Government in Budget 2021 notified Leave Travel Concession (LTC) cash Voucher scheme. In view of the situation arising out of outbreak of COVID pandemic, it is proposed to provide tax exemption to cash allowance in lieu of LTC.

Initially, the scheme was announced in October 2020 for Central Government Employees and later via a press release, the scheme was extended to private sector, PSU and state government employees also.

In order to provide relief to employees, it is proposed to insert second proviso in clause 5 of section 10, so as to provide tax exemption to the amount given to an employee in lieu of LTC subject to incurring of specified expenditure. This amendment will take effect from 1st April, 2021 and will, apply in relation to the assessment year 2021-2022 only.

It is also proposed to clarify by way of an Explanation that where an individual claims and is allowed exemption under the second proviso in connection with prescribed expenditure, no exemption shall be allowed under this clause in respect of same prescribed expenditure to any other individual.”

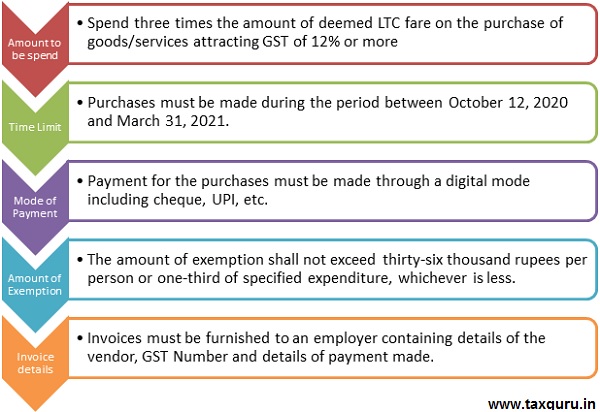

To claim the benefit under the scheme, an individual is required to fulfill the following conditions:

Note: The employee who has exercised an option to pay tax under concessional tax regime under section 115BAC of Income tax Act, 1961 shall not be entailed for the above exemption.

Author Bio

I have purchased a flat having possession date 08.01.2021. My final installment invoices of Rs 600000 generated on 08.01.2021 having GST @ 12%. Should I am eligible for LTA cash voucher scheme for this invoice . I have six person in my family including mother & father.

Is this scheme extended for FY21-22. What are the eligible dates when expenditure needs to be incurred

Hi, I purchased a car to avail the cash voucher scheme in March 21, before 31st March. As I could not furnish invoice to employer by 31st March for LTA benefit for FY 20-21. Can I claim the benefit when I file my return or claim in FY 21-22 as the LTA cycle is from 2018 to 2021.

Useful article as many of our employees are hurrying to catch up 31st march

It’s very useful to all government employees

Nice article Ajay.