Introduction:

Hello friends, this time I got opportunity from my new office to prepare on a seminar for exchanging thoughts on “Reopening of assessment” in study circles. I endeavour this attempt and left no stone unturned to bring out in depth analysis and research on this topic. This blog covers an extensive analysis on the reassessment provisions in light of landmarks judgement which will help professional to face dispose the litigations hastily. I am not inserting bare sections here to increase the size of blog, it is written keeping in mind to provide less, solid and crux content about the matter. It includes gist if case laws on section 147, few riders which can twist anyone mind along with plethora of recent rulings on 147 at the end to left your mind tranquil. Let’s start the journey!

The provisions of section 147 empower the Assessing Officer, to reopen an assessment if he has “reason to believe” that income has escaped assessment. The important words under section 147 are ‘has reason to believe’ and these words are stronger than the words ‘is satisfied’.

Reopening can be done on QUIPIDITY of assessee & STUPIDITY of AO.

Bare Section:

Income escaping assessment.

147. If the[Assessing] Officer[has reason to believe] that any income chargeable to tax has escaped assessment91for any assessment year, he may, subject to the provisions ofsections 148 to 153, assess or reassess91 such income and also any other income chargeable to tax which has escaped assessment and which comes to his notice subsequently in the course of the proceedings91 under this section, or recompute the loss or the depreciation allowance or any other allowance, as the case may be, for the assessment year concerned (hereafter in this section and in sections 148 to 153 referred to as the relevant assessment year) :

Page Contents

- Let’s have brief understanding of the section 147 word by word:

- I. “A.O. has Reason to Believe”

- II. Recording of Reasons by the A.O.:

- III. Request for Reasons Recorded, Filing Objections & its disposal

- IV. “Change of Opinion”

- V. Income chargeable to tax has escaped assessment

- VI. Explanation-2 to Section 147 (Deemed Income escaped )

- VII. Explanation -3 to Section 147

- VIII. 1st Proviso to the section 147:

- IX. 2nd Proviso to Section 147:

- X. 3rd Proviso to Section 147

- XI. Explanation -1

- Section-148 – Issue of Notice

- Section-149, 150, 151 & 153

- Some Judicial decisions on Section 147 (Unreported):

- Practical Tax management Issues

Let’s have brief understanding of the section 147 word by word:

I. “A.O. has Reason to Believe”

- There should be ‘reasons’ and ‘belief’. “Reasons” refer to the cause like document, statement, third party confirmation etc and “belief” refers to the conclusion. The “reason to believe” is different from “reason to suspect” or from “to have an opinion”.

- Belief of A.O. only (Not of CIT/ex-officer) SheoNarain v ITO 176 ITR 352, Hyoup Food and Oil Industries Ltd. vs. ACIT (2008) 307 ITR 115 (Guj)

- The basis of the belief should be discernible from the material on record, which was available with the Assessing Officer, when he recorded reason.

- Live link or close nexus between material obtained and formation of belief. ITO v Lakshmani 103 ITR 437 (SC).

- Information to form Reason to believe available at the time of reopening not subsequent to it. CIT Vs Smt. Paramjit Kaur 311 ITR 38 (P&H)

- No New Tangible Material even within 4 years, reopening not valid. NDT systems v. ITO 363 ITR 603

INVALID Reason to Believe

- In ACIT Vs. Dhariya Construction Co. (2010) 328 ITR 515 (SC) opinion of the DVO per se is not information for the purposes of reopening assessment under Section 147 of the Act.

- In Income Tax Officer Vs. Saradbhai M. Lakshmi, (2000) 243 ITR 1, the Supreme Court held that the decision of the High Court would constitute information and the initiation of reassessment proceeding on the basis of the decision of the High Court has been justified.

- Cannot make fishing inquiries. Ajanta Pharma Ltd. v. ACIT (2004) 267 ITR 200

- Unaccounted expenditure on renovation of premises at the time of survey in a subsequent year, not a reason to believe that such discrepancies existed in earlier years also. CIT v. Gupta Abhushan (P) Ltd. (2008) 312 ITR 166 (Del)

- Applying one of the different legally permissible methods to assess larger income. CIT v. Simon Carves Ltd.105 ITR 212 (SC). Eg. Calculation Of ALP.

- Statement by an unconnected person. PrafulChunilal Patel vs. M.J. Makwana, ACIT (1999) 236 ITR 832 (Guj)

- Where only a s. 143(1) Intimation is passed, no reopening merely to “scrutinize” the return or “verify” the expenditure. Inductotherm (India) v. DCIT (2013) 356 ITR 681 (Guj).

- Notice enquiring into source of funds for purchasing flat by assessee not a reason to issue notice of 147. CIT v. Smt. Maniben Valji Shah (Bom)

- Intimation cannot be reopened without “fresh material”. Reason to believe cannot have separate different meanings for 143(3) & 143(1)

- Mismatch of Income with TDS Certificates. (Meheria Reid & Co. v. ITO 151 TTJ 545)

- Reopening solely on basis of objection of audit party without application of mind by the AO is not valid. (JagatJayantilal Parikh v. DCIT) (2013) 355 ITR 400 (Guj-HC). You

- Opinion of audit party on a point of law cannot be regarded an information. Indian & Eastern Newspaper Society v. CIT, (1979) 119 ITR 996.

- No reassessment can be made on the basis of Tax Audit Report/Accounts/Transfer pricing report because no new tangible material come into possession of AO. CIT Vs Modipon Ltd., reported in 2011 334 ITR 106.

- CHANGE OF OPINION (Discussed infra)

VALID Reason to Believe

- Lata Chouhan Vs. ITO, (2010) 329 ITR 400 (MP) material unearthed during survey can be the basis of reassessment

- EssEss Kay Engineering Co. P. Limited Vs. CIT, (2001) 247 ITR 818, SC held that the reopening of the assessment on the basis of finding of fact, made on the basis of the fresh materials in the course of assessment of the subsequent assessment year is valid.

