Introduction: The Finance Act 2023 introduced a pivotal amendment to the Income Tax Act of 1961 by adding subsection (h) to Section 43B. This amendment, effective from April 1, 2024, emphasizes timely payments to Micro and Small Enterprises (MSMEs). The section outlines specific criteria for allowable expenses and disallowances, impacting the taxable income computation of enterprises.

As per the amendment;

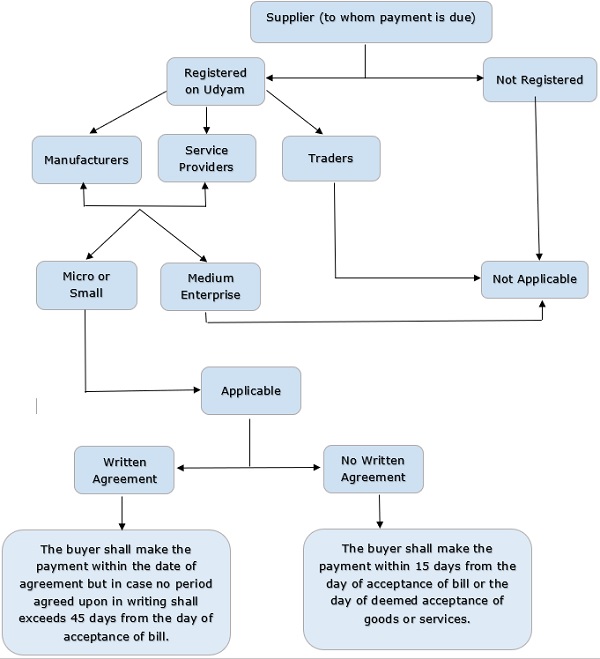

a. If any amount remained outstanding to MSME supplier as on 31st March which is not paid within 45 days or period agreed between the buyer and supplier in writing, whichever is earlier shall be disallowed;

b. If any amount remained outstanding as on 31st March not paid within 15 days when there is no agreement between buyer and supplier in writing shall be disallowed.

To summarize if any sum payable to micro & small enterprises (supplier) is not paid within time limit as mentioned above; then the expenses is not allowed as deductions while computing the taxable income of an enterprise. Those expenses will be allowed only after the payment is made to the supplier.

Some Important Notes:

- This amendment takes effect from 1st April, 2024 and will accordingly apply in relation to the assessment year 2024-25 (i.e FY 2023-24) and subsequent assessment years.

- To identify the enterprise and to ensure the due compliances it is advisable for business entities to take an Annual Declaration from their supplier indicating that they are micro or small enterprises registered under the Micro, Small and Medium Enterprises Development Act, 2006.

- This section applies to Micro and Small Enterprise only and amount payable to medium enterprises will not be governed by section 43B(h).

- This section is not applicable to those enterprises who show their income under presumptive basis (i. e 44AD/44ADA/44AE).

- This section is not applicable for dues outstanding in respect of capital expenditure incurred.

- Though payment is made after 15/45 days but before filing a return of income, the deduction can only be claimed in the year in which actual payment is made and not in the year of accrual.

- In case there is a dispute between buyer and supplier, in that case as per MSMED Act the day on which such objection is removed by the supplier shall be treated as day of acceptance and the payment has to be made before the appointed day which will be day following immediately after the expiry of the period of fifteen days from the day of acceptance.

Situations:

|

Sr. No |

Situation | Allowed / Disallowed |

| 1 | Amount outstanding and paid after 15/45 days but before 31st March 2024 | Allowed |

| 2 | Amount not paid within 15/45 days and is outstanding as on 31st March 2024 | Disallowed |

| 3 | Amount outstanding on 31st March 2024 but 15/45 days’ period not ended on 31st March 2024 and payment is made in Next FY within prescribed time | Allowed |

| 4 | Amount outstanding on 31st March 2024 but 15/45 days’ period not ended on 31st March 2024 and payment is not made in Next FY within prescribed time | Disallowed |

Note: Please refer below flow chart for more clarity about the section 43B(h)

Applicability of Section 43B Clause (h)

Conclusion: Section 43B(h) brings a nuanced dimension to the Income Tax Act, emphasizing timely payments to MSMEs and influencing deductible expenses. Understanding its intricacies, exceptions, and impact on various scenarios is crucial for businesses aiming for tax efficiency. As enterprises navigate these amendments, compliance and strategic financial planning become imperative to ensure smooth operations and avoid disallowances in taxable income calculations.

Author Bio

Capital Creditors if falls under Micro and Small category will also be excluded.

However the industry challenge is that if buyer holds the GST amount of MSME vendors being default, then still this section will be applicable.

very descriptive and useful explanation for MSME in a simple language.