provided under section 197) or higher rate of deduction(on account of non-furnishing of PAN by the deductee) has to be mentioned in column 328 of Annexure I of Form 24Q.

d. The total amount of salary received from other employer(s) to be quoted in column 337 of Annexure II of Form No. 24Q.

e. Employer is advised to quote Total Taxable Income (Column 346) in Annexure II without rounding-off and TDS should be deducted and reported accordingly i.e. without rounding-off of TDS also.

f. It is mandatory for non-Government deductors to quote PAN. In case of Government deductors,”PANNOTREQD” should be mentioned.

g. Fee paid under section 234E for late filling of TDS statement to be mentioned in separate column of Fee (column306)

h. In column 308, Government DDOs to mention the amount of TDS remitted by the PAO/TO/CDDO. Other deductors to write the exact amount of TDS deposited through challan.

i. In column 309, Government deductors to write “B” where TDS is remitted to the credit of Central Government through book adjustment. Other deductors to write”C”.

j. Challan/Transfer Voucher (CIN/BIN) particulars, i.e. 310, 311, 312 should be exactly the same as available at Tax Information Network.

k. In column 313, mention minor head as marked on the challan.

1. Where an employer deducts from the emoluments paid to an employee or pays on his behalf any contributions of that employee to any approved superannuation fund, all such deductions or payments should be included in the statement.

4.6.9 Authentication by Digital Signatures:

(i) Where a certificate is to be furnished in Form No. 16, the deductor may, at his option, use digital signatures to authenticate such certificates.

(ii) In case of certificates issued under clause (i), the deductor shall ensure that

a) the conditions prescribed in para 4.6.1 above are complied with;

b) once the certificate is digitally signed, the contents of the certificates are not amenable to change; and

c) the certificates have a control number and a log of such certificates is maintained by the deductor.

The digital signature is being used to authenticate most of the e-transactions on the Internet as transmission of information using digital signature is failsafe. It saves time specially in organisations having large number of employees where issuance of certificate of deduction of tax with manual signature is time consuming (Circular no 2 of 2007 dated 21.05.2007)