Hence it is pertinent to note that for valid reopening of assessment REASON TO BELIEVE is one of the core ingredients. There must be something which is really escaped from the assessment, there must be NEW tangible material, and it should not be change of opinion. Mere suspicion of escapement of income does not give power to AO to put the gun on assessee. Section never talks about any procedural requirements but as law evolved in past years a practise has been developed and laid down by the apex court (GKN Driveshafts) for the sake of natural justice which is to be mandatorily followed during the course of reopening. This procedural requirement includes the “Recording of Reasons”, “Requesting for reasons and disposal of its objection”. Let’s discuss this in the light of some judgements.

II. Recording of Reasons by the A.O.:

♠ In Hindustan Lever Limited Vs. R.B. Wadkar, Asst. Commissioner of Income Tax, (2004) 268 ITR 332 (Bom), a Division Bench has opined the followings with respect to recording of reasons which should form the unimpeachable code for the Assessing Officers:

- The reasons are required to be read as they were recorded by the Assessing Officer;

- No substitution or deletion is permissible;

- No additions can be made to those reasons;

- It is for the Assessing Officer to disclose and open his mind through reasons recorded by him;

- It is for the Assessing Officer to reach to the conclusion as to whether there was failure on the part of the assessee to disclose fully and truly all material facts necessary for his assessment for the concerned assessment year;

- The reasons recorded should be clear and unambiguous and should not suffer from any vagueness;

- The reasons recorded should be self explanatory and should not keep the assessee guessing for the reasons;

- Reasons provide the link between conclusion and evidence;

- The reasons must be based on evidence;

- The Assessing Officer, in the event of challenge to the reasons, must be able to justify the same based on material available on record;

- He must disclose in the reasons as to which fact or material was not disclosed by the assessee fully and truly necessary for assessment of that assessment year, so as to establish the vital link between the reasons and evidence;

- That vital link is the safeguard against arbitrary reopening of the concluded assessment;

- The reasons recorded by the Assessing Officer cannot be supplemented by filing an affidavit or making an oral submission;

III. Request for Reasons Recorded, Filing Objections & its disposal

- Reasons need not accompany the notice.

- After filing return, request for copy of reasons recorded to be made by assessee.

- If Assessee desires, objections to reopening can be filed.

- A comprehensive order disposing off objections.

- If AO agrees with objections, he ceases to have jurisdiction on reassessment. Shri RatanSingh 306 ITR 343 (Raj.), Atlas Cycle Industires 180 ITR 319 (P&H).

- Copy of reasons recorded to be given by the AO – if AO fails to provide copy of reasons recorded till completion of assessment, reassessment is invalid CIT v. VSNL 340 ITR 66 (Bom)

- Disposal of objections by a speaking order GKN Driveshafts (India) Ltd. 259 ITR 19 (SC)

- AO to wait for 4 weeks to begin assessment after disposing off the objections. Asian Paints Ltd. v. DCIT 296 ITR 1 (Bom)

- Disposal of objections to be linked with recorded reasons. Reasons recorded on the basis of survey/search evidences subsequently disposed off by referring to investigation carried out by sales tax department is unsustainable in law. Interestingly Court has given fresh opportunity to AO to dispose off the objections keeping in mind the recorded reasons. (Pranshukhlal Bros. v. ITO WP lodging no. 2124 of 2014 dt 20/08/2014, (Bom-HC)

- Reassessment order passed by the AO without supplying reasons recorded though specifically asked by the assessee is invalid. (CIT v. Videsh Sanchar Nigam Ltd. (2012) 340 ITR 66 (Bom.-HC).

- In Acrylic Manufacturing Co. v. CIT 308 ITR 38 (P&H) reasonable time for furnishing reasons is the time within which department can issue the notice u/s 148.

- Failure to comply with the procedure prescribed in K.N. Drive Shaft (India) Ltd. vs. ITO 259 ITR 19 (SC) renders the assessment order invalid & void ab initio. (Suresh Chandra v. ITO 44(1) (Delhi-ITAT) [2015] IT no. 3061/2012 (Unreported)

- Garden Finance Ltd. v. ACIT 268 ITR 48 (Guj) (FB) held that the assessee preferably file a revision before the Commissioner u/s 264 first then he can file writ petition. This is the single decision which is not in terms with the section said. How someone can file revision appeal when the original order itself is not passed.

Rider-1

One question which may arise in mind is what is the recourse available to assessee after disposal of objections?

Ans: The only option which seems to available is writ petition. Another view is invited.

IV. “Change of Opinion”

Reopening can never be done on the basis of change of opinion. AO cannot stand on platform and catch two different trains together of same opinion, neither he can switch the train after getting inside of one train. There are certain cases discussed below to give you an idea about Change of Opinion.

- CIT v. Kelvinator of India (2010) 320 ITR 561 (SC) is one of the crucial judgement as regards to the Change of opinion wherein it is held that:

- Reappraisal of same facts/documents/information means change of opinion. AO has no power to review his order.

- Order which has been passed purportedly without application of mind would itself confer jurisdiction upon the Assessing Officer to reopen the proceeding without anything further, the same would amount to giving premium to an authority exercising quasi-judicial function to take benefit of its own wrong.

- Change of Opinion v. No Opinion 143(1) (ACIT v.s. Rajesh Jhaveri(2006)291 ITR 500 (SC), however reopening relying on information already on record and not on basis of tangible material, not permitted. (S. Ranjhit Reddy v. DCIT 161 TTJ 316) (Hyd).

- Deduction u/s 80IA allowed earlier, reopen to consider certain aspects is change of opinion. Agrawal JV ITO 257 CTR 112 (Guj).

