The Startup Registration Program (SRP) is an initiative of the Department for Promotion of Industry and Internal Trade (DPIIT) under the Startup India initiative. The SRP aims to provide a platform for startups to register themselves with the government and avail of the benefits offered under the Startup India scheme.

India’s startup ecosystem has seen remarkable growth since the launch of the Startup India Initiative in January 2016. By December 2024, over 1,57,000+ startups had been officially recognized by DPIIT under the initiative. This milestone highlights the country’s dynamic entrepreneurial landscape.

*Foreign company/business are not allowed to claim the benefit u/s 80IAC

B.) Startup Recognition Benefits :

1. Tax Exemption – Eligible startups get a 3-year tax holiday under Section 80IAC.

2. Access to Funding – Startups can avail government schemes like the Startup India Seed Fund Scheme.

3. IP Protection – Benefits include fast-track patent examination and an 80% patent filing fee rebate.

4. Self-Certification – Simplified compliance for 6 labor and 3 environmental laws.

5. Section 56 Benefits – Startups are exempt from tax on shares issued above fair market value, provided the post-issue paid-up capital and share premium do not exceed ₹25 crores, and a declaration is filed with DPIIT in Form 2.

6. Easier Public Procurement – Exemption from Earnest Money Deposit (EMD) and bid security in government tenders.

7. Merchant Banker Valuation Report : A DPIIT recognized startup is not required to obtain a valuation report from a merchant banker for the purpose of Section 56(2)(viib) exemption.

C.) What is the 80IAC deduction, and is separate registration required for it if the startup is already recognized?

Yes, even if a startup is recognized by the government, it still needs to register for 80IAC (Separate Application) to avail the tax benefits provided under the scheme.

What is 80IAC?

80IAC is a tax exemption scheme for startups that was introduced in the Union Budget 2016. Under this scheme, eligible startups can get a tax holiday for three consecutive years out of their first ten years of operation.

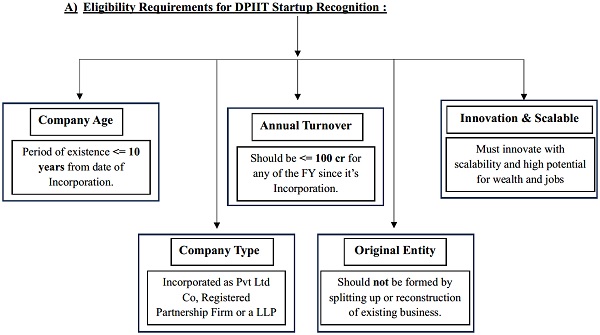

Eligibility Conditions for 80IAC Registration :

1. The startup should be incorporated as a private limited company or a limited liability partnership (LLP).

2. The startup should have been incorporated after 1st April, 2016.

3. The total turnover of the startup should not exceed INR 100 crores during the eligible assessment year(s).

D.) Benefits available to entities registered under 80IAC that are not provided to startups recognized by DPIIT but not registered under 80IAC.

1. Tax Holiday : 100% tax exemption on profits derived from “eligible business” for consecutive 3 years within the first 10 years from the date of incorporation under Section 80IAC.

*Exclusions from eligible business : Dividend, Interest, Rental Income, Capital gains and other non-operating income.

2. Loss Carry Forward : Carry forward losses even if there is a change in shareholding of more than 51%, provided that all the shareholders of the company on the last day of the year in which the loss was incurred continue to hold those shares on the last day of the previous year in which the loss is set off.

3. Deferred Tax Payment on Exercise of ESOPs: Unlike regular companies, 80IAC registered startups are not required to deduct tax at source (TDS) on the fair value of the shares granted to employees under an ESOP when the employee exercises their option to purchase the shares. This deferment of tax payment provides significant cash flow benefits to both the startup and its employees.

E.) What is the process in order to claim Tax exemption from Income tax perspective?

1. File form 10CCB certified by Chartered Accountant before one month of due date of filing of ITR. This is over and above as may be required under 44AB. (Form 10CCB is a Chartered Accountant’s certificate certifying a startup’s eligibility for deduction under Section 80-IAC. It includes details of income from the eligible business and compliance with prescribed conditions.)

2. Company is required to claim deduction u/s 80IAC while filing the return under Chapter VI-A in the ITR for the relevant 3 consecutive FYs.

3. Deduction is available only if the startup has profits and cannot be carry forward if not

claimed in any year.

4. Timely filing of the Tax Audit Forms (if applicable), 10CCB & ITR is must in order to claim benefit under 80IAC.

F) **Applicability of MAT/AMT Provisions Despite Section 80-IAC Exemption.

Companies claiming deduction under Section 80-IAC are still liable to pay MAT/AMT under Sections 115JB/115JC. This is due to the overriding clause “Notwithstanding anything contained in this Act” in both sections. Since Section 80-IAC isn’t listed as an exception (unlike 80P), the exemption doesn’t override MAT/AMT applicability. Does this mean there’s no real benefit under Section 80-IAC?

Not at all!!! Even though MAT/AMT may apply, the company still enjoys a significantly lower effective tax rate compared to the standard rates — 26% for companies and 30% for partnership firms or LLPs.

Additionally, any MAT/AMT paid during the 3-year tax holiday period under Section 80-IAC is available as credit and can be carried forward to offset tax liabilities in future years. This ensures that the benefit of the deduction is not entirely lost, but rather deferred.

G) **Opting for Section 115BAA – Concessional Tax Rate and Eligibility for Section 80-IAC Deduction.

1. A newly incorporated startup that qualifies for Section 80-IAC should not opt for Section 115BAA right away, because doing so would make it ineligible for the 80-IAC deduction.

2. Instead, the startup should first avail the 3-year tax holiday under Section 80-IAC.

3. After fully utilizing the 80-IAC benefit, the startup can then switch to the concessional tax regime under Section 115BAA, which offers a lower corporate tax rate (22% plus surcharge and cess), for the remaining years.

Author Bio

Please clarify on filing form 10CCB to claim deduction under section 80IAC.

Hi Kuldip, I focused on 80IAC and DPIIT registration in this article to keep it concise. I plan to cover 10CCB and how to claim the deduction in a separate article. In the meantime, I’m happy to explain the 10CCB process via email if you share your email address.

Insightful article