Page Contents

- 1. Basic Principles Behind Return Simplification Exercise

- 2. Current Status

- 3. Model-A (Recommended by Committee on Return Filing)

- 4. Model-B

- 5. Core concepts that have found wide-spread acceptance among all stakeholders.

- 6. Where the Two Models don’t match

- 7. Principle for reconciling the differences

- 8. Applying 3 Principles on Provisional Credit

- 9. Applying 3 Principles on Linkage to Tax Payment

- 10. Alternate Solution

- 11. Preventive Safeguards

- 12. Corrective Safeguards – Semi-automatic Reversal, if preventive safeguard is not sufficient

- 13. Conclusion

- 14. Limitation pointed out for Model-B

- 15. Other Recommendations

1. Basic Principles Behind Return Simplification Exercise

♦ Reduction in number of Returns to One Return per month

♦ No to-and-fro movement of invoice data (like GSTR → GSTR → GSTR → GSTR1A → GSTR-3)

♦ Simplicity of Return design: Summary of outwards supplies and inward supplies with annexure of invoices for outward supplies and inward supplies attracting reverse charge. Taxpayer Interface should be simple to use and fill up.

♦ Continuous upload and viewing of invoices: Supplier should be able to upload invoices at anytime basis and Recipient should be able to continuously see the invoice uploaded by the supplier.

♦ Safeguard the tax revenue: Input Tax Credit mechanism should ensure have mechanism to protect government revenue

♦ Follow business practice: As far as possible follow business practice rather than disrupting the established practices. (Ex. upload of invoice data by bunching line items at tax rate level led to increase of work for sellers and buyers both)

2. Current Status

♦ Return Committee constituted by GST Council submitted its report suggesting one model (Model-A).

♦ Mr Nandan Nilekani, former Chairman of UIDAI suggested another model (Model-B)

♦ Both Models have many commonalities but few differences.

♦ Both reports were presented before GST Council. The Council asked the Group of Ministers under chairmanship of Sh Sushil Kumar Modi to consider both and come up with one model

♦ This meeting is towards this goal in terms of wide stakeholders’ consultation.

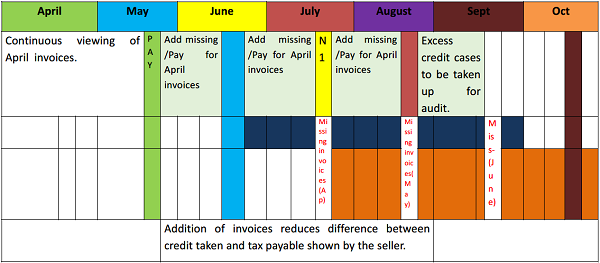

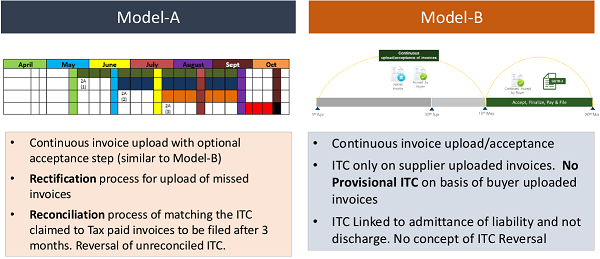

3. Model-A (Recommended by Committee on Return Filing)

♦ Monthly return

♦ Return design: Monthly return shall consist of summary return like present GSTR 3B and as its annexure invoices for outward supplies and inward supplies attracting reverse charge.

♦ No system based matching: Matching would be done offline by the taxpayer.

♦ Continuous viewing of invoices: Recipient would be able to continuously see the invoice uploaded by the supplier and its tax payment status. (Locking facility can be considered to be made available as an IT facilitation measure.)

♦ Continuous facility to add invoice: Seller would have continuous facility to add invoices for the past period and pay tax thereon.

♦ Partial payment of tax: Partial payment of tax on self assessment basis shall be allowed. Buyer would be shown the tax payment status of the purchase invoices in the conventional design.

♦ Input tax credit: Input tax credit shall be provisionally taken on the basis of receipt of goods and covering invoices giving declaration on aggregated basis.

♦ Return filing shall be spread out: Above Rs 1.5 Cr by 10th and Lower by 20th of the next month, except composition dealer etc.

♦ Return and reconciliation of credit – Return is one stage but based on credit taken vis a vis supply declared by seller.

(i) Main return: This would be a summary return with outward supply invoices and reverse charged inward supply invoices as annexure. Input tax credit would be availed on self declaration basis.

(ii) Rectification platform: This IT platform would provide facility to continuously add missing invoices, credit note and debit note for the past period and pay tax liability thereon for a period say rectification period.