- Business loss assessed in 143(1), later on reopened to treat Speculative Loss. Held that there was “nothing new” which had come to the notice of the revenue , it is a “mere relook” which was not permissible. (ACIT vs.ICICI Securities Primary Dealership Ltd.) 348 ITR 299 (Bom)

- Reopening based on auditor’s note in his audit report. NYK Lines (India) Ltd. v. DCIT [2012] 206 Taxmann.com 135 (Bom)

- Change in rate of depreciation from 25% to 20% is mere change of opinion. Aventis Pharma Ltd. vs. ACIT (2010) 323 ITR 570 (Bom)

- Initially holding transfer of equity shares as capital gain but on reassessment as business. Ritu Investments P. Ltd. v. DCIT 345 ITR 214.

- No addition made by AO during original assessment on Issue regarding addition of amount of deferred taxation for computing book profits u/s. 115JB being satisfied with the explanation of the assessee. Reopening of assessment on the very same issue in absence of any fresh material invalid. J. Pharmaceuticals Ltd vs. CIT (2008) 297 ITR 119 (Bom)

- Reopening on the basis of internal audit amounts to change of opinion hence not a valid reason. CIT v. The Simbholi Sugar Mills Ltd. 2011-TIOL-293-HC-DEL-IT

- 143(3) assessment order is not a scrap of paper & AO is expected to have applied his mind. Reopening on ground of “oversight, inadvertence or mistake” is not permissible. CIT.v. Jet Speed Audio Pvt Ltd (Bombay High Court) (Unreported)

- Reopening cannot be done on carelessness of AO. New Excelsior theatre v ITO 185 ITR 158.

- Reopening of assessment to deny Section 80IB is without jurisdiction if no failure of Assessee to disclose information during Original Assessment – International Flavours and Fragrances India Private Limited Vs DCIT (Madras High Court); W.P.Nos. 309 & 44102 of 2016; 19/05/2020

- On mere change of opinion, the concluded assessment cannot be reopened – Akshaya Souharda Credit Cooperative Limited Vs ITO (ITAT Bangalore); ITA No. 2574/Bang/2019

- No section 147 notice based on material already presented during section 143(3) assessment – Audhut Timblo Vs ACIT (Bombay to Goa High Court); W.P. No. 166 of 2007; 27/11/2019

- Reopening of assessment without bringing any fresh material on record is not justified – Chordia Buildcon Pvt. Ltd. Vs DCIT (ITAT Jaipur); ITA No. 64/JP/2020

- Reassessment u/s 147 without any tangible material to support escapement of income not justified – SPR & RG constructions Pvt. Ltd. Vs ACIT (ITAT Chennai); ITA No. 2334/Chny/2019; 25/02/2020

Rider-2

Website of Sales tax constitutes ‘information’ for reopening?

- Mere information on the website may not constitute information, however if, based on the same, the return of the assessee is verified and after recording the reasons the notice is issued it may be valid information.

- General Hawala Case unearthed, same cannot be used by the AO against a particular assessee unless there is a confessional statement against the assessee by the Hawala Operator. 92 ITD(Asr)(SB) 85, 98 ITD(Asr)(SB)227, 97 TTJ(Jd)573, 329 ITR(Del)110, 248 CTR(Del)33, 325 ITR(Del)285, 132 TTJ(Nag)490

- If the A.O. re-opens an assessment simply on the basis of satisfaction recorded by some other authority like Sales Tax, Excise or DG(Inv.) and does not record his own satisfaction re-opening held as bad. 313 ITR(Raj)231, SLP dismissed(St)27, 135 ITD(Ahd)1, 220CTR Mad 335 & (Raj)361 & (Del)531 125 TTJ(Del)816, 236 CTR(Del)362

- Notice issued after 4 years on the basis of information supplied by DIT(Inv.) about bogus entries, No application of his own mind by AO- Invalid. (CIT v. Kamdhenu steel and alloys Ltd. & Ors. (2012) 248 CTR 33.

Conclusion: It is the hottest topic as many cases are reopened on this basis. What is more important for reopening on this basis is the facts of case. AO cannot merely reopen the case on the basis of frivolous information received from any department, he has to apply his mind and made his own finding, he cannot rely on the finding of others. Second important thing is how reasons are recorded. If AO want to successfully reopen the case then reasons must be drafted appropriately which clearly indicates that it is the valid Reason to Believe?

Notice issued beyond 4 years by forming belief on the basis of information that the bills produced is not genuine, valid reopening. (Nickunj Enterprises Pvt. LTd. v. ACIT (2014) 107 DTR 69 (Bom) (HC).

Rider-3

Can reopening be done on the basis of AIR Information?

- Second hottest topic of the year is reopening on the basis of information emitting from AIR (Annual information return). Income tax is keenly interested in looking into the pockets of assessee that how much he is spending from Credit card, how much cash is deposited in Bank and many others information which forms part of AIR. Can AO do reopening on such basis? Well in my opinion he cannot do so, because on this information he has merely just a suspicion that income has escaped assessment, he is not sure that income escaped or not. It was so hard to find decision on this recent topic, but still I manage to find few which are given in next bullet.

- Addition made solely on the basis of AIR information is not sustainable in law vide ANS Law Associates, in ITA No. 5181/M/2012 dated 5.12.14 (Mum)/ DCIT vs. Shree G. Selva Kumar” in ITA No.868/Bang/2009 decided on 22.10.10 and another case in the case of “Aarti Raman vs. DCIT” in ITA No.245/Bang/2012 decided on 05.10.12

Rider-4

Can Later decisions of Supreme Court & high court is valid reason to reopen the assessment?