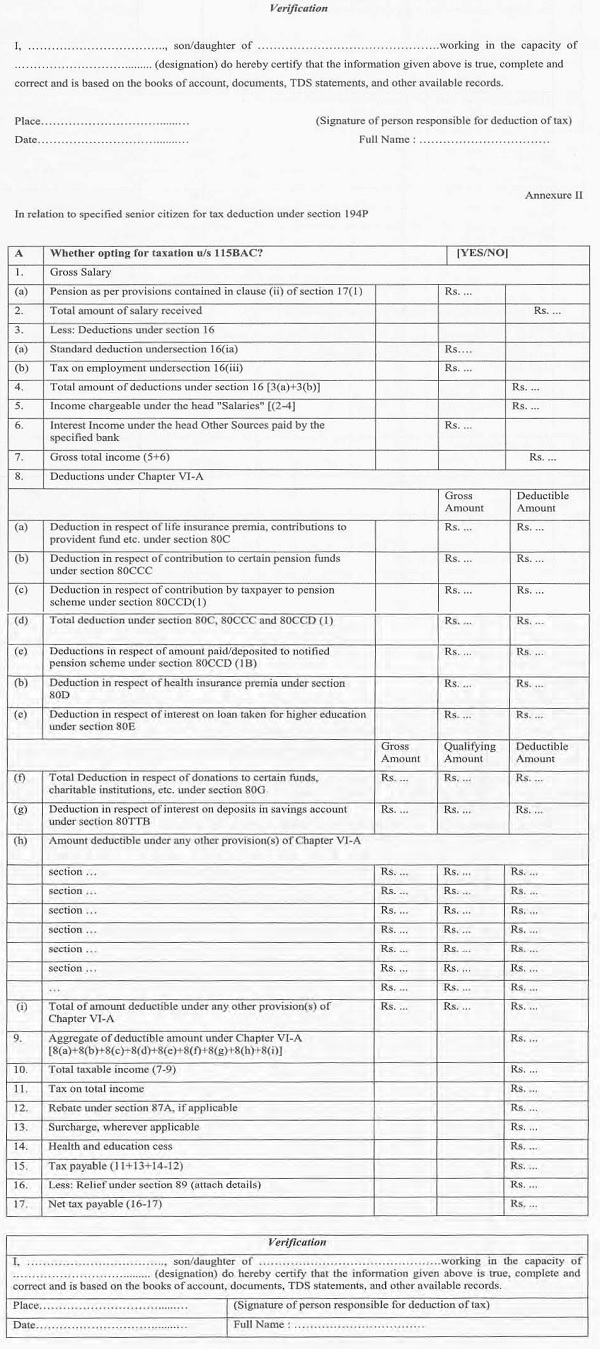

4.7 Furnishing of particulars pertaining to perquisites, etc. – Section 192(2C)

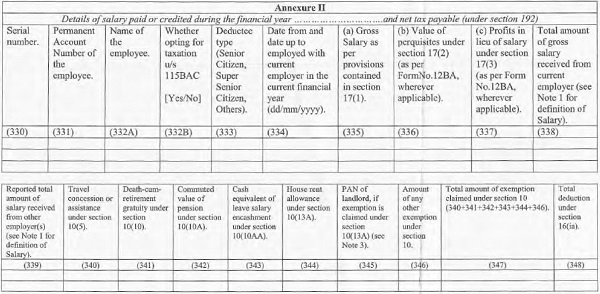

4.7.1 As per section 192(2C), the person responsible for paying income chargeable under the head “Salary” shall be responsible for providing correct and complete particulars of perquisites or profits in lieu of salary to the employee. The form and manner of such particulars are prescribed in Rule 26A i.e Form 12BA (placed as Annexure II) and Form 16 of the Rules. Information relating to the nature and value of perquisites, other fringe benefits or amenities and profits in lieu of salary is to be provided by the employer in Form 12BA in case the salary paid or payable is above Rs.1,50,000/-. In other cases, the information would have to be provided by the employer in Form 16 itself.

It may be noted that Form 12BA is to be furnished in addition to Form 16 to the employee whose salary is more than one lakh and fifty thousand rupees.

4.7.2 An employer, who has paid the tax on perquisites on behalf of the employee as per the provisions discussed in para 3.2 of this circular, shall furnish to the employee concerned, a certificate to the effect that the tax has been paid to Central Government and specify the amount so paid, the rate at which tax has been paid and certain other particulars in the amended Form 16.

4.7.3 The obligation cast on the employer under Section 192(2C) for furnishing a statement showing the value of perquisites provided to the employee is a crucial responsibility of the employer, which is expected to be discharged in accordance with law and rules of valuation framed there under. Any false information, fabricated documentation or suppression of requisite information will entail consequences thereof provided under the law. The certificates in Forms 16 shall be furnished to the employee by 15th June of the financial year immediately following the financial year in which the income was paid and taxes deducted. Through the Circular no. 12 of 2021 dated 25a1 June 2021, the due date for furnishing Form 16 for F.Y. 2020-21 to the employee was extended up to 31.07.2021. Form 12BA should be furnished to the employee by 30th April of the Assessment Year. If the person responsible for paying any income chargeable under the head salaries and therefore responsible for furnishing statement under Form 12BA and Form 16. as the case may be , fails to issue these certificates to the person concerned, as required by section 192(2C), he/she will be liable to pay, by way of penalty, under section 272A(2)(i), a sum which shall be Rs.100/- for every day during which the failure continues.

4.7.4 DDOs empowered to obtain evidence of proof or particulars of the prescribed claim (including claim for set-off of loss) under the section 192(2D)

DDOs have been authorized u/s 192 to allow certain deductions, exemptions or allowances or set-off of certain loss as per the provisions of the Act for the purpose of estimating the income of the assessee or computing the amount of tax deductible under the said section. The evidence /proof /particulars for some of the deductions/exemptions/allowances/set-off of loss claimed by the employee such as rent receipt for claiming deduction in I-IRA, evidence of interest payments for claiming loss from self-occupied house property, etc. is not available to the DDO. To bring certainty and uniformity in this matter, section 192(2D) provides that person responsible for paying (DDOs) shall obtain from the assessee evidence or proof or particular of claims such as House rent Allowance (where aggregate annual rent exceeds one lakh rupees); Leave Travel Concession or Assistance; Deduction of interest under the head Income from house property and deduction under Chapter VI-A as per the prescribed form 12BB laid down by Rule 26C of the Rules. Form 12BB is enclosed as Annexure Ha.

