Satish Vattam, CA & Alok Agarwal, FCA

Who is distinct person?

As per CGST ACT

Section 22(1) provides that every supplier shall be liable to be registered under this Act in the State or Union territory from where he makes a taxable supply of goods or services or both, if his aggregate turnover in a financial year exceeds Rs. 20 lakhs (10 lakhs for specified states):

|

That means if the aggregate turnover of a person/an entity crosses the threshold prescribed (20 Lakhs/10 Lakhs), then he has to get registered in each of the states from where he is making taxable supply of goods/ services. He is required to obtain registration for branch offices irrespective of the turnover of such branch office. |

Section 25(4) provides that, a person who has obtained or is required to obtain more than one registration, whether in one State or Union territory or more than one State or Union territory shall, in respect of each such registration, be treated as distinct persons for the purposes of this Act.

As Per Section 8 of IGST ACT

Explanation 1 – For the purposes of this Act, where a person has,–

(i) an establishment in India and any other establishment outside India;

(ii) an establishment in a State or Union territory and any other establishment outside that State or Union territory; or

(iii) an establishment in a State or Union territory and any other establishment being a business vertical registered within that State or Union territory, then such establishments shall be treated as establishments of distinct persons.

| That means branches/offices/establishments/ Verticals of a single entity (bearing same PAN number) in same/ different states having separate registration for purpose of GST laws shall be considered distinct entities. |

Who is Related Person?

Explanation to Section 15 of CGST Act provides,-

(a) persons shall be deemed to be “related persons” if –

(i) such persons are officers or directors of one another’s businesses;

| That means owner of a business should be officer or director of another business, with which he is transacting.

Say Mr. A is a major shareholder (owner) of A Ltd and Mr. B is a major shareholder (owner) of B Ltd. If Mr. A is appointed as an Officer/director in B Ltd, and Mr. B is appointed as officer/director in A Ltd , then A Ltd & B Ltd are related entities Thus, the test should establish that 2 companies are connected if they had common officers/directors. |

(ii) such persons are legally recognised partners in business;

| Mr. A and Mr. B are partners in a partnership firm Zika & Co. As per this clause, A&B shall be related persons. A transaction of supply between A & B in the course or furtherance of business shall be treated as supply even if made without consideration |

(iii) such persons are employer and employee;

| Employer and Employees are considered to be related persons, making all perquisites taxable under GST. However exemption for gifts up to an annual value up to Rs. 50,000/- is given. |

(iv) any person directly or indirectly owns, controls or holds twenty-five per cent or more of the outstanding voting stock or shares of both of them;

| If Mr X holds sharing having voting rights of 25% or more of Company A and Company B, then both Company A and Company B shall be deemed to be related. |

(v) one of them directly or indirectly controls the other;

| This shall include all the holding – subsidiary relationships, including subsidiary of a subsidiary companies.

The term used in this clause is control. In addition to shareholding, control is said to exist if one person can exercise operational / legal restraint over the other. For example: A Ltd plays significant role in corporate policy, design specification, quality control, marketing of B Ltd. It can be said that A Ltd controls B Ltd. |

(vi) both of them are directly or indirectly controlled by a third person;

| As per clause (iv) of the definition, relationship is being established based on shareholding. However, in this clause relationship is established on the basis of control. Let’s say X Ltd controls the composition of Board of directors of A Ltd and B Ltd. He is said to control both A Ltd and B Ltd. In such cases, A Ltd and B Ltd are related persons. |

(vii) together they directly or indirectly control a third person; or

| If A Ltd and B Ltd together control X Ltd, then A Ltd and B Ltd are treated as related person |

(viii) they are members of the same family;

| 2(49) “family” means,––

(i) the spouse and children of the person, and (ii) the parents, grand-parents, brothers and sisters of the person if they are wholly or mainly dependent on the said person; |

(b) the term “person” also includes legal persons;

(c) Persons who are associated in the business of one another in that one is the sole agent or sole distributor or sole concessionaire, howsoever described, of the other, shall be deemed to be related.

Why understanding the distinct persons and related person is important?

1. Schedule I of the GST Act, Clause II provides that :

“Supply of goods or services or both between related persons or between distinct persons as specified in section 25, when made in the course or furtherance of business SHALL BE TREATED AS SUPPLY EVEN IF MADE WITHOUT CONSIDERATION:”

2. Section 15 provides that the value of a supply of goods or services or both shall be the transaction value, which is the price actually paid or payable for the said supply of goods or services or both where the supplier and the recipient of the supply are not relatedand the price is the sole consideration for the supply.

That means for a supply of goods or services or both between related persons or between distinct persons, the transaction value has to be ignored and valuation as per Rule 2 of Valuation Rules has to be considered.

Rule 2 of Valuation Rules

Option 1: Open Market Value of such supply

Option 2: If Open market value is not available, be the value of supply of goods or services of like kind and quality

Option 3: If Option 1 and 2 is not applicable, then be the value as determined by application of rule 4 or rule 5

|

Rule 4 – 110% of cost of production / cost of provision of service Rule 5 – reasonable means consistent with the principles and general provisions of section 15 |

II. If goods are intended for further supply as such

In addition to the options as described in I above, at the option of the supplier, value can be an amount equivalent to 90% of the price charged for the supply of goods of like kind and quality by the recipient to his customer not being a related person.

III. Where the recipient is eligible for full input tax credit.

Value declared in the invoice shall be deemed to be the open market value of goods or services.

What to be done in case business entities have related party transactions under GST?

There is an additional burden on the business entities to identify all the transactions between related persons and distinct establishments. The moot question which arises in the case of supply to related persons is valuation.