- Supreme court decision cannot be the basis for Reopening: The ITO cannot seek to reopen an assessment under section 147 on the basis of the Supreme Court decision in a case where assessee had disclosed all material facts. Indra Co. Ltd. V. ITO (1971) 80 ITR 559 (Cal.), 305 ITR 156

- Where revenue did not file appeal against an order granting relief to the assessee, the assessment cannot be reopened on same issue following a supreme court judgement. (CIT v Ramachandra Hatcheries 305 ITR 117)

- Further it is also held that reopening on the basis of reversal of law by higher court is also not valid reason for belief in case assessment is reopened after 4 years. The Apex court has held that change in legal position due to reversal of judgement not a valid ground when the assessment is finalised on the basis of law in force at the time of assessment. (DCIT v. Simplex Concrete Piles (India) Ltd.)

- Subsequent High court decision – beyond 4 year Discloure of complete facts. Reopening bad in law. Subsequent decision does not mean failure on part of an assessee to disclose fully and truly all material facts. SESA Goa ltd v/s CIT (2007) 294 ITR 101 BOM.

Conclusion: Yes it is possible if within the time frame of 4 years. Beyond 4 years only if failure is on part of assessee.

V. Income chargeable to tax has escaped assessment

This was all about R2B which we have discussed in depth, now second precondition for reopening is that there must be income chargeable to tax and which should have escaped assessment. That means the AO cannot reopen the assessment in case of exempt income. There are certain cases given under explanation 2 where it would be deemed assumed that income has escaped the assessment discussed infra.

- No reopening for exempt income.

- It is immaterial that the income was charged or included in some other assessment. (CIT v Vednath 8 ITR 222)

- No Reopening if Tax Neutral, for example in case of inclusion & exclusion of VAT & CENVAT which is have no effect on P&L. w. Givaudan flavours India Pvt. Ltd. DCIT 2011-TIOL-195-ITAT-MUM

- It is immaterial that the income was charged or included in some other assessment. (CIT v Vednath 8 ITR 222)

VI. Explanation-2 to Section 147 (Deemed Income escaped )

- No return of income is filed.

- Return of income has been furnished by the taxpayer but no assessment has been made and it is noticed by the AO that the taxpayer has understated the income or has claimed

- excessive loss, deduction, allowance or relief in the return.

- Failed to furnish a report of international taxation u/s 92E.

- Where an assessment has been made, but:

- income chargeable to tax has been under assessed; or

- income has been assessed at low rate; or

- income has been made the subject of excessive relief; or

- excessive loss or depreciation allowance or any other allowance has been computed.

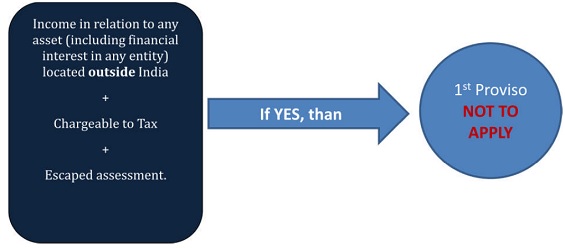

- Have any asset (including financial interest in any entity) located outside India.

The section deems that there will be escapement in aforesaid cases. However, for reopening there should be “reason to believe” as well. There must be certain information leading to belief that income has escaped assessment. By the way of explanation the AO itself not got any blanket power to reopen the assessment. Even to invoke explanation information has to be fresh from outside. CIT Vs. Feather Foam 296 ITR 342 (Del.)

Rider-5

Can AO reopen the assessment on the basis of Audit Objection?

- It has been held by the Supreme Court in the case ofIndian & Eastern Newspaper Society v. CIT,(1979) 119 ITR 996 that an opinion of audit party on a point of law cannot be regarded an information within the meaning of S. 147 and it cannot lead to valid initiation of reassessment proceedings.

- On the contrary Audit note is information P. V.S beedies P Ltd- 237 ITR 13(SC).

- Reopening solely on basis of objection of audit party without application of mind by the AO is not valid. (JagatJayantilal Parikh v. DCIT) (2013) (guj-HC)

VII. Explanation -3 to Section 147

99[Explanation 3.—For the purpose of assessment or reassessment1 under this section, the Assessing Officer may assess or reassess the income in respect of any issue, which has escaped assessment, and such issue comes to his notice subsequently in the course of the proceedings under this section, notwithstanding that the reasons for such issue have not been included in the reasons recorded under sub-section (2) of section 148.]

Assess or Reassess such Income AND ALSO any other Income

- Reassessment can be done N No. of times. Kunal Organic P. Ltd. 362 ITR 530 (Guj.)

Section 147 is much discussed provision in law and while applying one has to read each and every word carefully. The section lays the diplomatic view by using word AND ALSO twice which is as below:

Explanation 3 is inserted recently few year back to remove the hinder cause to happen for AO to reopen the assessment. Before this explanation even though in main section it is written that AO can reassess such income and also, he was unable to reassess because assessee object that he cannot reassess the income for which no reasons are recorded. Thereafter this explanation 3 is introduced which empower the AO to reassess such income even without recording reasons. The important thing to note that AO can reassess other income now, but he cannot make sole addition on such other income assessed unless there is any addition on income for which reasons are recorded. Let’s see how Bombay high court decision under CIT vs. Jet Airways (I) Ltd. (2011) 331 ITR 236 (Bom) sets the right balance between the above twin aspects:

a) The words “and also” indicate that reassessment must be with respect to the income for which the AO has formed an opinion and also in respect of any other income which comes to his notice subsequently. However, if the AO is satisfied with the objections of assessee as regards to the issue for which reason is recorded and does not assess the income which was the basis of the notice, it is not open to him to assess income under some other issue independently; the words ‘and also’ are used in a conjunctive and cumulative sense indicating that the other escaped incomes can be assessed only in conjunction with the escaped incomes on the basis of which notice us 148 had been issued.