(iii) Action on excess credit: On expiry of the rectification period, cases where excess credit is taken shall be taken up for assessment/scrutiny (Missing invoices to be reported towards the end of rectification period).

Note: Tax administration shall take action to recover tax from the seller on the basis of the missing invoices reported and where recovery takes place, credit would be considered valid.

4. Model-B

♦ Monthly return

♦ Continuous facility to add invoice: Seller would have facility to add invoices continuously for the present as well as past period and pay tax thereon.

♦ Continuous viewing of invoices: Recipient would be able to continuously see the invoice uploaded by the supplier. Buyer can Lock the invoice after which seller can’t edit/delete (it becomes confirmed liability of seller).

♦ Input tax credit: Input tax credit shall be given on the basis of acceptance of invoice.

♦ Return design: System will draft Monthly return based on supply data uploaded and inward supply accepted. Annexures will contain these details along with data on B2C, CN/DN, Reverse Charge purchases etc. fed by taxpayer.

♦ Safeguards to be put in place to ensure that system is not gamed

5. Core concepts that have found wide-spread acceptance among all stakeholders.

| Features | Model-A | Model-B |

| Liability on self declared invoices | Yes | Yes |

| Monthly Periodicity of Return for All | Yes | Yes |

| Supplier uploads the invoice | Yes | Yes |

| Unidirectional flow of invoices for calculation of liability and input tax credit. | Yes | Yes |

| Continuous upload of Invoices | Yes | Yes |

| Invoice Level matching of credit as opposed to “ledger-level” or counter-party level on cumulative basis | Yes | Yes |

| No System based matching | Yes | Yes |

♦ Leveraging technology innovations such as Big Data/ Advanced Analytics which is now possible in a Centralized Tax System for identification of potential high risk tax payers

♦ Flagging of potential fraudulent transactions in real-time to both Buyer and Tax authorities Where the Two Models don’t match

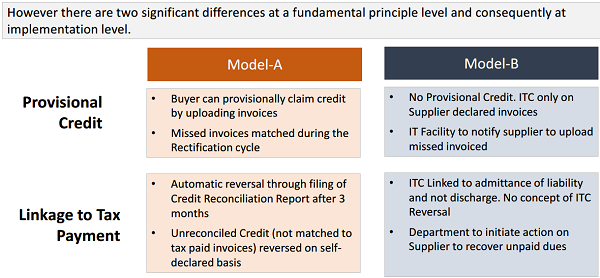

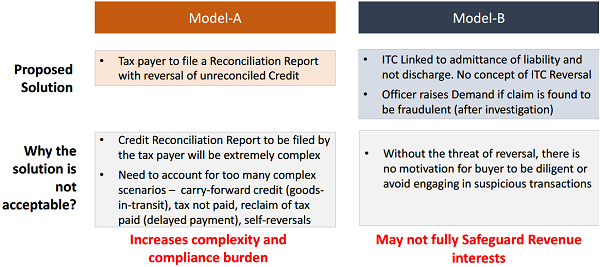

6. Where the Two Models don’t match

7. Principle for reconciling the differences

It has therefore become necessary to reconcile these two differences. To this end we need to establish some core principles on the basis of which the decision can be made…

- In order to objectively reconcile or resolve the differences we need to define some clear goals or markers that shall be used to make the decision. This includes…

- Safeguard the interest of revenue

- Avoid inconvenience to the taxpayers

- Avoidance of complexity of the system (also results in complexity to tax payer)

- We realize that in some cases these may be competing if not conflicting – A balanced view is needed in such situation

- Although not specifically stated, the goal is also to increase tax buoyancy by bringing more transactions into the system (in other words, curb parallel economy)

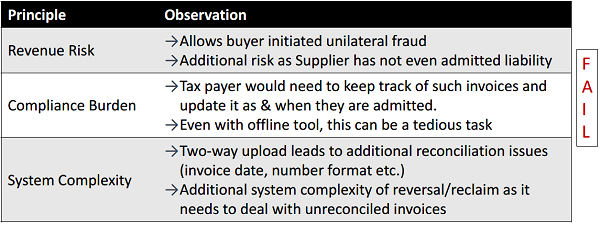

8. Applying 3 Principles on Provisional Credit

Provisional credit will anyway be allowed during the transition period based on GSTR-3B

9. Applying 3 Principles on Linkage to Tax Payment

10. Alternate Solution

Way forward on linkage to payment

♦ Linkage of credit to tax payment is essential and should be continued. (No Change in Law)

♦ However, analysis clearly shows any solution involving automatic reversal of credit is demonstrably complex and hence increases burden on tax payer.

