Dear readers, in the past few months, GST Department is issuing GST ASMT-10 Notices and show cause notices in Form GST DRC-01 to GST registered dealers for discrepancies found in there filed GSTR-1, GSTR-3B and excess/ wrong availment of GST Input tax credit. In today’s article we will discuss about a real case study of GTA Service provider who has received GST ASMT-10 and Form GST DRC-01 show cause notice from department due to mismatch in GSTR-1 and GSTR-3B.

Further, we will discuss a draft reply related to this notice. In GST Notice reply, each and every reply depends on the facts of the case and no one format can be used in all cases and drafting of same notice reply may vary from professional to professional depending on his grip and experience of the subject. Reply which we are going to discuss in this blog is purely for educational purpose and some experts may have different opinion on same notices. So, positive comments are always welcome for the well being of more peoples.

Facts of the case – Mr. A is Proprietor of ABC Road lines and providing GTA services through road transport. During the F.Y -2018-19, Mr. A has provided GTA services to XYZ Private Limited and filed his GSTR-1 on time showing this service as GTA Services attracting reverse charge where liability to be paid by XYZ Private Limited. At the filing of GSTR-3B, ABC Road lines due to clerical mistake/ ignorance of law filed Nil GSTR-3B because GST Liability is to be paid by XYZ Private Limited on reverse charge basis. In this case, Proper Officer as issued ASMT-10 notice to the ABC Road Lines asking the reason of this mistake and later they issued show cause notice under Form GST DRC-01 to pay GST Liability on whole turnover of GTA Service provided to XYZ Private Limited.

In reply to this notice, there are many ways of presentation of case to the proper officer. Below is sample draft reply after taking care of above mentioned facts of the case.

To

The GST Officer

Delhi

Sub: Reply of Form GST DRC-01

Ref: ABC ROAD LINES

GSTIN No – XXXXXXX

Dear Sir

With reference to the above cited subject, please note that, we are running a Good & Transport Agency, providing services related to transport of goods by Road and Mr. A is the Proprietor of this firm. These details can be verified from our profile. For your convenience we are attaching snapshot of that.

As per notification No – 13/2017- Central Tax (Rate) Dated – 28th June 2017, GTA Services are covered under reverse charge mechanism, as specified in S.No-1 of this notification. According to this notification, we are covered under this notification. For your ease we are attaching snapshot of that notification.

Notification No. 13/2017- Central Tax (Rate)

New Delhi, the 28th June, 2017

GSR 692(E).- In exercise of the powers conferred by sub-section (3) of section 9 of the Central Goods and Services Tax Act, 2017 (12 of 2017), the Central Government on the recommendations of the Council hereby notifies that on categories of supply of services mentioned in column (2) of the Table below, supplied by a person as specified in column (3) of the said Table, the whole of central tax leviable under section 9 of the said Central Goods and Services Tax Act, shall be paid on reverse charge basis by the recipient of the such services as specified in column (4) of the said Table:-

Table

|

Sl. No. |

Category of Supply of Services | Supplier of service | Recipient of Service |

| (1) | (2) | (3) | (4) |

| 1 | Supply of Services by a goods transport agency (GTA) in respect of transportation of goods by road to-

(a) any factory registered under or governed by the Factories Act, 1948(63 of 1948);or (b) any society registered under the Societies Registration Act, 1860 (21 of 1860) or under any other law for the time being in force in any part of India; or (c) any co-operative society established by or under any law; or (d) any person registered under the Central Goods and Services Tax Act or the Integrated Goods and Services Tax Act or the State Goods and Services Tax Act or the Union Territory Goods and (e) any body corporate established, by or under any law; or (f) any partnership firm whether registered or not under any law including association of persons; or (g) any casual taxable person. |

Goods Transport Agency (GTA) | (a) Any factory registered under or governed by the Factories Act, 1948(63 of 1948); or

(b) any society registered under the Societies Registration Act, 1860 (21 of 1860) or under any other law for the time being in force in any part of India; or (c) any co-operative society established by or under any law; or (d) any person registered under the Central Goods and Services Tax Act or the Integrated Goods and Services Tax Act or the State Goods and Services Tax Act or the Union Territory Goods and Services Tax Act; or (e) any body corporate established, by or under any law; or (f) any partnership firm whether registered or not under any law including association of persons; or (g) any casual taxable person; located in the taxable territory. |

As pointed out in point (b) of your show cause notice, you have mentioned that on the taxable supply of Rs.1412650/- there is short payment of Tax liability of Rs.84760/- which is not correct and turnover as mentioned by you is also not correct.

You have taken this tax liability figure from GST-1 for the Quarter October-December, 2018, in which we have supplied GTA Services to M/s XYZ Private Limited having GSTIN – *********

If we see these transaction in details, it can be clearly seen that, while Filing GSTR-1of this period we have reported these GTA services under B2B Column and highlighting that tax is payable on reverse charges because service recipient in this case is Private limited company which are liable to pay GST in this transaction under reverse charge mechanism as per above mentioned GST Notification.

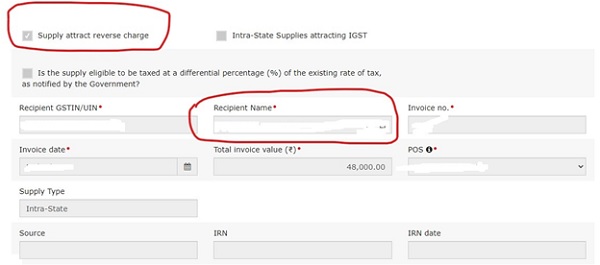

For your reference, we are attaching a sample invoice issued by us to our customers to whom we provide GTA Services.

From above discussion, we hope, matter is clear before your goodself that, we are not liable to pay GST in this case and services receiver is liable to pay taxes in this case. Further, due to clerical mistake at the time of filing GSTR-3B of this period, by mistake NIL GSTR-3B has been filed but this clerical mistake does not affect the revenue of Government because, GST liability has to be discharged by GTA Service receiver and we have correctly filed our GSTR-1 showing this service has attracting reverse charge. Requesting your goodself to kindly condone the clerical error committed while filing GSTR-3B because this error does not have any impact on revenue of the department.

If still you require any other information then kindly let us know.

Thanks

Yours Truly

For ABC ROAD LINES

Authorised Person

Author’s Note: Above is the glimpse of Sample GST Notice reply, which vary from case to case basis and professional to professional. While drafting reply, we should firstly understand the case properly and then present the case in sequence. Proper attention should be given to provisions applicable at that time because wrong presentation of case may invite heavy tax liability, interest and penalty.

****

Disclaimer: This article is for the purpose of information and shall not be treated as solicitation in any manner and for any other purpose whatsoever. It shall not be used as legal opinion and not to be used for rendering any professional advice. The author will not be held responsible for any lose, if occur after using above information. Kindly consult your professionals before taking any action. This article is written on the basis of author’s personal experience and provision applicable as on date of writing of this article. Adequate attention has been given to avoid any clerical/arithmetical error, however; if it still persists kindly intimate us to avoid such error for the benefits of others readers. The Author “CA. Shiv Kumar Sharma” can be reached at mail –shivsharma786@gmail.com and Mobile/WhatsApp–9911303737.

Author Bio