b) Explanation 3 to s. 147 was inserted to supersede the judgements inVipinKhanna 255 ITR 220 (P&H) &Travancore Cements 305 ITR 170 (Ker) where it was held that the AO could not assess income in respect of issues unconnected with the issue for which the notice was issued. However, Explanation 3 does not affect the judgements in Ram Singh 306 ITR 343 (Raj) & Atlas Cycle Industries 180 ITR 319 (P&H) where it was held that if the AO accepted that the reasons for which the notice was issued were not correct, he would cease to have jurisdiction to proceed with the reassessment;

c) Explanation 3 lifts the embargo inserted by judicial interpretation on the making of a s. 147 assessment in respect of items not referred to in the recorded reasons. However,it does not and cannot override the substantive part of s. 147 that the income for which the notice was issued must be assessable.

d) Hence this judgement clearly states that AO has vested with powers (to assess other income) but within the Sphere of the authority i.e. the limits within which the vested power can be exercised.

(Hotel Regal International &Anr. Vs. ITO (2010) 320 ITR 573 (Cal.), ITO v Bidbhanjan Investment & Trading CO (P ) Ltd ( 2011) 59 DTR 345 ( Mum) (Trib))

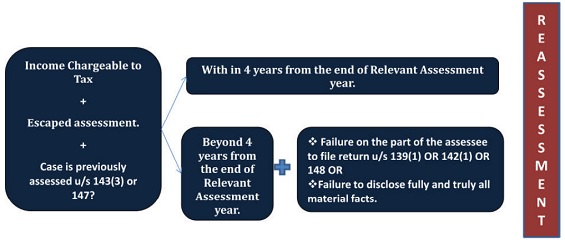

VIII. 1st Proviso to the section 147:

Analysis:

First Proviso to the section 147 deals with the deadline of the reopening of the assessment. Let’s understand with Flow chart what it says:

- No reopening beyond 4 years until & unless Failure on part of assessee.

- On failure on part of AO & to cover up own faults, no reopening. DCIT v. Hyundai Motor India Ltd. 148 ITD 333 (Chen).

- No benefit of proviso if return not submitted on time pursuant to Section 148 notice. Therefore return must be submitted timely.

What is the most important part here for reopening beyond 4 years is “FAILURE ON PART OF ASSESSEE TO DISCLOSE FULLY AND TRULY ALL MATERIAL FACTS”.

Let’s understand what it means:

- Deduction u/s 80IB once allowed after considering audit report in Form 10CCB and other details during the assessment u/s 143(3) Purity Techtextile (P) Ltd. v. ACIt (2010) 325 ITR 49 (Bom.)

- Claim for Bad debts allowed during original assessment after receiving explanation claim was allowed, later on reopening made on bad debts is invalid. Yash Raj Films P. Ltd. vs. ACIT (2011) 332 ITR 428 (Bom)

- Despite “Wrong Claim”, reopening invalid if failure to disclose not alleged. There is a well known difference between a wrong claim made by an assessee after disclosing all the true and material facts and a wrong claim made by the assessee by withholding the material facts i.e. False Claim. Titanor Components Limited vs ACIT (2011) 60 DTR 273 (Bom.)(HC)

- Assessee has to only disclose facts, no need to guide AO about legal inferences that what is right or what is wrong. Calyon Bank v. DCIT 54 SOT 111 (Mum) (URO) (2012).

- Adhoc expenses claimed which is withdrawn during the assessment u/s 143(3) cannot be reopened within 4 years by forming belief that it is unexplained expenditure u/s 69. No new tangible material. CIT v. Amitabh Bachchan [2013] 349 ITR 76

IX. 2nd Proviso to Section 147:

This proviso states the case where reopening can be done beyond 4 years without any failure on part of assessee.

X. 3rd Proviso to Section 147

This proviso prescribes that AO cannot reopen the case to assess the income chargeable to tax escaped the assessment if that income is subject matter of an appeal or revision.

XI. Explanation -1

XI. Explanation -1

Explanation 1.—Production before the Assessing Officer of account books or other evidence from which material96 evidence could with due diligence have been discovered by the Assessing Officer will not necessarily96 amount to disclosure within the meaning of the foregoing proviso.

Explanation 1 is inserted in the section with the purpose to elaborate lines written at the end of the first proviso to the section 147 i.e. “Omission of failure…..to disclose fully and truly all material facts”. This explanation empowers AO to reopen the case beyond four years by taking the advantage of this explanation and stating that there was not proper disclosure by the assessee during assessment hence it is the failure on part of assessee. But one must have to note the important words in explanation i.e. “not necessarily” which means every time AO cannot play hide and seek behind the curtains of this explanation.

- The expressions‘ material fact’ refers only to primary facts.

- This explanation is inserted to support the basic provision stated in main clause “Omission of failure…to disclose facts..” which empowers the AO

- Where the assessee has disclosed all material primary facts, proceedings u/s 147 cannot be taken if the AO fails to draw the correct legal inference from such facts or fails to pursue the matter appropriately. (CIT v KrishnakuttyMenon 181 ITR 237)

- Words “not necessarily” places the burden equally on the AO to exercise due diligence in examining the record (account books or evidence) produced before him in the light of declarations made in the return or responses (to the notices, questionnaire etc.) Donaldson India Filters Systems Pvt Ltd.v.DCIT (Delhi HC) (Unreported)

Section-148 – Issue of Notice

Introduction:

Reopening of the assessment can be done only when proper notice has been issued and served. Issue of notice u/s 148 is mandatory and if not properly issued, reopening is illegal and hence whole reassessment proceeding are vitiated. It is pertinent to note that notice u/s 143(2) says “Notice to be Served” on assessee while notice u/s 148 requires notice to be “Issued”, actual service is irrelevant. However for completion of reassessment proceedings section 153 use the word “Served” discussed supra.

