The CBDT on 12th September 2019, notified the much talked about e-assessment procedure vide Notification no. 61/2019. The stakes were high, as it was expected to reduce the red-tapism in the country, during an assessment proceeding. This notification was quickly followed up by another notification vide 62/2019, giving effect to the Income Tax E-Assessment Scheme, 2019.

This article attempts to cover both these notifications and provides the reader with a bird’s eye view of the E-assessment scheme.

Important Definitions

- “assessment” means assessment of total income or loss of the assessee under sub-section (3) of section 143 of the Act

- automated allocation system” means an algorithm for randomised allocation of cases, by using suitable technological tools, including artificial intelligence and machine learning, with a view to optimise the use of resources

- automated examination tool” means an algorithm for standardised examination of draft orders, by using suitable technological tools, including artificial intelligence and machine learning, with a view to reduce the scope of discretion.

- e-assessment” means the assessment proceedings conducted electronically in ‘e-Proceeding’ facility through assessee’s registered account in designated portal

- registered mobile number” of the assessee means the mobile number of the assessee, or his authorised representative, appearing in the user profile of the electronic filing account registered by the assessee in designated portal

- “video telephony” means the technological solutions for the reception and transmission of audio-video signals by users at different locations, for communication between people in real-time.

- Mobile app” shall mean the application software of the Income-tax Department developed for mobile devices which is downloaded and installed on the registered mobile number of the assessee

The Process of Assessment

Similar to how there is Centralized Processing Centers at Ghaziabhad and Bengaluru, National E-assessment center, Regional E-assessment Centres, assessment units, verification units, technical units and review units shall be set up to facilitate the conduct of e-assessment. All these centers have been assigned their role-play in the Notification.

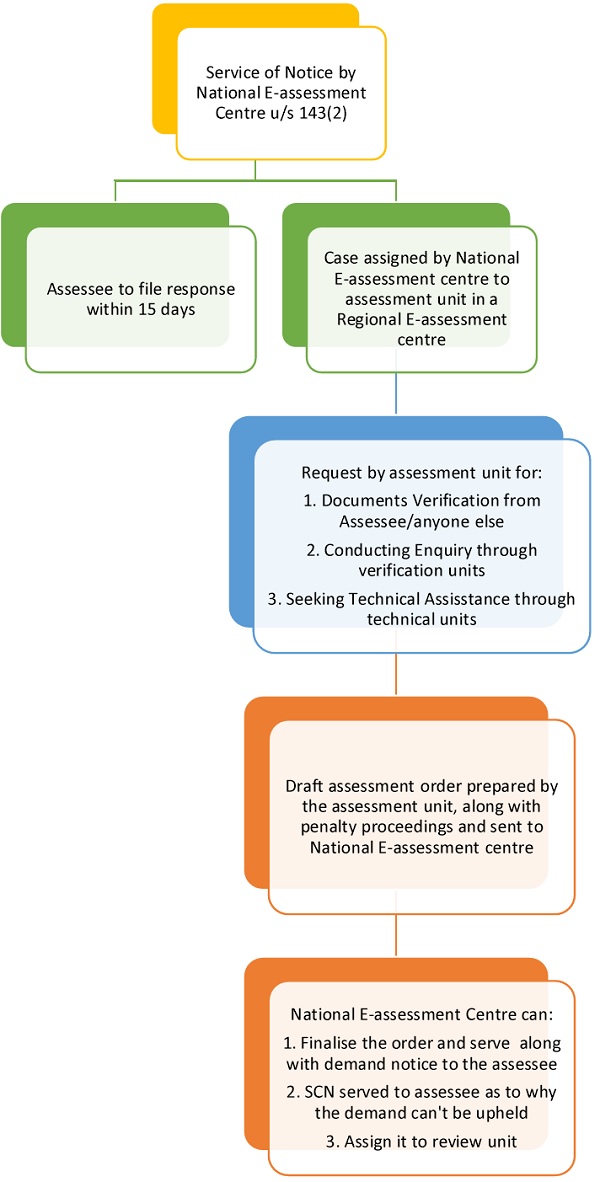

Process Flow Diagram (A):