4.8 Mandatory Quoting of PAN or Aadhaar number as the case may be and TAN

4.8.1 Section 203A of the Act makes it obligatory for all persons responsible for deducting tax at source to obtain and quote the Tax deduction and collection Account Number (TAN) in the challans, TDS-certificates, statements and other documents. Detailed instructions in this regard are available in this Department’s Circular No.497 [F.No.275/118/ 87-IT(B) dated 01.10.1987]. If a person fails to comply with the provisions of section 203A, he/she will be liable to pay, by way of penalty, under section 272BB, a sum of ten thousand rupees. Similarly, as per Section 139A(56), it is obligatory for persons deducting tax at source to quote PAN or Aadhaar number as the case may be, of the persons from whose income tax has been deducted in the statement furnished u/s 192(2C), certificates furnished u/s 203 and all statements prepared and delivered as per the provisions of section 200(3) of the Act.

4.8.2 All tax deduetors are required to file the TDS statements in Form No.24Q (for tax deducted from salaries). As the requirement of filing TDS certificates along with the return of income has been done away with, the lack of PAN or or Aadhaar number as the case may be. of deductees is creating difficulties in giving credit for the tax deducted. Tax deductors are, therefore, advised to procure and quote correct PAN or Aadhaar number, as the case may be, of all deductees in the TDS statements for salaries in Form 24Q. Taxpayers are also liable to furnish their correct PAN or Aadhaar number as the case may be, to their deductors. Non-furnishing of PAN or Aadhaar number as the case may be, by the deductee (employee) to the deductor (employer) will result in deduction of TDS at higher rates u/s 206AA of the Act mentioned in para 4.9 below.

4.9 Compulsory Requirement to furnish PAN or Aadhaar by employee (Section 206AA)

4.9.1 Section 206AA in the Act makes furnishing of PAN or Aadhaar number as the case may be, by the employee compulsory in case of receipt of any sum or income or amount, on which tax is deductible. If the employee(deductee) fails to furnish his/her PAN or Aadhaar number, as the case may be, to the deductor, the deductor has been made responsible to make TDS at higher of the following rates:

i) at the rate specified in the relevant provision of this Act; or

ii) at the rate or rates in force; or

iii) at the rate of twenty per cent

4.9.2 The deductor has to determine the tax amount in all the three conditions and apply the higher rate of TDS. However, where the income of the employee computed for TDS u/s 192 is below taxable limit, no tax will be deducted. But where the income of the employee computed for TDS u/s 192 is above taxable limit, the deductor will calculate the average rate of income- tax based on rates in force as provided in sec 192. If the tax so calculated is below 20%, deduction of tax will be made at the rate of 20% and in case the average rate exceeds 20%, tax is to be deducted at the average rate.

4.10 Statement of deduction of tax under section 200(3) [Quarterly Statement of TDS1

4.10.1 The person deducting the tax (employer in case of salary income), is required to file duly verified Quarterly State;nents of TDS in Form 24Q for the periods [details in Table below] of each financial year, to the TIN Facilitation Centres authorized by Pr.DGIT (Systems) which is currently managed by M/s National Securities Depository Ltd (NSDL) or at www.incometaxindiaefiling.gov.in after registering as Deductor. Particulars of e-TDS Intermediary at any of the TIN Facilitation Centres are available at http://www.incometaxindia.gov.in and http://tin-nsdl.com portals. The requirement of filing an annual return of TDS has been done away with w.e.f. 1.4.2006. The quarterly statement for the last quarter filed in Form 24Q (as amended by Notification No. S.0.704(E) dated 12.5.2006) shall be treated as the annual return of TDS. Due dates of filing this statement quarter wise is as in the Table below:

TABLE: Due dates of filing Quarterly Statements in Form 240

| SI. No. |

Date of ending of quarter of financial year | Due date |

| 1 | 30th June | 31st July of the financial year |

| 2 | 30th September | 31″ October of the financial year |

| 3 | 31st December | 31 St January of the financial year |

| 4 | 31st March | 31st May of the financial year immediately following the financial year in which the deduction is made. |

(Note: The statement of Deduction of tax for the last quarter of the Financial Year 2020-21 required to be furnished on or before 31′ May 2021 under rule 31A of the Income Tax rules, was extended to 30th June 2021 vide Circular no. 9 of 2021 dated 20th May 2021, which was further extended to 15th July 2021 vide Circular no. 12 of 2021 dated 25’h June 2021.)

4.10.2 The statements in Form 24Q may be furnished in paper form or electronically under digital signature or along with verification of the statement in Form 27A or verified through an electronic process in accordance with the procedures, formats and standards specified by the Director General of Income-tax (Systems). The procedure for furnishing the e-TDS/TCS statement is detailed at Annexure VI.