- Section 148 Notice has to specify the period in which return is filed.

- Filing of return, whether issue of notice u/s 143(2) necessary? (ITO v. D.D. Ahuja 158 TTJ 54). Reference to Section 139(1).

- AO to record reasons before issuing notice u/s 148.

- “To issue” – Meaning– Notice signed on 31/3/2010 sent to speed post on 7/4/2010 – Notice issue after Six years for the relevant Kanubhai M. Patel (HUF) vs. HIren Bhatt (2010) 43 DTR 329 (Guj.)

- Issue of 2nd Notice during pendency of proceedings consequent to 1st SB Jain v. ITO [1972] 83 ITR 104 (SC).

- Can notice u/s 148 be issued during the pending period u/s 143(2). CIT v/s. Qatalys Software Technology (2009) 308 ITR 249 (Mad), CIT vs. TCP Ltd. (2010) 323 ITR 346.

- Notice and order on objections cannot be challenged in a Writ Petition. Kalanithi Maran v. JCIT (2014) 107 DTR 1 (Mad) (SC)

- Above judgment is explained in Aroni Chemicals v. ACIT (Bom) adjudicatory facts v. jurisdictional facts

- Two Notices on same ground not permissible. (Kunal Organics P. Ltd. v. DCIT (2014) 362 ITR 530 (Guj) (HC).

- Composite notice u/s 148 for different years, invalid. Mohd. Ayub v. ITO 254 CTR 314.

Section-149, 150, 151 & 153

I. Time Limit for issue of Notice

Introduction: Section 148 prescribes about the Notice for commencing the reassessment proceedings while section 149 prescribes the time limit for issuing notice. It is the most important part as we know that if the notice is invalid than reassessment is also invalid. Section 151 put the precondition to the notice u/s 148 that it cannot be send in some cases without obtaining the previous approval of the superior officers. And at last section 153 provides the time limit for completion of the reassessment proceedings.

Analysis:

Let’s have a combined summary of the above provisions which prescribes the time limit along with the prescribed conditions for reopening of the assessment.

*In 2nd point i.e. when Income chargeable to tax escaping assessment should not be less than Rs.1,00,000/-, it is pertinent to note that Notice of reopening u/s 148 should contain the amount of escapement so that one can know how A.O. came to conclusion that this case falls in this situation.

* In last point ‘Indefinite period’ word finding has important meaning. One has to keep in mind that observation of court is only in respect of specific alleged year.

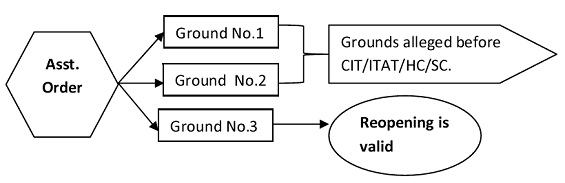

Indefinite Extended Period not to apply in:

- This section will not apply if at the time when the order (Which was subject matter of the appeal/revision/ reference) was passed the time limit for the issue of notice u/s 148 had already expired.

Example:

Asst order passed on 31.03.2020 for AY 2017-18. Appeal filed to CIT(A). Matter finally decided by ITAT on 25.03.2016, holding that the addition done by AO should be done in AY 2002-03, Whether AO can reopen the assessment for AY 1999-00 on 25.03.2016?

In given situation, on 31.03.2020, reopening for 1999-00 could not have been initiated as 6 years had already elapsed. Hence on 25.03.2016, AO cannot reopen AY 2002-03.

II. Time limit for completion of the reassessment (Section 153):

1 year from the end of the financial year in which notice u/s 148 is “SERVED”. It is 2 year if reference is made to TPO u/s 92CA.

III. Relevant case laws regarding Approval & sanction (Section 151):

- Record “Satisfaction” on the file put up for approval.

- CIT having mechanically granted approval for reopening of assessment without application of mind, the same is invalid and not sustainable. German Remedies Ltd vs. Dy. CIT (2006) 287 ITR 494 (Bom).

- Merely affixing a ‘yes’ stamp and signing underneath suggested that the decision was taken by the Board in a mechanical manner as such, the same was not a sufficient compliance under section 151 of the Act. Central India Electric Supply Co. Ltd. vs. ITO (2011) 51 DTR 51 (Del.)

- Merely stating “Approved” is not sufficient sanction of CIT and renders reopening void. Commissioner has to apply mind and due diligence before according sanction to the reasons recorded by the AO. ITAT Delhi in ITO10(3) v. Direct Sales (P) Ltd. 2015.

- Sanction of commissioner instead of JCIT renders reopening is void. Ghanshyam K. Khabrani v. ACIT (2012) 346 ITR 443 (Bom)(High Court)

- Non-mentioning in the reasons that approval has been obtained from the CIT vitiates the reopening and become bad in law. GTL Limited.v.ACIT (ITAT Mumbai) (Unreported)

Rider-6

Can Assessee make further claims during the reassessment?

- The income for purposes of reassessment cannot be reduced beyond the income originally assessed, new claim or deduction by assessee cannot be allowed in reassessment proceedings. (CIT v Sangeetha Granites Ltd. 326 ITR 324 applying sun engineering)

- Contrary to that under VishwanathProducts (2008) 117 TTJ 549 it is held that fresh deduction can be claimed subject to it does not reduced below the originally assessed income. It is held that it is fresh deduction and asssessee is not reagitiating the the old issues.

Rider-7

Can Reassessment is available for benefit of revenue only?

