CBDT notifies substituted new form 13 related to Application by a person for a certificate under section 197 and/or sub-section (9) of section 206C of the Income-tax Act, 1961, for no deduction of tax or deduction or collection of tax (TDS/TCS) at a lower rate, Substituted new rule 28 related to Application for grant of certificates for deduction of income-tax at any lower rates or no deduction of income-tax, Substituted Rule 37G related to Application for certificate for collection of tax at lower rates under sub-section (9) of section 206C and also amended Rule 28AB, 28AA and 37H of Income Tax Rules.

MINISTRY OF FINANCE

(Department of Revenue)

(CENTRAL BOARD OF DIRECT TAXES)

Notification No. 74/2018

New Delhi, the 25th October, 2018

G.S.R. 1068(E).—In exercise of the powers conferred by sections 197 and 206C read with section 295 of the Income-tax Act, 1961 (43 of 1961), the Central Board of Direct Taxes hereby makes the following rules further to amend the Income-tax Rules, 1962, namely:—

1. Short title and commencement,__ (1) These rules may be called the Income–tax (Eleventh Amendment) Rules, 2018.

(2) They shall come into force from the date of their publication in the Official Gazette.

2. In the Income-tax Rules, 1962,-

(I) for rule 28, the following rule shall be substituted, namely: __

“Application for grant of certificates for deduction of income-tax at any lower rates or no deduction of income-tax.

28. (1) An application by a person for grant of a certificate for the deduction of income-tax at any lower rates or no deduction of income-tax, as the case may be, under sub-section (1) of section 197 shall be made in Form No. 13 electronically, ___

(i) under digital signature; or

(ii) through electronic verification code.

(2) The Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems), as the case may be, shall lay down procedures, formats and standards for ensuring secure capture and transmission of data and uploading of documents and the Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems) shall also be responsible for evolving and implementing appropriate security, archival and retrieval policies in relation to the furnishing of Form No.13.”;

(II) in rule 28AA, __

(A) in sub-rule (2), __

(a) in clause (ii), for the words “income, as the case may be, of the last three”, the words “or estimated income, as the case may be, of last four” shall be substituted;

(b) in clause (iv), after the word “payment”, the words “, tax deducted at source and tax collected at source” shall be inserted;

(c) clause (v) and clause (vi) shall be omitted;

(B) for sub-rule (4), sub-rule (5) and sub-rule (6), the following sub-rules shall, respectively, be substituted, namely:__

“(4) The certificate for deduction of tax at any lower rates or no deduction of tax, as the case may be, shall be issued direct to the person responsible for deducting the tax under advice to the person who made an application for issue of such certificate:

Provided that where the number of persons responsible for deducting the tax is likely to exceed one hundred and the details of such persons are not available at the time of making application with the person making such application, the certificate for deduction of tax at lower rate may be issued to the person who made an application for issue of such certificate, authorising him to receive income or sum after deduction of tax at lower rate.

(5) The certificates referred to in sub-rule (4) shall be valid only with regard to the person responsible for deducting the tax and named therein and certificate referred to in proviso to the sub-rule (4) shall be valid with regard to the person who made an application for issue of such certificate.

(6) The Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems), as the case may be, shall lay down procedures, formats and standards for issuance of certificates under sub-rule (4) and proviso thereto and the Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems) shall also be responsible for evolving and implementing appropriate security, archival and retrieval policies in relation to the issuance of said certificate.”;

(III) in rule 28AB, __

(A) in sub-rule (2), __

(a) in clause (i), the word “and” shall be inserted at the end;

(b) in clause (ii), the words “and” occurring at the end shall be omitted;

(c) clause (iii) shall be omitted.

(IV) for rule 37G, the following rule shall be substituted, namely: __

“Application for certificate for collection of tax at lower rates under sub-section (9) of section 206C

37G. (1) An application by the buyer or licensee or lessee for a certificate under sub-section (9) of section 206C shall be made in Form No. 13 electronically, –

(i) under digital signature; or

(ii) through electronic verification code.