4.10.3 Where the deductor is an office of the Government or is the principal officer of a company or is a person who is required to get his accounts audited under section 44AB in the immediately preceding financial year, or the number of deductee’s records in a statement for any quarter of the financial year are twenty or more, the deductor shall furnish the statement electronically under digital signature or along with the verification of the statement in Form 27A or verified through an electronic process [Rule 31A(3)].

4.11 Fee for default in furnishing statements u/s 200(3) of the Act

Under section 234E of the Act, if a person fails to deliver or caused to be delivered a statement within the time prescribed in section 200(3) in respect of tax deducted at source [on or after 1.07.2012] he/she shall be liable to pay, by way of fee a sum of Rs. 200 for every day during which the failure continues. However, the amount of such fee shall not exceed the amount of tax which was deductible at source. This fee is mandatory in nature and to be paid before furnishing of such statement.

4.12 Rectification of mistake in filing TDS Statement

A DDO can also file a correction statement for rectification of any mistake or to add, delete or update the information furnished in the statement delivered earlier.

4.13 Penalty for failure to furnishing statements or furnishing incorrect information (section 271H)

Under section 271 H of the Act, if a person fails to deliver or caused to be delivered a statement within the time prescribed in section 200(3) or furnishes an incorrect statement, in respect of tax deducted at source [on or after 1.07.2012], he/she shall be liable to pay, by way of penalty, a sum which shall not be less than Rs. 10,000/- but which may extend to Rs 1,00,000/-. However, the penalty shall not be levied if the person proves that after paying TDS with the fee and interest, if any, to the credit of Central Government, he/she had delivered such statement before the expiry of one year from the time prescribed for delivering the statement. At the time of preparing statements of tax deducted, the deductor is required to:

(i) mandatorily quote his tax deduction and collection account number (TAN) in the statement;

(ii) mandatorily quote his permanent account number (PAN) or Aadhaar number as the case may be, in the statement except in the case where the deductor is an office of the Government (including State Government). In case of Government deductors -PANNOTREQD to be quoted in the e-TDS statement;

(iii) mandatorily quote of permanent account number PAN or or Aadhaar number as the case may be. of all deductees;

(iv) furnish particulars of the tax paid to the Central Government including book identification number or challan identification number, as the case may be.

(v) furnish particular of amounts paid or credited on which tax was not deducted in view of the issue of certificate of no deduction of tax u/s 197 by the assessing officer of the payee.

4.14 TDS on Income from Pension

4.14.1 As per section 17(1)(ii) of the Income-tax Act, 1961, the term ‘salary’ includes pension. In the case of pensioners who receive their pension (not being family pension paid to a spouse) from a nationalized bank, the instructions contained in this circular shall apply in the same manner as they apply to Salary-income. The deductions from the amount of pension under section 80C on account of contribution to Life Insurance, Provident Fund, subscription to certain equity shares or debentures, etc., if the pensioner furnishes the relevant details to the banks, may be allowed. Necessary instructions in this regard were issued by the Reserve Bank of India to the State Bank of India and other nationalized Banks vide RBI’s Pension Circular (Central Series) No.7/C.D.R./1992 (Ref. CO: DGBA: GA (NBS) No.60/GA.64 (11CVL)-/92) dated the 27th April 1992, and, these instructions should be followed by all the branches of the Banks, which have been entrusted with the task of payment of pensions.

4.14.2 Under section 194P of the Act, the specified bank shall compute the total income of specified senior citizen and deduct income tax on the basis of rates in force. As per clause (2) of section 194P, the provisions of section 139 will not apply to specified senior citizen for the assessment year for which tax has been deducted. The specified senior citizen has been defined as an individual resident in India who has attained age of 75 years or more at any time during the Financial year and who is having income of the nature of pension and no other income except the income of the nature of interest received or receivable from any account maintained by such individual in the same specified bank in which he is receiving his pension income. Further the specified senior citizen has to furnish declaration in Form 12BBA (Rule 26D) to the specified Bank.

4.14.3 The declaration in Form no. 12BBA is to be furnished in paper form duly verified.

The specified bank shall, after giving effect to the deduction allowable under Chapter VI-A and rebate allowable under section 87A, compute the total income of such specified senior citizen for the relevant assessment year and deduct income-tax on such total income on the basis of the rates in force. The declaration and evidence for claiming deduction under Chapter VI-A shall be properly maintained by the Specified Bank and shall be made available to the Principal Chief Commissioner of Income-tax or Chief Commissioner of Income-tax, as and when required.