- Since the proceedings under section 147 are for the benefit of the revenue and in the assessee, and are aimed at gathering the escaped income of the revenue and an assessee and are aimed at gathering the escaped income of an assessee the same cannot be allowed to be converted as revisional or review proceedings at the instance of the assessee, thereby making the machinery workable. CIT vs. Sun Engineering Works (p.) Ltd. (1992) 198 ITR 297 (SC)(Asst yr 1960-1962)

- Proceeding under section 147 are for the benefit of the revenue and not the assessee and hence the assessee cannot form the be permitted to convert the reassessment proceedings as his appeal or revision in disguise and seek relief in respect of items earlier rejected, or claim relief inrespect of items not claimed in the original assessment proceedings unless relatable to the escaped income and reagitate concluded matters. Allowance of such a claim in respect of escaped assessment in the case of reassessment has to be limited to the extent to which they reduce the income to that originally assessed. Sudhakar S. Shanbhag V. ITO (2000) 241 ITR 865 (Bom.) (Asst yr 1987-1989)

- Assessee having not claimed deduction under section 80HHC, in its return because it had only income from other sources and no business income, claim made in the revised return by filing audit report under section 147 due to disallowances under section 43B is upheld. ITO vs. Tamil Nadu Minerals Ltd. (2010) 124 ITD 156 (Chennai)(TM).

Rider-8

Can RETROSPECTIVE AMENDMENT is valid reason to reopen the assessment?

Reopening WITHIN 4 Years – YES

- ACIT V Parixit Industries (P.) Ltd. SUPREME COURT OF INDIA, SLP Dismissed CC.NO. 15455 OF 2012

- Ganesh Housing Corporation Ltd. v. Dy. CIT (Guj) (High Court

Reopening BEYOND 4 Years – NO

- Denish Industries Ltd. Vs. ITO (2004) 271 ITR 340 (Guj.) (346) SLP dismissed (2005) 275 ITR 1 (St.)

- CIT Vs Aashni Leasing & Finance Ltd. 2010-TIOL-661-HC-AHM-IT

- Voltas Ltd. v. ACIT 349 ITR 656 (Bom.), CIT v. Avadh Transformers (P) Ltd. 51 Taxmann.com 369 (SC)

- PCIT Vs SKI Retail Capital Ltd. (Madras High Court); TCA No. 66 & 67 of 2018; 07/05/2020

IV. Section 147 vs. 154 vs. 263

Whether where power to rectify an order of assessment under section 154(1) is adequate to meet a mistake or error in order of assessment, Assessing Officer must take recourse to that power as opposed to wider power to reopen assessment – Held, yes Hindustan Unilever Ltd. vs. Dy. CIT (2011) 325 ITR 102 (Bom.)

Some Judicial decisions on Section 147 (Unreported):

- The words “failure to disclose material facts” isn’t a magician’s mantra & the failure to use those words will not by itself oust jurisdiction to reassess if the reasons as a whole implies a failure to disclose material facts. (Allanasons Ltd. v. DCIT CC1(1)) (Bom- HC)

- Bald statement that assessee has failed to make a full & true disclosure of material facts not sufficient. Details must be given as to which fact was not disclosed. (Bombay Stock Exchange Ltd. v. DDIT-1(2) (Bom-HC)

- After the expiry of the time limit for issue of s. 143(2) notice, the AO has no jurisdiction to make a reference to the TPO. The TPO’s report cannot form the basis for reopening the assessment. (XL India Business Services Pvt. Ltd. v. ACIT 18(1)) (ITA No.16/Del/13)

- The notice should not be in a standard format but indicate why s. 147 has been resorted to. The term “failure to disclose material facts” has a specific legal connotation. The non-disclosure has to be of a “material fact” to attract s. 147. Tata Business Support Services Ltd .v. DCIT (Bombay) (HC)

- If the recorded reasons show contradiction and inconsistency it means necessary satisfaction in terms of the statutory provision has not been recorded at all. The Court cannot be called upon to indulge in guess work or speculate as to which reason has enabled the AO to act in terms of s. 147. Plus Paper Food Pac Ltd .v. ITO (Bombay High Court)

- If the assessee does not ask for reasons and file objections before the AO, he is not entitled to challenge the reopening proceedings. Anil Kumar Chaudhary.v.ITO (ITAT Delhi)

- Reopening an assessment on the ground that there is need of an inquiry which may result in detection of an income escaping assessment is not valid. Bir Bahadur Singh Sijwali .v. ITO (ITAT Delhi)

- A writ petition is not like an appeal where the assessee has a statutory right to require the Court to entertain the challenge. A writ will be maintained only if the notice is clearly without jurisdiction & not otherwise. Nickunj Eximp Enterprises Pvt Ltd.v.ACIT (Bom.) HC

Practical Tax management Issues

- It is always advised that return in respect of notice u/s 148 should be filed timely; otherwise it may cause to reopen the assessment beyond 4 years also.

- Copy of Reasons recorded must be obtained first than only one has to proceeds with the reassessment proceedings. In case A.O. is not willing to give reasons than one has to remind it again and again than he/she is duty bound to give it. Subsequent to that reasons recorded must be read carefully so that it can decide whether it has to be objected or not.

- Reasons recorded must be carefully read and objected in case of reassessment on the basis of AIR information and bogus purchases/sales. Remember AO has to form his own belief, not borrowed one.

- It is always advisable that inspection of assessee’s file must be done by paying nominal fee of Rs.50/- before objecting reasons recorded so that one can have idea that what are the documents available in the file with A.O.

Disclaimer: The contents of this document are solely for informational purpose. It does not constitute professional advice or a formal recommendation. While due care has been taken in preparing this document, the existence of mistakes and omissions herein is not ruled out.

Do comment & Share your views on this post!

(Author can be reached at +91 9098589691, nimeshsingi@gmail.com)

(Republished with Amendments by Team Taxguru)

Author Bio

Brilliant Article, summarising ALL RELEVANT Provisions.

Author Animesh may like to add further materil to the same together with Fresh Case Law.

Kudos !!