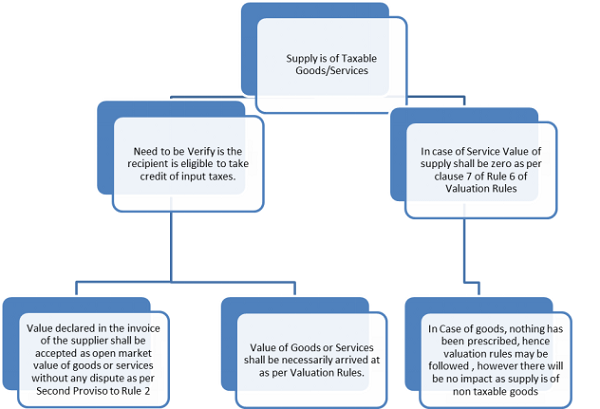

Valuation to be followed in different scenarios has been explained in the below flow chart.

Steps wise process of same can be described as below:

Step 1: Identify whether supply to the related/distinct entity is of taxable goods/ services.

Step 2: If answer in step 1 is No then valuation of supply of services shall be Nil as per clause 7 of Rule 6 of Valuation rules. For supply of non-taxable goods to related/distinct entities nothing has been specifically provided, however valuation rules may be adopted. Any Valuation shall be of no impact as tax applicable is zero.

Step 2: If answer in step 1 is yes, then the supplier need to examine if the recipient is eligible to take credit of Input taxes.

Step 3: if answer to step 2 is yes, then Value declared in the invoice of the supplier shall be accepted as open market value of goods or services without any dispute as per second provision of Rule 2. This provision appears to accommodate internal preferences of the parties where the tax paid is revenue neutral. However, caution is advised in taking recourse of this proviso and charging a price lower than cost.

Step 4: If answer to Step 2 is No, then Value of goods/ services supplied necessarily need to be arrived at using valuation rules.

Lot of precaution needs to be taken when the transaction is of taxable supply of goods/services between related /distinct persons and the recipient is not eligible for input tax credit. For those transactions the value of goods or services has to be determined based on open market value and invoice has to be raised along with due taxes and should be accounted and reported as a transaction with any other third party.

For most of the supplies between related/distinct persons, open market value may not be available as goods/services supplied to related entity may or may not be supplied to unrelated persons.

Example: The management services provided by the HO to all the branches.

Illustrative list of transactions between distinct entities / related persons (without consideration)

| Nature of transaction | Action |

| 1. Sharing of infrastructure

Eg: Office space owned by X Ltd (Holding company) is but allowed to be used by A Ltd (Subsidiary) or other entities under the same management without consideration |

X Ltd mandatorily needs to value the supply and raise invoice with GST to all entities with whom the infrastructure is being shared. |

| 2. Management cost incurred at head office to manage the operations of branches | H.O needs to value such supply and raise an invoice with GST to all the branches for whom the cost is being incurred |

| 3. Licence fees paid by head office for entire company | The company must request the vendor / supplier to invoice the licence fees for each establishment separately. In case the vendor disagrees, H.O company must raise invoice to the other branches |

| 4. H.O incurs expenditure to set up a branch office | H.O has to raise an invoice and charge GST on the value of such supply |

| 5. Processing fees paid for loan availed by the H.O | H.O needs to allocate the fund raising expenses to all the branches and raise the invoice with GST |

To conclude, it becomes imperative for the business to identify all the transactions undertaken between the related parties and then appropriately arrive at valuation for ascertaining the tax impact.

Hope this article is of help in your professional work. In case of any query/feedback please write us at alok@alokfoundation.com, Satish.vattam@gmail.com

The tenant Consumer Society( GST Reg ) allowing Credit society(Not GST Regt ) under the same Mgt to use & share premises .

Does consumer society need to value the Supply & raise invoice with GST ? If Credit Society is not paying rent to Consumer Society

Thanks…..

The tenant ,Consumer co operative society allowing credit society under same Mgt to use the premises, The Consumer society is GST Regt whereas credit society not Regt under GST

.

Does consumer society need to value the supply & raise invoice with GST ?

Consumer Society’s contention is that we don’t charge any rent from Credit Society as we belong to same Mgt

Thanks a lot….

Hi,

Whether society and member will be treated as related party?

So if member is using any property/land of society for personal purpose at discounted rate or at free of cost will it attracts GST on society under this provision? Or if any lease agreement is signed between society and it’s member for personal use of some land of society at lesser than market value of land will gst is applicable to society on discount given to member?

If a supply made to a distinct person with consideration even then same shall be treated as deemed supply or a normal supply

Sir, Mr A is working in Z company and some times he goes on duty to some where related to Y company then we have booked his expenses in Z as below

Mr A a/c – Cr

Y (related company) A/c Dr

then we have passed same entry in Y as below

Expenses A/c – Dr

Z company A/c -Cr

here IUT Y & Z company is Matched but is there any TAX issue in this..?

Thank you Sir!!! It has helped me a lot in taking critical decision.

GSTIN of related person would be different. In cases where at a consolidated level of group, the balance sheet of both related persons are getting merged. There would be mismatch in balance sheet and gst return. Can authorities question that?

Travelling and conveyance expenses paid to employee are taxable under reverse charge or not.

Will centralized accounting services and utility bills with respect to same be liable as Interco transactions?

Well narrated in a lucid manner, thank you.

Will a non executive director, who is not getting any monetary benefit from the company, be covered under the aforesaid provisions? Will invoice with GST be raised in such case? Please clarify.

Excellent analysis!!