[Notification no. 99/2021/F.no.370142/11/2021-TPL dated 2-9-2021]

4.14.4 A specified Bank means a banking company which is a scheduled bank and has

been appointed as agents of Reserve Bank of India under section 45 of the Reserve Bank of India Act, 1934 (2 of 1934).

[Notification No. 98/2021/F.no. 370142/11/2021-TPL dated 2-9-2021]

4.15 Matters pertaining to the TDS made in case of Non-Resident

4.15.1 Under section 192 of the Act, any person responsible for paying any income chargeable under the head Salaries, shall at the time of payment, deduct income tax on the amount payable. This section does not distinguish between the salary paid to a resident or a non resident. Hence all payments taxable under the head Salaries are liable for deduction of TDS irrespective of the residential status of the recipient.

4.15.2 In respect of non-residents, the salary paid for services rendered in India shall be regarded as income earned in India. It has been specifically provided in the explanation to section 9(1)(ii) of the Act that any salary payable for rest period or leave period which is both preceded or succeeded by service in India and forms part of the service contract of employment will also be regarded as income earned in India.

4.15.3 Where Non-Residents are deputed to work in India and taxes are borne by the employer, if any refund becomes due to the employee after he/she has already left India and has no bank account in India by the time the assessment orders are passed, the refund can be issued to the employer as the tax has been borne by it [Circular No. 707 dated 11.07.1995].

5. Computation Of Income Under The Head “Salaries”

5.1 Income chargeable under the head “Salaries”

(1) The following income shall be chargeable to income-tax under the head “Salaries”:

(a) any salary due from an employer or a former employer to an assessee in the previous year, whether paid or not;

(b) any salary paid or allowed to him in the previous year by or on behalf of an employer or a former employer though not due or before it became due to him.

(c) any arrears of salary paid or allowed to him in the previous year by or on behalf of an employer or a former employer, if not charged to income-tax for any earlier previous year.

(2) For the removal of doubts, it is clarified that where any salary paid in advance is included in the total income of any person for any previous year it shall not be included again in the total income of the person when the salary becomes due.

Any salary, bonus, commission or remuneration, by whatever name called, due to, or received by, a partner of a firm from the firm shall not be regarded as “Salary”.

5.2 Value of Perquisites as per Rule 3

The value of perquisites provided directly or indirectly by the employer to the employee or to any member of household of employee, for the purpose of computing the income chargeable under the head “Salaries” for that employee shall be determined on the basis of Rule 3 of the Income-tax Rules 1962. The provisions of Rule 3 are as follows: –

A. Residential Accommodation provided by the employer [Rule 3(1)]

As per rule 3 of the Income-tax Rules 1962, “accommodation” includes a house, flat, farm house or part thereof, hotel accommodation, motel, service apartment, guest house, a caravan, mobile home, ship or other floating structure. The value of perquisites for unfurnished, furnished or hotel accommodation provided by different category of employers is detailed below : –

a) Rent-free unfurnished accommodation: The accommodation is divided into two categories:

(i) Accommodation provided by the Central Government or any State governments:

The value of perquisite shall be equal to the license fee determined by the Central Government or any State Government as reduced by the rent actually paid by the employee.

(ii) Accommodation is provided by any other employer:

The valuation of perquisite in respect of accommodation would be at prescribed rates, as discussed below:

- Where the accommodation provided to the employee is owned by the employer:

| SL No | Cities having population as per the 2001 census | Value of the Perquisite |

| 1 | Exceeds 25 lakh | 15% of salary |

| 2 | Exceeds 10 lakhs but does not exceed 25 lakhs | 10% of salary |

| 3 | For other places | 7.5 % of salary |

- Where the accommodation so provided is taken on lease/ rent by the employer: The value 30 of perquisite is lower of the two: –

(i) 15% of the salary or

(ii) the actual amount of lease rental paid or payable by the employer, as reduced by any amount of rent actually paid by the employee.

For the purpose of calculation of value of perquisite under rule 3, the term ‘Salary’ includes the pay, allowances, bonus or commission payable monthly or otherwise or any monetary payment, by whatever name called from one or more employers, as the case may be, but does not include the following:

(a) dearness allowance or dearness pay unless it enters into the computation of superannuation or retirement benefits of the employee concerned;

(b) employer’s contribution to the provident fund account of the employee;

(c) allowances which are exempted from payment of tax;

(d) the value of perquisites specified in clause (2) of section 17 of the Income-tax Act;