In Response to notice u/s 148 counsel did not furnished any documents provided by the client. Ex Parte order passed by the AO u/s 144 r.w,s 147 can Assesse argue on this ground before CIT (A)

Is there any direct decisions of tribunal or high court

Excellent guide especially for non professional like me sir. Congratulations. Can I send my doubt through mail sir. Regards

really it is amazing n time saver quick access relief oriented sir thanking you sir please thanks a lot sir

MANY THANKS FOR PAINS IN WRITING SUCH ARTICLES FOR OUR BENEFIT

GOD BLESS U DEAR

Very helpful article. Thank you.

Archit Bohra

Advocate

GOOD AND INFORMATIVE ARTICLE. HIGHLY ANALYTICAL WHICH IS A RESULT OF HARD WORK AND KNOWLEDGE.

Very Useful article sir,

Just one doubt…After Scrutiny assessment if any demand comes, can corresponding income be generated in the assesses file by increasing cash amount. If not, than kindly give us the reference for the same.

Now there are paper less returns,where assessee can disclose facts

Very informative and exhaustive article. Pz. incorporate judgment of Gujrat HC in the case of Sahkari Khand Udyog Ltd prescribing the time limit for each stage of proceedings u/s 147/`148 of the Act.

Excellent and painstaking. Your kind attention is invited to the following judgements.

“issuance of notice u/s.148 is prima facie illegal for the fact that the alleged reasons recorded for reopening the assessment were communicated after the end of 6 years ie., after 31/03/2015. In this connection your kind attention is invited to the following judgments

(a) The decision of Delhi ITAT in the case of Shri Balwant Rai Wadhva vs. ITO in ITA No.4806/Del/10, which in-turn based their decision of the Delhi High Court in the case of

(b) Haryana Acrylic Manufacturing Co Vs. Commissioner of Income-tax reported in 175 Taxman 262 (Delhi)

5. It was held by them “..that issuance of the notice and the communication and furnishing of reasons would go hand in hand. The reasons are to be supplied to the assesse before the expiry of period of 6 years. If it has not been done then validity u/s 148 could not be upheld. It is not in the income tax proceeding alone. In any proceeding say, civil or criminal, if a summon is issued to the defendant / respondent, is not accompanied with the copy of plaint or complaint then it is to be construed that no valid service of notice has been effected upon the defendant or the respondents whichever may be the case. The notice could be served at any point of time before the expiry of 6 years, if AO has reasons to believe that income has escaped assessment but such reasons are also to be communicated to the assesse before the expiry of the limitation otherwise validity of such notice could not be sustainable.”

Though it is debatable, once can take shelter under it. You may consider

Excellent and painstaking. However your kind attention is invited to the following judgements. “..issuance of notice u/s.148 is prima facie illegal for the fact that the alleged reasons recorded for reopening the assessment were communicated after the end of 6 years ie., after 31/03/2015. In this connection your kind attention is invited to the following judgments

(a) The decision of Delhi ITAT in the case of Shri Balwant Rai Wadhva vs. ITO in ITA No.4806/Del/10, which in-turn based their decision of the Delhi High Court in the case of

(b) Haryana Acrylic Manufacturing Co Vs. Commissioner of Income-tax reported in 175 Taxman 262 (Delhi)

5. It was held by them “..that issuance of the notice and the communication and furnishing of reasons would go hand in hand. The reasons are to be supplied to the assesse before the expiry of period of 6 years. If it has not been done then validity u/s 148 could not be upheld. It is not in the income tax proceeding alone. In any proceeding say, civil or criminal, if a summon is issued to the defendant / respondent, is not accompanied with the copy of plaint or complaint then it is to be construed that no valid service of notice has been effected upon the defendant or the respondents whichever may be the case. The notice could be served at any point of time before the expiry of 6 years, if AO has reasons to believe that income has escaped assessment but such reasons are also to be communicated to the assesse before the expiry of the limitation otherwise validity of such notice could not be sustainable.”

Though it is debatable one can take shelter under it. You may consider it

Mr. Animesh

Very demystify article showing your hard work for the article and very usefull too.

Very good article. One query on disclosure by assesses. If some facts are disclosed in notes to accounts of Financial statements of assessee but AO do not ask any further details/explanation on the same and assessment completed without any addition the this ground subsequently AG audit point out some descripency based on the notes in financial statement. Can AO reopen the assesseemnt beyond four years on the plea of non- disclosure by assessee.

Thanks

Sunil

Mr Animesh, excellent article but initial line on A.O. is wrong. I personally think income tax persons are generally excellent as well as generous as compared to other government officers

You need correction on this point

Very well written Animesh – excellent presentation and a handy case law book. Keep up the excellent research.

HI,

Very comprehensive.There are no of practcleile tips.Iam benfittted.

Thanks

DONE WELL. CONGRATS.

Excellent article.

Very useful info.

nice one & elaborated

Excellent effort Mr.Animesh. Very nicely done and pretty useful.

Thank you.

balu

Mr.Animesh, Excellent Article and very useful.

Well done Nimesh Singi, for compilation of case laws on re-opening assessment! Further each and every case has its on theory and we cann’t applied any court rule without going through with the facts and circumstances of the case and issue in dispute. Recently most of the cases re-open on the basis of information and report of Audit team objection without going through with root and facts and material before the department.

Excellent Article !!! Animesh You have done a good hard work & can be beneficial to the readers of it.

Sub: capital gain on residential land Quiery

sir,

My client had deposited capital gain under capital gain deposit scheme through term deposit.

but no nominee was written.

now after his death, his spouse want to purchase land and want such term deposit in her name.

But bank said, term deposit cannot be tranfer without deducting tax @20% as there was NO NOMINEE entered at the time of term deposit.

Please tell me possible solutions

thanks

Gaurav Agrawal