♦ Therefore the best way to implement Linkage to Payment is through ‘Safeguards’ and a semi-automatic reversal of credit through administrative order.

11. Preventive Safeguards

Starting right from preventing fraudulent registrations to limiting the credit flow from defaulting suppliers after a certain threshold

| Prevent Fraudulent Registrations | Credit against Advanced Deposit | Complete Blocking of Credit Flow |

|

|

|

Note: All of the above safeguards could be common to both the models

12. Corrective Safeguards – Semi-automatic Reversal, if preventive safeguard is not sufficient

♦ System can track and generate a list of supplier defaults. Cases from this list may be presented to assessing officer based on configurable rules.

- Rules could pick up candidate for reversal based on thresholds. For e.g. 100% of all high-value, Random 50% of medium value and Random 33% of even lower value

- Every default – however small – may potentially be picked up by the system for reversal with a non-zero probability and not dependent on tax officers’ discretion

♦ System issues notice to the selected cases. If the rectification is not satisfactory, officer may issue a reversal order at the click of a button.

♦ Low risk of revenue loss since the rules will be configured for 100% reversal for high value defaults

♦ No extra compliance burden on the taxpayer such as filing of a reconciliation report.

- May only need to produce proof-of-payment when served with notice

♦ Retains the self-policing aspect of GST design. Non-zero probability of reversal of credit in the event of non-payment.

- For high value defaults, the reversal probability will be nearly 100%

A semi-automated reversal model based on carefully crafted rules is far more desirable than a fully automatic reversal model

13. Conclusion

♦ Most aspects of the solution are common under both the models. But two principal differences exist – Provisional Credit and Linkage to payment of tax

- Provisional Credit not only increases revenue risk but also adds to complexity / compliance burden and hence not recommended.

- Credit linkage to payment of tax by Supplier is essential and should be retained. (No Change in Law)

- However automatic reversal through filing of additional return forms will increase burden on the tax payers

- A semi-automatic process of ITC reversal through administrative order has minimal revenue risk with Simplicity for the tax payer.

- Fusion of both the models (simplicity of operation and design).

- Continuous facility to add invoice by Seller and Continuous viewing of invoices by Recipient who can lock the invoice after which seller can’t edit/delete (it becomes confirmed liability of seller).

- Return design: System will draft Monthly return based on supply data uploaded and inward supply accepted. Annexures will contain these details along with data on B2C, CN/DN, Reverse Charge purchases etc. fed by taxpayer.

- Input tax credit: Input tax credit will be given on the basis of acceptance of invoice. However, Credit linkage to payment of tax by Supplier be retained. (No Change in Law)

- A semi-automatic process of ITC reversal through administrative order. System will track and generate a list of supplier defaults. Cases from this list may be presented to assessing officer based on configurable rules (all or based on quantum of difference). System issues notice to the selected cases. If the rectification is not satisfactory, officer may issue a reversal order at the click of a button.

- Safeguards: Starting right from preventing fraudulent registrations to limiting the credit flow from defaulting suppliers after a certain threshold to making RC inactive for non-filing of return by defaulting sellers.

14. Limitation pointed out for Model-B

| Limitations | Ways to resolve limitations | |

| 1 | Invoice added late would make it multi-loop | The seller will pay the interest. |

| 2 | Accept, finalise, pay and file is not correct due to reverse charge, credit on imports etc. | Reverse charge will be added by buyer. Similarly other components like CN/DN; B2C sales etc. will be added by the taxpayer |

| 3 | Return should be self assessed and declared and not automatically filled. | B2B part will be drafted. Other parts will have to be filled by the taxpayer and then sign the same. |

| 4 | Wrongly locked invoices would complicate design. | Mechanism will have to be introduced to handle it |

| 5 | Law, rules and form would not be easy to draft due to the design moving in completely new territory of locking, supplier side control etc. | The middle path suggested can be drafted in the Law |

| 6 | Revenue concern of default in tax payment and credit control is not addressed in IT model (Model-B). | This is by set of safeguards to cap the damage; by having strict examination for entry into the system, taxpayer rating and use of strong analytics tools. |

15. Other Recommendations

♦ Offline utility to facilitate both upload and acceptance of invoices

♦ IT Facility for locking of the same by Buyer through acceptance

♦ Leveraging technology innovations such as Big Data/ Advanced Analytics which is now possible in a Centralized Tax System for identification of potential high risk tax payers

♦ Flagging of potential fraudulent transactions in real-time to both Buyer and Tax authorities

♦ Staggered filing for Large and Medium/Small Taxpayers

♦ Removal of linkage of CN/DN to Invoice

♦ Removal of reporting like B2C large, Documents etc.