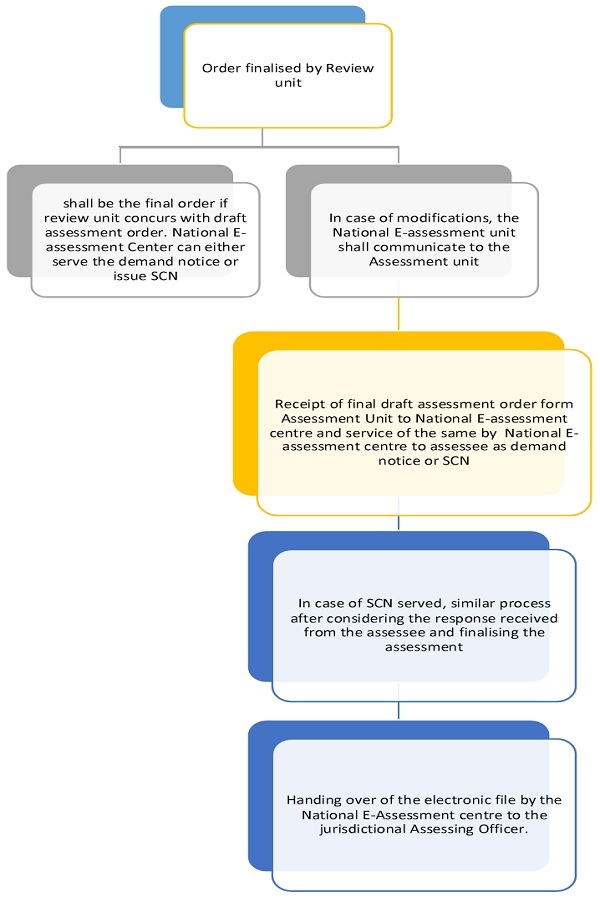

Process Flow Diagram (B):

Other Aspects of E-Assessment

- Penalty proceedings can be initiated by the assessment unit through National E-assessment center in case of non-compliance of any notice, direction or order.

- All the above communication shall take place through electronic communication which will be served either in the electronic portal or e-mail id or mobile app and a real time alert.

- There is no personal appearance in the process, but an assessee can request for personal hearing of the same. Personal hearing shall take place through Video conference, through a software which would enable Video telephony. Further, video conference facilities shall be established at such locations for the assessee to visit and attend the video conference, even though he may not have video conference facilities at his place.

- E-assessment is not a special type of assessment. All the current assessments can be carried out in an electronic manner following the procedure mentioned above. Interestingly, re-assessment u/s 147 has not been covered and that has to happen through offline mode.

- Appeals u/s 246A shall remain lie with the jurisdictional Commissioner (Appeals).

Powers of Jurisdictional Assessing Officer:

Once the file has been handed over to the Assessing officer, he would have powers only for the following:

- imposition of penalty;

- collection and recovery of demand;

- rectification of mistake;

- giving effect to appellate orders;

- submission of remand report, or any other report to be furnished, or any representation to be made, or any record to be produced before the Commissioner (Appeals), Appellate Tribunal or Courts, as the case may be; proposal seeking sanction for launch of prosecution and filing of complaint before the Court;

- However, the National e-assessment Centre may at any stage of the assessment, if considered necessary, transfer the case to the Assessing Officer having jurisdiction over such case

Understanding the fine print

The complete assessment till the finalization of 143(3) shall be on an electronic mode without any face to face interaction. This is expected to reduce the large scale redtapism and the nexus between the AO and the assessee.

The new process has resulted into geographical dissection of the assessment proceeding, thus curbing the chance of even a nexus between the assessment unit and the jurisdictional assessment officer.(At least that is what is expected!).

The idea of video conference is exciting as this would be the first ever application in India and if this succeeds, one can even expect the same in GST as well.

The scheme has proposed the time limit (15 days) within which an assessee has to respond to a notice u/s 143(2). It is surprising that the time limit which was not present in 143(2) has been imposed by way of notification issued through 143(3A).

Though the scheme clarifies where the appeal would lie, the problem would be faced by the Department. As the e-assessment shall take place with someone else and the file would reach the jurisdictional AO only after completion of assessment, the jurisdictional AO and Commissioner would have to be on their toes to read the file and be prepared for the appeal.

Generally, an assessment would involve a submissions comprising 300+ printed pages. Huge work load would be expected as the same would have to be converted into digital format. Technical glitches from the Information Technology side can also be expected and investments in servers would be required to keep huge amount of data.

One has to ensure that following precautions are taken:

- Ensure that fields used in the return are consistent as it is totally automated. Clerical errors without having a bearing on the tax payable may initiate assessment proceeding.

- Ensure that mobile number and the e-mail id are updated as the assessee would be notified through an SMS/e-mail.

However, the above move of the Government is one of the first steps in right direction in easing assessment procedures and cleansing the bureaucracy.

| Title | Notification No. | Date |

|---|---|---|

| Directions for giving effect to Income Tax E-assessment Scheme, 2019 | Notification No. 62/2019- Income Tax | 12/09/2019 |

| CBDT notifies Income Tax E-assessment Scheme, 2019 | Notification No. 61/2019- Income Tax | 12/09/2019 |