(2) The Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems), as the case may be, shall lay down procedures, formats and standards for ensuring secure capture and transmission of data and uploading of documents and the Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems) shall also be responsible for evolving and implementing appropriate security, archival and retrieval policies in relation to the furnishing of Form No.13” ;

(V) in rule 37H, __

(a) for sub-rule (1), the following sub-rules shall be substituted, namely:-

“(1) Where the Assessing Officer, on an application made by a person under sub-rule (1) of rule 37G is satisfied that existing and estimated tax liability of a person justifies the collection of tax at lower rate, the Assessing Officer shall issue a certificate in accordance with the provisions of sub-section (9) of section 206C for collection of tax at such lower rate;

(1A) The existing and estimated tax liability referred to in sub-rule (1) shall be determined by the Assessing Officer after taking into consideration the following, namely: __

(i) tax payable on estimated income of the previous year relevant to the assessment year;

(ii) tax payable on the assessed or returned or estimated income, as the case may be, of the last four previous years;

(iii) existing liability under the Act and the Wealth-tax Act, 1957 (27 of 1957);

(iv) advance tax payment, tax deducted at source and tax collected at source for the relevant assessment year relevant to the previous year till the date of making application under sub-rule (1) of rule 37G.”;

(b) after sub-rule (5), the following sub-rule shall be inserted, namely : __

“(6) The Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems), as the case may be, shall lay down procedures, formats and standards for issuance of certificate under sub-rule (5) and the Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems) shall also be responsible for evolving and implementing appropriate security, archival and retrieval policies in relation to the issuance of said certificate.”;

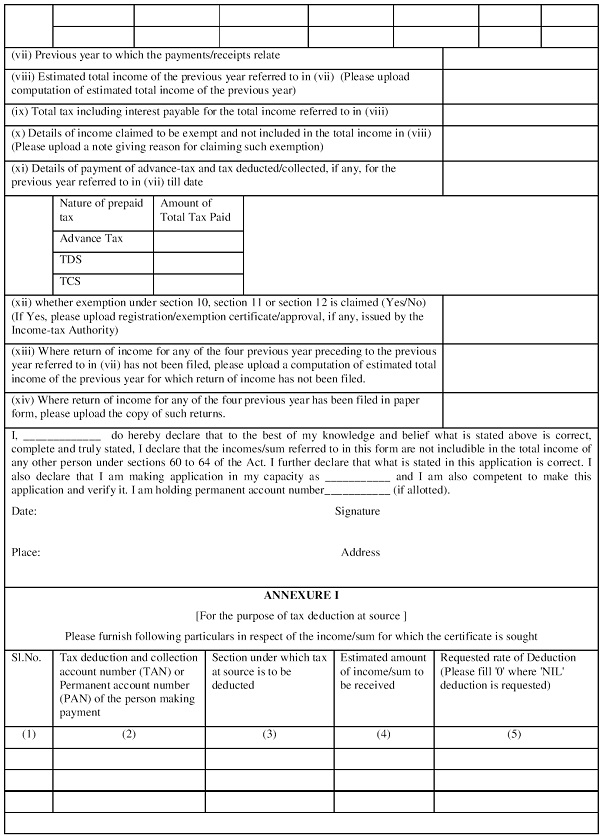

(VI) in Appendix II, for Form No.13, the following shall be substituted, namely:__

[Notification No.74/2018/F. No. 370142/10/2018-TPL]

Dr. T. S. MAPWAL, Under Secy. (Tax Policy and Legislation)

Note : The Principal Rules were published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (ii) vide notification number S.O. 969(E), dated the 26th of March, 1962 and were last amended vide notification number G.S.R. 1054(E) dated the 23rd of October, 2018.

THE COMMISSIONER HAS ISSUED LOWER DEDUCTION CERTIFICATE. IF THERE IS ANY ERROR IN THE CERTIFICATE, CAN THAT CERTIFICATE BE REVISED? IF YES WHAT IS THE PROCEDURE?

How to download electronic Soft copy of Form 13? Procedure to file Form 13 – through IT portal after logging in OR Otherwise?

how to file nil deduction of tx on sale of property by nri

Can I apply for a fresh Form 13 for dedutors missed in the previous filing

please read my article on same issue

More details

Till date not received refund apply on 26/06/2018

Kindly help me out

I appreciate your latest updates in tax matters